Yahoo Finance

Yahoo Finance

Global Video Telematics Market Report 2023: North America and Europe to Account for 11 Million Video Telematics Systems in Use by 2027

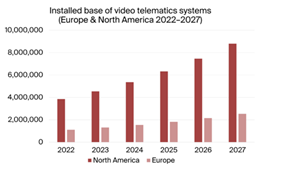

Installed Base of Video Telematics Systems Europe & North America 2022-2027

Dublin, May 11, 2023 (GLOBE NEWSWIRE) -- The "The Video Telematics Market - 4th Edition" report has been added to ResearchAndMarkets.com's offering.

How will the emerging video telematics market evolve in 2023 and beyond? The report covers the latest trends and developments in the dynamic telematics industry. The analyst forecasts that the active installed base of video telematics systems in Europe and North America will grow at a CAGR of 17.7 percent from almost 5.0 million units at the end of 2022 to 11.3 million by 2027. Get up to date with the latest information about vendors, products and markets.

The integration of cameras to enable various video-based solutions in commercial vehicle environments is a massive trend in the fleet telematics sector. The definition of video telematics includes a broad range of camera-based solutions deployed in commercial vehicle fleets either as standalone applications or as an added feature set to conventional fleet telematics. The frontrunning North American video telematics market is more than three times the size of the European, which is so far largely dominated by activities in the UK.

The analyst estimates that the installed base of active video telematics systems in North America reached almost 3.9 million units in 2022. Growing at a compound annual growth rate (CAGR) of 18.0 percent, the active installed base is forecasted to reach 8.8 million units in North America by 2027. In Europe, the installed base of active video telematics systems is estimated to be over 1.1 million units in 2022. The active installed base in the region is forecasted to grow at a CAGR of 17.9 percent to reach 2.5 million video telematics systems in 2027.

The video telematics market is served by a number of different types of players, ranging from specialists focused specifically on video telematics solutions, to general fleet telematics players which have introduced video offerings, and hardware-focused suppliers offering mobile digital video recorders (DVRs) and vehicle cameras used for video telematics. "The analyst ranks Streamax, Lytx and Samsara as the leading video telematics players in their respective categories", said Rickard Andersson, Principal Analyst.

He adds that Streamax is the leading hardware provider, having more than 2.4 million mobile DVRs installed in vehicles worldwide to date. The company also offers software dashboards which are widely used together with its devices. "Lytx has the largest number of video telematics subscriptions, while Samsara stands out among the general fleet telematics players with a significant number of camera units deployed across its subscriber base", continued Mr. Andersson.

Additional sizeable players in this space include the new channel-focused brand Sensata INSIGHTS (including the acquired video telematics company SmartWitness), the fleet management player Motive (formerly KeepTruckin), the hardware-focused video telematics company Howen, and the fleet management provider Solera Fleet Solutions (which acquired the commercial vehicle telematics pioneer Omnitracs including the video safety specialist SmartDrive).

"The remaining top-10 players are Netradyne, Nauto and VisionTrack which all have a primary focus on camera-based solutions specifically", said Mr. Andersson. Other noteworthy players competing in the video telematics space include video-focused solution providers such as Bendix (SafetyDirect by Bendix CVS), Idrive, SureCam, LightMetrics, Waylens, Seeing Machines and CameraMatics; fleet telematics players including Trimble, Matrix iQ, MiX Telematics, Forward Thinking Systems, Radius Telematics, ISAAC Instruments, Azuga, Microlise, Trakm8 and AddSecure Smart Transport; as well as the hardware-focused supplier Pittasoft (BlackVue). "These players have all reached estimated installed bases in the tens of thousands", concluded Mr. Andersson.

Highlights from the report:

Insights from numerous interviews with market-leading companies.

Descriptions of video telematics applications and associated concepts.

Comprehensive overview of the video telematics value chain.

In-depth analysis of market trends and key developments.

Updated profiles of 40 companies offering video telematics software and hardware.

Market forecasts lasting until 2027.

This report answers the following questions:

What different types of players are involved in the video telematics value chain?

Which are the major specialised providers of video telematics solutions?

What offerings are available from the general fleet management solution providers?

How are the hardware-focused suppliers approaching the market?

Which are the frontrunning geographic markets for video telematics solutions so far?

What are the price levels for video telematics hardware and software?

Which trends and drivers are shaping the market?

How will the video telematics industry evolve in the future?

Who should read this report?

The Video Telematics Market is the foremost source of information about this fast-growing application area in the transportation sector. Whether you are a telematics vendor, video specialist, vehicle manufacturer, telecom operator, investor, consultant, or government agency, you will gain valuable insights from our in-depth research.

Key Attributes:

Report Attribute | Details |

No. of Pages | 175 |

Forecast Period | 2022 - 2027 |

Estimated Market Value in 2022 | 5 Million |

Forecasted Market Value by 2027 | 11.3 Million |

Compound Annual Growth Rate | 17.7% |

Regions Covered | Global |

Key Topics Covered:

Executive Summary

1 Video Telematics Solutions

1.1 Introduction to video telematics

1.1.1 Video telematics as a standalone application

1.1.2 Video telematics as an integrated part of fleet telematics

1.2 Video telematics applications and associated concepts

1.2.1 Video-based driver management

1.2.2 Driver fatigue and distraction monitoring

1.2.3 Advanced driver assistance systems (ADAS)

1.2.4 Driver training and coaching

1.2.5 Managed services

1.2.6 Exoneration of drivers and insurance-related functionality

1.3 Business models

2 Market Forecasts and Trends

2.1 Market analysis

2.1.1 Video telematics vendor market shares

2.1.2 The North American video telematics market

2.1.3 The European video telematics market

2.1.4 Rest of World outlook

2.2 Value chain analysis

2.2.1 Video telematics solution providers

2.2.2 Fleet telematics solution providers

2.2.3 Hardware-focused suppliers

2.2.4 Insurance industry players

2.3 Market drivers and trends

2.3.1 Privacy issues expected to soften as video telematics becomes mainstream

2.3.2 Acknowledging the performance of good drivers can alleviate scepticism

2.3.3 Regulatory developments can drive adoption of camera-based technology

2.3.4 Video telematics is at the core of the current M&A wave in the FM space

2.3.5 Partnership strategies increasingly common in the video telematics space

2.3.6 Increasing commoditisation of video telematics hardware expected

2.3.7 OEM integration may ultimately lead to the widespread uptake of video.

2.3.8 Artificial intelligence and machine vision capabilities become table stakes

3 Company Profiles and Strategies

List of Acronyms and Abbreviations

A selection of companies mentioned in this report includes

AddSecure Smart Transport

Azuga (Bridgestone)

Bendix (SafetyDirect by Bendix CVS)

CameraMatics

D-TEG

Exeros Technologies

Fastview 360

FleetCam

Forward Thinking Systems

Howen

iCAM Video Telematics

Idrive

ISAAC Instruments

J. J. Keller

LightMetrics

Lytx

Matrix iQ

Microlise

Micronet

MiX Telematics

Motive (formerly KeepTruckin)

Nauto

Pittasoft (BlackVue)

Positioning Universal

Radius Telematics

Samsara

Seeing Machines

Sensata INSIGHTS (including SmartWitness)

Solera Fleet Solutions (including SmartDrive)

Streamax

SureCam

Teltonika

Trakm8

Trimble

Verizon Connect

Vision Techniques

VisionTrack

VUE (Radius Telematics)

Waylens

For more information about this report visit https://www.researchandmarkets.com/r/463mgq

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment

CONTACT: CONTACT: ResearchAndMarkets.com Laura Wood,Senior Press Manager press@researchandmarkets.com For E.S.T Office Hours Call 1-917-300-0470 For U.S./ CAN Toll Free Call 1-800-526-8630 For GMT Office Hours Call +353-1-416-8900