Yahoo Finance

Yahoo Finance Grainger's (LON:GRI) Shareholders Will Receive A Bigger Dividend Than Last Year

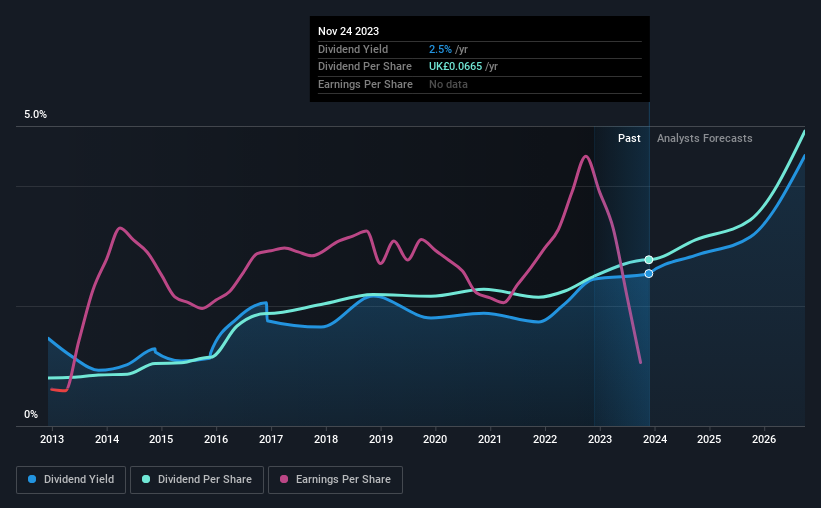

Grainger plc's (LON:GRI) dividend will be increasing from last year's payment of the same period to £0.0437 on 14th of February. Although the dividend is now higher, the yield is only 2.5%, which is below the industry average.

See our latest analysis for Grainger

Grainger's Payment Has Solid Earnings Coverage

Even a low dividend yield can be attractive if it is sustained for years on end. Based on the last payment, Grainger's profits didn't cover the dividend, but the company was generating enough cash instead. Given that the dividend is a cash outflow, we think that cash is more important than accounting measures of profit when assessing the dividend, so this is a mitigating factor.

Looking forward, earnings per share is forecast to rise exponentially over the next year. If the dividend continues along recent trends, we estimate the payout ratio will be 27%, which would make us comfortable with the dividend's sustainability, despite the levels currently being elevated.

Grainger Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. The dividend has gone from an annual total of £0.0192 in 2013 to the most recent total annual payment of £0.0665. This works out to be a compound annual growth rate (CAGR) of approximately 13% a year over that time. So, dividends have been growing pretty quickly, and even more impressively, they haven't experienced any notable falls during this period.

The Dividend Has Limited Growth Potential

The company's investors will be pleased to have been receiving dividend income for some time. However, things aren't all that rosy. Grainger's earnings per share has shrunk at 30% a year over the past five years. Such rapid declines definitely have the potential to constrain dividend payments if the trend continues into the future. Over the next year, however, earnings are actually predicted to rise, but we would still be cautious until a track record of earnings growth can be built.

In Summary

In summary, while it's always good to see the dividend being raised, we don't think Grainger's payments are rock solid. The company is generating plenty of cash, but we still think the dividend is a bit high for comfort. Overall, we don't think this company has the makings of a good income stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Case in point: We've spotted 4 warning signs for Grainger (of which 1 can't be ignored!) you should know about. Is Grainger not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.