Yahoo Finance

Yahoo Finance What happens to my pension when I change jobs?

The days of having a job for life appear to be over. A recent American study found that the average baby boomer had worked for 12 different employers by the time they reached 56.

And it’s a trend which has hopped across the pond, with employees regularly switching jobs. A study by accountancy firm PwC last year found nearly a quarter of Britons (23pc) are expecting to change jobs in the next 12 months.

That equates to more than seven million workers, all of whom will be left needing to make a decision about their workplace pension. It is very possible a new employer will use a different pension provider to your previous place of work, meaning you’ll potentially have several different pots to manage and keep track of.

So does it make sense to consolidate your pension pots? Is it worth keeping your pension with your old employer? And what do you do if you have a dozen different pots and you can’t remember where all of them are?

Here, Telegraph Money explains what happens to your pension when you change jobs and assesses the options available so that you can make a decision which best suits your needs.

How do workplace pensions work?

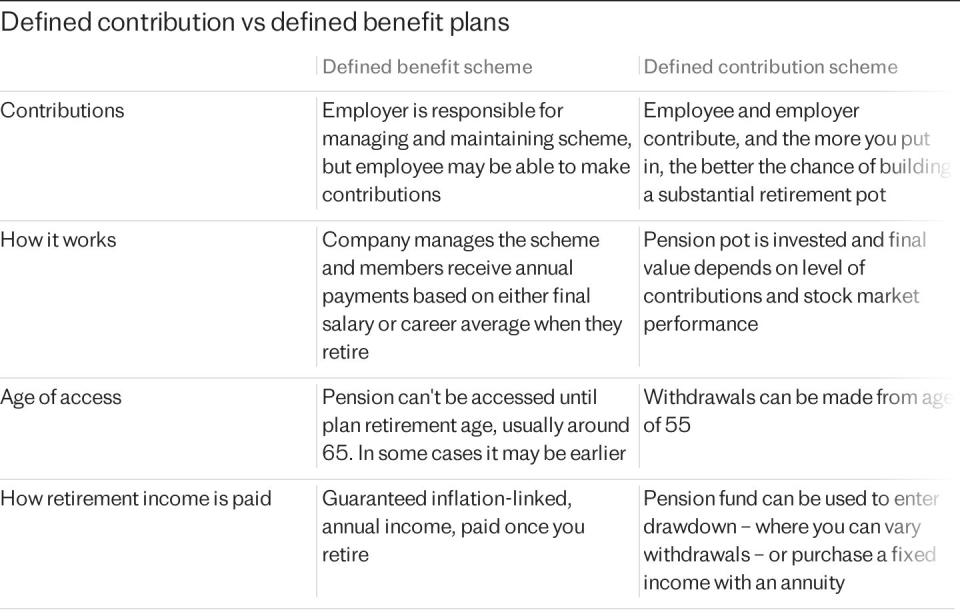

There are two different types of workplace pensions: defined contribution (DC) and defined benefit (DB), which is sometimes referred to as a final salary pension.

Employers have increasingly shifted towards defined contribution pensions – when you come to retire, your pension is based on how much money has been paid in to invest, and how well those investments have performed.

Defined benefit pensions are not linked to investment performance, and are instead a reflection of the years you worked at the company and your salary.

A defined benefit pension pays a secure income for life, which usually rises each year in line with inflation. As such, they are highly sought-after, yet rarely found outside of the public sector or some very large employers.

Pension enrolment rules

Thanks to auto-enrolment rules, it is compulsory for every employer in Britain to automatically enroll eligible workers into the company’s workplace pension scheme, with minimum contributions set at 8pc – this must include at least 3pc from the employer, and 5pc from the employee.

Eligible employees must be aged between 22 and the state pension age, and be earning at least £10,000 a year.

How do workplace pension contributions work?

In most cases, workplace pension contributions take place before you receive your salary, and will be noted on your payslip. Depending on the system your employer uses, the contributions may be paid before tax, meaning you can pay into your pension tax-free, and will pay less income tax and National Insurance as a result of your taxable income effectively being lower.

If the contributions are made after tax, you’ll still receive tax relief on your pension contributions – the Government will automatically add 20pc to the amount you pay in, and higher- or top-rate can claim for the extra 20pc or 25pc tax they’ve paid via a self-assessment tax return.

Recommended

How do pensions work?

What happens to my pension when I leave a company?

It is important to note that when you change jobs, you do not lose the pension pot you had built up while you were working at your “old” company.

In respect of your pension, you don’t have to complete any admin when you switch jobs; the money that’s been paid in will remain invested, and it will have no impact on your ability to access this money when you reach retirement.

However, while leaving your pension savings in several smaller pots might seem like the easy, stress-free solution, it could mean your total retirement savings will suffer in the long term – potentially missing out on thousands of pounds. But equally, some people may be better off leaving their savings where they are.

Recommended

Want a better pension than your colleagues? Here's how to get it

Should I transfer my pension to a new employer?

There are three key reasons why you should consider combining your pension with your new employer when switching jobs.

Firstly, each pension pot comes with fees, including an annual management fee. If you’ve worked in four or five different jobs over the last 20 years, each one of those pots will be charging fees on your investments.

Depending on how much you have saved, and whether the fee is charged as a percentage or at a flat rate, this could make a dent in your savings over time. Combining your pensions into one pension could therefore save you money as you’ll only have to pay one set of fees.

The second thing to consider about having multiple pension pots is their performance – some will inevitably deliver better returns than others. Although it’s important to acknowledge that past performance is not a guide to future returns, it’s worth reviewing where your money is invested and how the pots are performing.

Failing to do this, and choosing to ignore a pension pot for a long period of time could mean missing out on investment growth, had you consolidated into a better performing pension.

But above both of those reasons, combining pensions means it’s so much easier to keep track of your overall position and plan for your retirement. It means receiving one annual benefit statement, being aware of how much you’ve saved and how much more you need to add, without factoring in different statements from different schemes, arriving at different points in the year.

It can also save you from the trap 1.6 million savers have fallen into – losing your pension pot.

Around £37bn is held in lost pension pots, which should be helping fund people’s retirements, according to Gretel, a free platform that searches for lost pensions. The average size of a missing pension pot is £13,000, but some lost pots are thought to be far higher.

Recommended

Where to work for the biggest pension payouts

How do I find a pension plan from a previous employer?

By the year 2050, there could be as many as 50 million dormant and lost pensions, according to the Department for Work and Pensions.

If you fear you have lost a pension from years ago, you are not alone – it is believed more than one in five people are in the same position. However, there are options available to help you recover your hard-earned money.

The first is to send your National Insurance number to HMRC to find out if you were contracted out of the State Earnings-Related Pension Scheme (Serps) in order to boost your workplace pension. Millions of people chose to opt out of Serps during the 1980s and 1990s.

The scheme was designed to top-up state pension payments. It existed from 1978 to 2002, when it was replaced by the State Second Pension, and both schemes were often known as the “Additional State Pension”.

You can perform a Serps pension check by writing to HMRC with your National Insurance number, and you should also include your full name, any previous names if applicable, address and date of birth. HMRC can take up to a month to respond with details of any pension provider you paid into as a result of opting out of Serps.

You will then need to contact the providers to see how much any pension savings are now worth and how you can access them.

For other workplace pensions, you can contact your previous employers who should hold a record of your account and be able to help you access the lost pension. You will need your National Insurance number and the dates you worked at the company.

However, some companies may no longer exist, or are difficult to contact. In this instance, the Government’s free Pension Tracing Service may be able to help you find them.

Using your National Insurance number and the dates you worked at the company, the Pension Service will check against its own records and pass on the name of your pension provider and policy number.

Recommended

How to track down your long-lost pensions – and consolidate them

Why might you consider keeping pensions from previous jobs separate?

There are instances when you might be better off leaving your pension pot as it is, even when you change jobs.

This is particularly true of jobs you have worked at for a long time, because some older pensions may have valuable features you’ll lose if you transfer out – such as guaranteed annuity rates. Given the volatility of annuity rates in recent years, a guaranteed rate could provide greater security in your retirement.

Some schemes also come with a “protected pension age”, which means you can take the pension before you turn 55.

You should also consider the exit fees involved in transferring your pension to a different provider; if this is particularly high, it might not be worth making the move.