Yahoo Finance

Yahoo Finance Is HeidelbergCement (ETR:HEI) A Risky Investment?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that HeidelbergCement AG (ETR:HEI) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for HeidelbergCement

What Is HeidelbergCement's Debt?

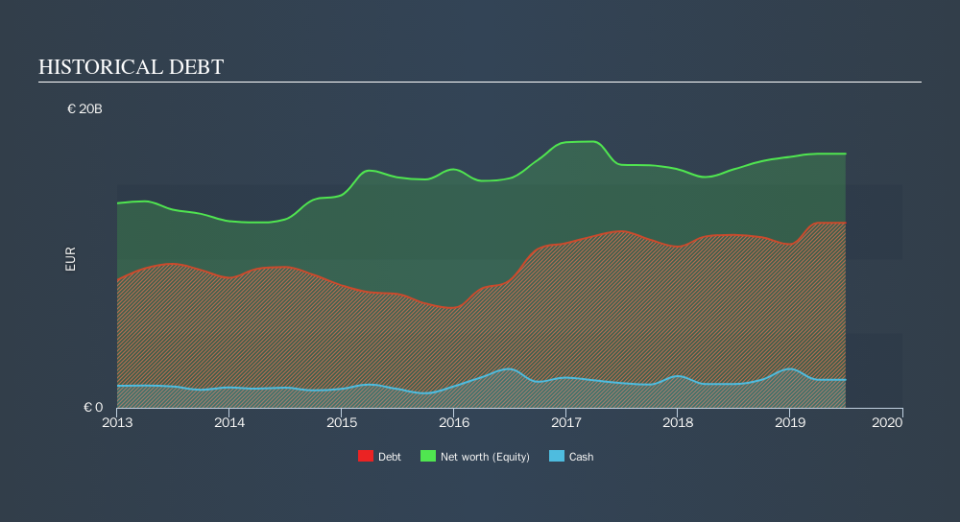

As you can see below, at the end of June 2019, HeidelbergCement had €12.4b of debt, up from €11.6b a year ago. Click the image for more detail. However, it also had €1.88b in cash, and so its net debt is €10.5b.

How Strong Is HeidelbergCement's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that HeidelbergCement had liabilities of €7.79b due within 12 months and liabilities of €12.2b due beyond that. On the other hand, it had cash of €1.88b and €3.24b worth of receivables due within a year. So it has liabilities totalling €14.9b more than its cash and near-term receivables, combined.

Given this deficit is actually higher than the company's massive market capitalization of €12.4b, we think shareholders really should watch HeidelbergCement's debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

HeidelbergCement's debt is 3.6 times its EBITDA, and its EBIT cover its interest expense 6.2 times over. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. HeidelbergCement grew its EBIT by 5.1% in the last year. That's far from incredible but it is a good thing, when it comes to paying off debt. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine HeidelbergCement's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. In the last three years, HeidelbergCement's free cash flow amounted to 48% of its EBIT, less than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

We'd go so far as to say HeidelbergCement's level of total liabilities was disappointing. Having said that, its ability to grow its EBIT isn't such a worry. Looking at the balance sheet and taking into account all these factors, we do believe that debt is making HeidelbergCement stock a bit risky. Some people like that sort of risk, but we're mindful of the potential pitfalls, so we'd probably prefer it carry less debt. Another positive for shareholders is that it pays dividends. So if you like receiving those dividend payments, check HeidelbergCement's dividend history, without delay!

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.