Yahoo Finance

Yahoo Finance Help to Buy revival risks trapping first-time buyers in overpriced homes

Rishi Sunak’s pledge to revive the Help to Buy equity loan scheme risks trapping buyers in poorly-built overpriced homes, experts have warned.

Help to Buy – a former Tory flagship policy – helped 328,346 first-time buyers onto the housing ladder, before being axed in October 2022. It offered buyers of new builds a 20pc interest-free government loan for the five years.

The Prime Minister said under a Tory government, the scheme would return for another three years – and this time, the developers would foot a portion of the equity loan.

Rishi Sunak said the reboot would help “hundreds of thousands of families” take out mortgages “immediately” and pledged to build another 1.6 million new homes over the next parliament.

But experts have warned that reinstating the scheme in an environment of high interest rates could have big consequences, after the first version of the scheme inflated house prices by 7.94pc and has more recently exposed owners to negative equity.

Thousands of borrowers in the scheme are also struggling financially now interest is payable on the equity loan. Between 2022 and 2023, the number of Help to Buy households falling behind on repayments more than doubled.

Those trying to pay off their equity loans before interest kicks in, or those trying to sell, have encountered severe delays in response times.

The Conservatives said Homes England would continue to manage the scheme, despite a surge in customer service complaints last year and a more recent administrative error leading to houses being put in the wrong names.

Complaints of poor quality housing built under the previous scheme have also gone unacknowledged by the party. In December, a survey of 2,000 Britons by the Chartered Institute of Building found 60pc would not buy a new-build home – with a third saying they were “poor quality”.

Help to Buy inflated first-time buyer homes by 8pc

The first version of Help to Buy lasted a decade, stretching from 2013 to 2023. It could be used on houses worth up to £600,000 by first-time buyers, allowing them to put down a 5pc deposit.

The Government would then put down 20pc of the purchase price in the form of an equity loan, which was interest-free for the first five years before a 1.75pc interest rate kicked in.

In London, the equity loan size was double – 40pc – due to higher house prices.

Christian Hilber, professor at the London School of Economics, said bringing back the scheme was “a really bad idea” because it would increase demand specifically for starter homes.

“Prices for these homes, especially in the most unaffordable areas – Greater London and the South East – would increase even more, relative to what they would be without the policy.”

His research, now published in the Journal of Urban Economics alongside fellow academics Felipe Carozzi and Xiaolun Yu, found that Help to Buy increased the price of newly built homes by about twice as much as what buyers saved in interest.

Mr Hilber added: “Pushing up demand in light of unresponsive supply is not a solution, it’s part of the problem.”

Paul Cheshire CBE, a second professor at LSE, said a new version of the scheme now would inflate house prices “with boosters” – since the rate of house building is even worse now than it was.

“The scheme inflated house prices for eligible homes by more than the expected ‘value’ of the subsidy in all those areas where supply was tight – that is all over southern England – and affordability worse. The new proposals will do the same with boosters, “ he said.

Help to Buy increased house prices by 7.94pc, according to LSE’s research, and boosted developers’ revenues by 54pc – translating into profits of £64m.

Mr Cheshire added: “Labour does have policies to boost house building, but they will likely only increase building rates after a lag of at least three years.”

Negative equity

Marc von Grundherr, of estate agent Benham and Reeves, said the Government’s decision to fuel a “market imbalance” between supply and demand by reviving a scheme like Help to Buy will just see house prices remain dangerously inflated – and therefore more vulnerable to big drops.

“Help to Buy has been nothing but another poorly devised initiative to give the impression of success based on house price prosperity – when the reality is that the housing crisis simply can’t be solved by driving demand.

“To re-introduce it at a time when house prices remain close to record highs would be very ill-advised and it’s time that a longer term approach was implemented to get Britain building the homes it desperately needs.”

House prices have risen 1.3pc over the past year, according to high street bank Nationwide’s House Price Index. Over the past five years, house prices in rural areas have risen by 22pc, and 17pc in urban areas.

Four years ago, Daniel Hyatt bought a £450,000 three-bed in Guildford through the Government’s Help to Buy.

He told The Telegraph last year that he was in something of a Catch 22, in that if his house price rises then so does the size of the equity loan, making it harder to pay off before interest kicks in.

But if his house price drops too low, then Mr Hyatt and his wife could fall into negative equity – it only needs to fall by 5pc since he bought it for this to happen.

Interest rates bearing down

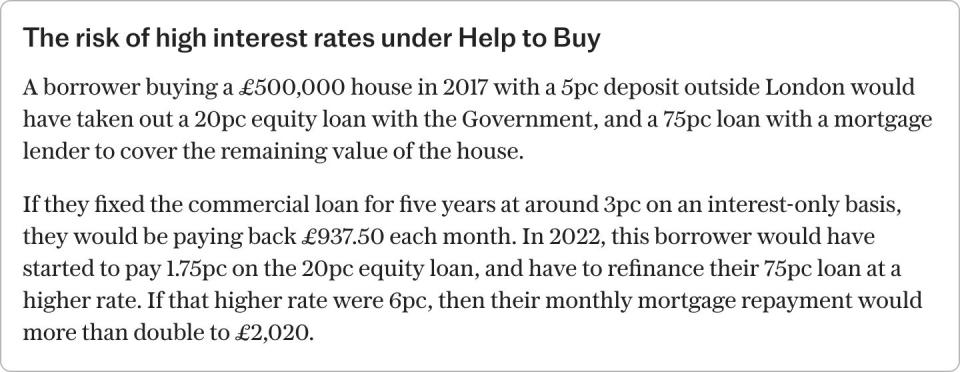

In 2020, the Bank Rate was 0.1pc, and mortgage rates hovered around 2pc. But since then, interest rates have risen considerably.

The average two-year fixed rate today is 5.96pc, and the average five-year fixed rate 5.52pc according to Moneyfacts.

Holly Tomlinson, a financial planner at wealth manager Quilter, said while another Help to Buy Scheme could help those with smaller deposits – high interest rates could become debilitating.

This is because no interest is payable on the equity loan for the first five years, but in the sixth year, a 1.75pc interest rate kicks in, which is compounded in line with inflation each year thereafter.

Borrowers also cannot pay off their equity loan in smaller chunks than half, or in full, and have to pay a solicitor each time they do this. In London, because the equity loan is double the size, borrowers can pay it back in quarters.

Ms Tomlinson said: “The Government’s previous equity loan scheme had a substantial impact on first-time buyers, with 387,195 properties bought using the scheme between April 2013 and May 2023 – out of which 328,346 were by first-time buyers.”

“The loans became increasingly burdensome for homeowners when they reached the end of their five-year interest-free loan period, as other costs had risen considerably. So despite intending to be an assistance programme, the scheme actually added financial strain to borrowers.”