Yahoo Finance

Yahoo Finance Here's Why BankUnited (BKU) is Worth Betting on Right Now

BankUnited, Inc. BKU is well-positioned for growth on the back of decent loans and deposit balance and fee income growth. Further, the current high interest rates environment will aid its financials.

Analysts are also optimistic about the stock’s earnings growth potential. Over the past 30 days, the Zacks Consensus Estimate for earnings for both 2024 and 2025 has moved upward by a penny. BKU currently carries a Zacks Rank #2 (Buy).

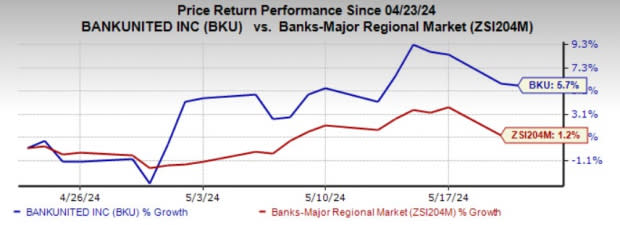

Over the past month, shares of BankUnited have rallied 5.7%, outperforming the industry’s growth of 1.2%.

Image Source: Zacks Investment Research

Let’s dive deeper into the reasons that make BKU stock a lucrative bet now.

Earnings Growth: BankUnited witnessed earnings growth of 6.17% over the past three to five years, which is in line with the industry average, driven by decent top-line growth and an improving deposit mix.

The upward trend is expected to continue in the near term. While we project BKU’s earnings to decline in 2024 by 11.4%, the metric is estimated to rebound in 2025 and 2026 with 10.1% and 4.2% year-over-year growth, respectively.

Revenue Strength: BKU’s total revenues witnessed a CAGR of 2.8% over the last five years (ended 2023). This uptick primarily resulted from the company’s efforts to stabilize funding costs and modest expansion in net interest income on the back of higher rates since 2022. Also, loans and deposit balances continued to rise. In the last five years, loans and deposits recorded a CAGR of 3.8% and 2.1%, respectively.

Though the Federal Reserve has signaled rate cuts this year, the interest rates are expected to remain high to control inflation. This, along with strong loans and deposit balance, will keep supporting BankUnited’s top line despite rising deposit costs weighing on it.

As of Mar 31, 2024, BankUnited’s non-interest-bearing demand deposits constituted 26.8% of total deposits. The company’s strategic shift toward a low-cost deposit mix in order to stabilize funding costs will further aid revenues.

We project the company’s revenues to grow at the rate of 3.3% and 4.4% in 2024 and 2025, respectively. While loans are projected to witness marginal growth in 2024, deposits are estimated to grow 7.4%.

Impressive Capital Distributions: BKU’s capital distribution activities are encouraging. For the first time, the company hiked its dividend by 10% to 23 cents per share in February 2020. Since 2020, the company has been hiking its dividend annually, with the most recent hike in February 2024. Additionally, BankUnited’s board of directors authorized the buyback of up to an additional $150 million worth of shares in September 2022 with no expiration date. As of Mar 31, 2024, $20.2 million remained under the buyback authorization.

Given its decent earnings strength, the company is expected to continue efficient capital distributions, thus enhancing shareholder value.

Stocks Seems Undervalued: BankUnited’s stock seems undervalued as its price-to-earnings (F1) and price-to-book ratios of 10.67 and 0.83, respectively, are well below the industry averages of 11.58 and 1.22.

It has a Value Score of B. The Value Score condenses all valuation metrics into one actionable score that helps investors steer clear of “value traps” and identify stocks that are truly trading at a discount. Our research shows that stocks with a Style Score of A or B, when combined with a Zacks Rank #1 (Strong Buy) or 2, offer the best upside potential.

Other Stocks to Consider

A couple of other stocks from the financial services space worth a look are Northern Trust Corporation NTRS and Wells Fargo & Company WFC, each sporting a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for NTRS’ current-year earnings has been revised marginally upward over the past week. Shares of the company have risen 11.1% in the past six months.

Estimates for WFC’s 2024 earnings have been revised marginally upward over the past month. Over the past six months, shares of the company have gained 43.7%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Wells Fargo & Company (WFC) : Free Stock Analysis Report

Northern Trust Corporation (NTRS) : Free Stock Analysis Report

BankUnited, Inc. (BKU) : Free Stock Analysis Report