Yahoo Finance

Yahoo Finance Here's Why Investors Should Buy Home Depot (HD) Stock Now

The Home Depot Inc. HD has been going strong thanks to the momentum in the home improvement industry, which has been benefiting from sustained demand for home-improvement projects and a robust housing market. Home Depot, in particular, has been gaining from growth in Pro and DIY customer categories, digital momentum and its ongoing investments. It remains on track with the execution of the “One Home Depot” investment plan, which bodes well.

The aforementioned factors helped the company deliver a robust performance in third-quarter fiscal 2021. The company reported sales and earnings beat for the sixth straight quarter in third-quarter fiscal 2021. The top and bottom lines also improved year over year. Home Depot has a robust earnings beat streak for the last four quarters, the average being 12.1%. This underlines the company’s operational excellence.

In the past seven days, estimates for the company’s fiscal 2021 and 2022 earnings per share have moved up 0.5% and 0.4%, respectively. For fiscal 2021, its earnings estimates stand at $15.42 per share, suggesting a rise of 28.2% from the year-ago reported figure.

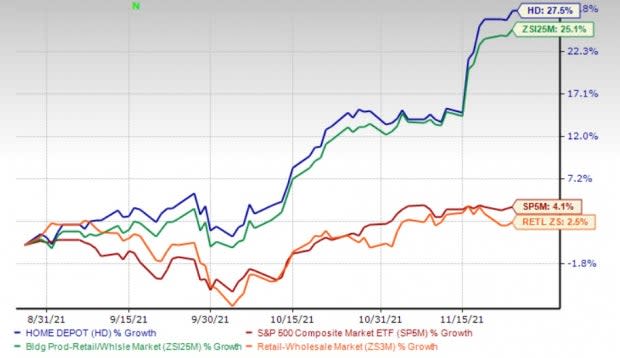

The Zacks Rank #1 (Strong Buy) stock has rallied 27.5% in the past three months compared with the industry’s growth of 25.1%. The stock comfortably outpaced the S&P 500’s growth of 4.1% and the Retail-Wholesale sector’s rise of 2.5% in the same period.

Image Source: Zacks Investment Research

Factors Aiding Growth

We are optimistic regarding Home Depot’s execution of the “One Home Depot” investment plan, which focuses on expanding supply-chain facilities, technology investments and enhancement to the digital experience. The company continues to leverage the momentum in strategic investments to enhance the interconnected experience to support its goals of driving growth faster than the market in any environment, strengthening its position as a low-cost provider in home improvement and delivering exceptional shareholder value.

The interconnected retail strategy and underlying technology infrastructure have aided in consistently driving web traffic for the past few quarters. Sales leveraging the digital platforms rose 8% in the fiscal third quarter. On a two-year stack basis, sales from digital platforms increased nearly 95%. Around 55% of the online orders were delivered from a store.

Another key component of delivering an interconnected experience is enhanced delivery and fulfillment options. Over the years, the company has created the fastest and most efficient delivery network in home improvement through options like buy online pickup in store (BOPIS) with convenient pickup lockers, buy online deliver from store with express car and van delivery, and curbside pickup.

Home Depot’s Pro segment has been a key growth driver, with the Pro segment witnessing robust sales growth for the past several quarters. Pro sales growth outpaced DIY sales in the fiscal third quarter. The growth in the Pro segment reflects significant demand for larger projects in the home improvement industry. During the quarter, the company witnessed strength in several Pro-heavy categories like drywall, pipe and fittings, and several mill-work categories.

The company expects continued sales growth from Pros as project demand remains strong and their backlogs are growing. The company remains on track with its strategic investments to build a Pro ecosystem that includes professional grade product, exclusive brands, enhanced delivery, credit, digital capabilities, field sales support, HD rental and more. The company expects its differentiated Pro ecosystem to help in deeper engagement with Pro customers in the long term.

Wrapping Up

Although the company is witnessing favorable demand conditions, rising expenses stemming from increased penetration of lumber products and transportation costs have been a concern for the company. It reported a soft gross margin in the fiscal third quarter as a result of higher cost of goods sold. Rising transportation costs and mix of products sold led to higher cost of goods sold.

Nevertheless, solid execution of growth strategies along with compelling product offering has been helping the company to efficiently meet demand conditions. This along with favorable conditions prevailing in the home improvements market is likely to keep supporting Home Depot’s growth in the days ahead.

Other Stocks to Bet On

We have highlighted three other top-ranked stocks in the Retail - Wholesale sector, namely Tecnoglass TGLS, Lowe's Companies LOW and Fastenal FAST.

Tecnoglass currently sports a Zacks Rank #1. The company has a trailing four-quarter earnings surprise of 34.5%, on average. Shares of TGLS have rallied 43.2% in the past three months. You can see the complete list of today's Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Tecnoglass’ current financial year sales and earnings per share suggests growth of 31.2% and 84.8%, respectively, from the year-ago period's reported figures. TGLS has an expected EPS growth rate of 20% for three-five years.

Lowe's, the main competitor of Home Depot, currently carries a Zacks Rank #2 (Buy). The company has a trailing four-quarter earnings surprise of 14.3%, on average. Shares of LOW have risen 22.7% in the past three months.

The Zacks Consensus Estimate for Lowe's current financial year sales and earnings per share suggests growth of 6.9% and 33.8%, respectively, from the year-ago period. LOW has an expected EPS growth rate of 14.6% for three-five years.

Fastenal currently has a Zacks Rank #2. The company has a trailing four-quarter earnings surprise of 2%, on average. Shares of FAST have appreciated 9.4% in the past three months.

The Zacks Consensus Estimate for Fastenal's current financial year sales and earnings per share suggests growth of 5.5% and 5.4%, respectively, from the year-ago period. FAST has an expected EPS growth rate of 9% for three-five years.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Fastenal Company (FAST) : Free Stock Analysis Report

Lowe's Companies, Inc. (LOW) : Free Stock Analysis Report

The Home Depot, Inc. (HD) : Free Stock Analysis Report

Tecnoglass Inc. (TGLS) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research