Yahoo Finance

Yahoo Finance Home buyer inquiries flatlined in April amid affordability challenge – surveyors

New home buyer inquiries fell back in April following three months of increases in a row, according to surveyors.

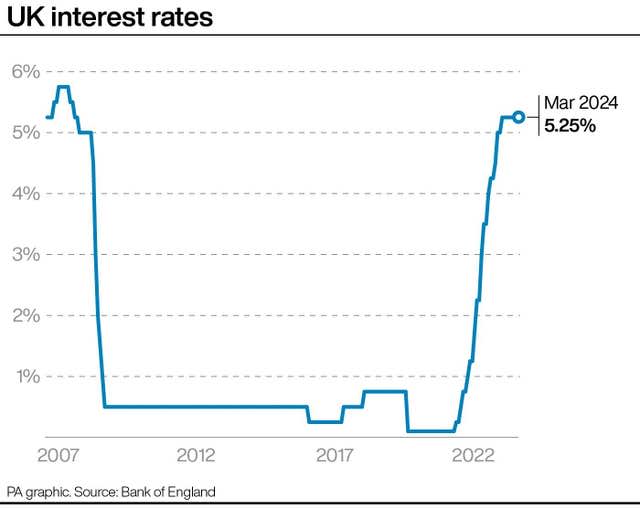

The Royal Institution of Chartered Surveyors (Rics) said its latest survey of property professionals suggests that a recent recovery in buyer demand has mellowed slightly, with the market seeming to have been impacted by mortgage rates edging up over the past few weeks.

A net balance of 1% of property professionals reported new buyer inquiries falling rather than rising in April, following a balance of 6% reporting inquiries rising in March.

The regional feedback on buyer demand is mixed, with a notable loss of momentum mainly seen in London and southern parts of England, Rics said.

Looking at the number of properties available on the market, a net balance of 23% of professionals noted an increase in new instructions to sell during April.

This represents the most positive figure since September 2020, Rics said.

Average stock levels have picked up to a three-year high, at 43 properties per branch, the report said.

Agreed sales have also improved, with a net balance of 5% of professionals seeing an increase rather than a fall in transactions.

Although this marks the most positive reading since May 2021, it only suggests a minimal increase in monthly sales, the report said.

A balance of 1% of professionals expect house sales to fall rather than rise in the next three months, marking the weakest reading since October 2023.

Over the coming year, a net balance of 33% of professionals expect house sales to rise rather than fall.

A balance of 5% of professionals reported prices falling rather than rising in April. This was unchanged from the previous month.

Virtually all parts of England returned either a flat or marginally negative reading for house prices, while Northern Ireland and Scotland continued to see an upward trend in property values, the report said.

Looking at the lettings market, feedback suggests that tenant demand is continuing to lose momentum, but landlord instructions remain in short supply, Rics said.

Simon Rubinsohn, chief economist, Rics, said: “Feedback to the latest Rics survey demonstrates the sensitivity of the sales market to interest rates at the present time, given the continuing challenge around affordability.

“A modest back up in mortgage pricing has contributed to the flatlining in the buyer inquiries metric over the past month, as well as the slightly more cautious signals around near-term expectations.

“That said, there is still a strong perception that activity in the market will pick up in the latter part of the year and into 2025, irrespective of any political uncertainty around the general election.

“As far as the lettings market is concerned, an increasing number of respondents are also drawing attention to affordability constraints, and this is reflected in a more modest pace of rental growth. But a fundamental problem in the market across much of the country remains the imbalance between demand and supply with new instructions continuing to decline.”

The report was released as a forecast from EY Item Club suggested that UK mortgage lending could grow by just 1.5% (net) in 2024, as stretched affordability and high borrowing rates continue to affect home-buying demand.

However, growth is forecast to increase in 2025, provided inflation continues to fall and interest rates are cut later this year as expected.

The pace of economic recovery is likely to accelerate over the course of this year and an expected first cut in the Bank of England base rate in the summer should lift consumer sentiment and drive a rise in housing demand in 2025, according to the prediction.

The EY Item Club forecasts that growth in UK mortgage lending will more than double compared with 2024 levels in 2025 (to 3.2% net) and reach 3% (net) in 2026.

It also expects write-off rates on UK mortgages to rise in 2024 and 2025, as higher mortgage costs impact some borrowers’ abilities to meet repayments.

While 2025 write-off rates are expected to be the highest since 2015, low unemployment will keep mortgage write-offs below average levels seen in the 2010s, according to the forecast. Write-offs are then expected to fall in 2026, providing pressure from high interest rates eases.

Anna Anthony, UK financial services managing partner at EY, said: “While we are hopefully beginning to see economic recovery in the UK, both households and businesses continue to face high borrowing costs.

“This of course has knock-on effects on bank lending, and activity in the housing market has been particularly impacted. High living and lending costs have meant fewer house purchases, and although we’re starting to see signs that activity is picking up, we expect mortgage lending growth to be very low again this year.

“If inflation continues to fall and interest rates are cut in the coming months as expected, we believe economic recovery and market confidence will gain momentum in 2025. However, election uncertainty in the UK and in the US, alongside rising geopolitical tensions in the Middle East and Ukraine, mean potential risks to the downside remain very real.”