Yahoo Finance

Yahoo Finance This investment’s short-term volatility is a price that is well worth paying

Investing in shares is not for the faint-hearted. While the stock market has historically produced exceptional returns over the long run, bouts of extreme volatility and temporary decline litter its track record.

As a result, any individual who buys shares must accept that they will not encounter a smooth path to high returns.

Share price volatility is particularly pronounced among smaller companies such as those held in Questor’s inheritance tax (IHT) portfolio.

Over recent years, our positions have regularly flip-flopped between phases of rapid gain and periods of dramatic decline due to a changing economic outlook and the inherent mood swings of investors.

Crucially, though, our holdings are fundamentally sound and have significant growth potential over the coming years. Therefore, short-term volatility is a price worth paying for high long-term returns.

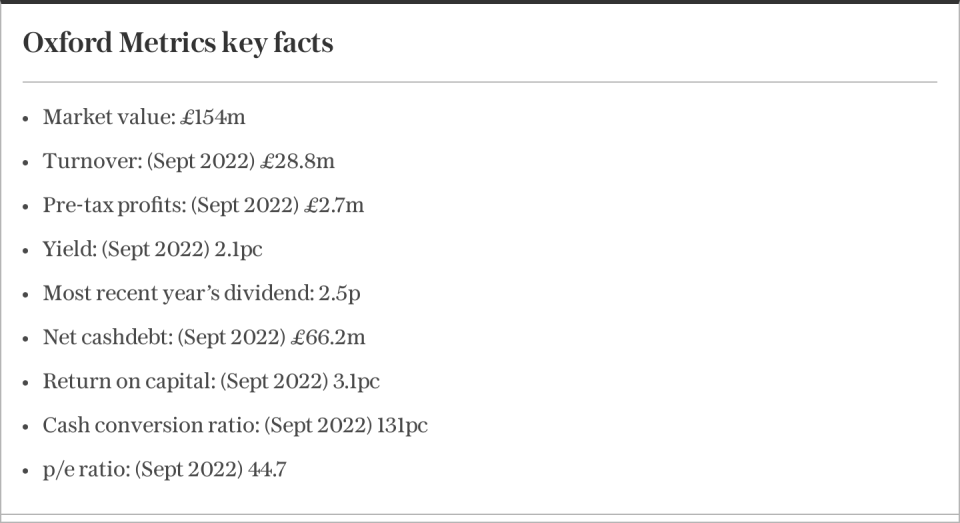

For example, motion capture technology specialist Oxford Metrics has generated a 29pc capital gain since being added to our IHT portfolio in September 2019 in spite of considerable share price turbulence along the way.

Its recently released interim results represented its best ever half-year performance, with revenue growing by 70pc and adjusted pre-tax profits rising by 1,263pc versus the same period of the prior year.

It experienced buoyant trading conditions that contributed to a 68pc increase in the size of its order book. This provides improved visibility during an uncertain period for the economy, with the company now expecting its full-year performance to be ahead of current market expectations.

Unsurprisingly, this news has prompted an 18pc share price rise since the release of its interim results earlier this month.

With net cash of £64m, Oxford Metrics is in an excellent position to make acquisitions at a time when many smaller companies trade at attractive prices. In its interim results, it stated that it has “ongoing active engagements with a number of specific opportunities”.

This suggests that, as well as having organic growth potential from continued high demand across its various divisions, its financial performance could be catalysed by acquisitions over the coming years.

Trading on a forward price-to-earnings ratio of around 31, the company’s shares may be deemed expensive by some investors. Indeed, it is not difficult to find high-quality small-cap stocks that trade on far lower earnings multiples.

However, in Questor’s view, the company offers attractive long-term growth potential.

Its large net cash position provides a degree of stability during an uncertain period for the economy, as well as the potential to make acquisitions that further enhance growth.

While ongoing share price volatility is a given, Oxford Metrics remains a worthwhile holding.

Questor says: hold

Ticker: OMG

Share price at close: £1.17

Update: Michelmersh

Shares in specialist brick manufacturer Michelmersh have also been highly volatile since they were added to our IHT portfolio in January 2018.

Having soared to an 86pc gain in little over three years, they have slumped as the UK’s economic outlook has become more challenging. As a result, they are now up just 12pc versus our notional purchase price.

Encouragingly, last month’s trading update showed the company is on track to meet full-year guidance.

This followed an upbeat set of full-year results, with revenue rising by 15pc and pre-tax profits moving 18pc higher year-on-year.

The company was able to successfully raise prices to mitigate the impact of high inflation, with its operating profit margin moving 0.3 percentage points higher to 17pc. Improving financial performance prompted a 16pc rise in dividends per share so that the company’s yield stands at 4.5pc.

With a net cash position of around £11m, the company has the financial strength to overcome a period of weaker growth prompted by rising interest rates.

Indeed, the construction industry is set to experience a tough period as higher borrowing costs weigh on demand. This could act as a drag on the firm’s near-term profitability and prompt heightened share price volatility.

An uncertain economic outlook, though, creates opportunities for financially sound businesses to acquire rivals at discounted levels.

And with Michelmersh’s recent purchase of prefabricated building solutions firm FabSpeed having boosted its profitability, it would be unsurprising for further acquisitions to take place.

Although one of the company’s Co-CEOs will leave in May, its move to a sole CEO management structure is unlikely to prompt a major strategy change.

With a forward price-to-earnings ratio of 9, the stock continues to offer good value for money on a long-term view.

Questor says: hold

Ticker: MBH

Share price at close: 95p

Read the latest Questor column on telegraph.co.uk every Sunday, Tuesday, Wednesday, Thursday and Friday from 6am.

Read Questor’s rules of investment before you follow our tips.