Yahoo Finance

Yahoo Finance Isa vs savings account: which one is right for you?

Higher interest rates may have hit borrowers – but it’s a good time to be a saver.

Interest rates on savings accounts are at highs not seen for more than a decade, with average returns finally beating inflation.

There are a few different types of savings account to choose from, giving different levels of access and returns, plus savers can also ensure they pocket any returns tax-free by using an Isa.

Savers can earn 3.12pc on an easy-access account or 4.58pc on a one-year fixed rate.

Isa savers can earn 3.33pc on an easy-access Isa and 4.42pc on a fixed rate.

So when it comes to an Isa versus savings account, where is the best place to stash your cash?

What is an Isa?

An individual savings account or Isa lets you put money away and earn any returns tax free.

The two most popular types are cash Isas, which pay a fixed interest rate, and stocks and shares Isas, where you put your money to work through investing in listed companies or funds and any growth is tax-free.

It is also possible to back peer-to-peer loans through an Innovative Finance Isa, or to save for a mortgage deposit or your retirement using a Lifetime Isa.

Most savers will compare the benefits of a cash Isa to a savings account as they are structured in a similar way. Cash Isas may offer an easy-access rate, or you could get a higher return by opting for a fixed rate over a set period.

The easy-access rate may be high to tempt you but these deals are often variable so could change at short notice, while a fixed-rate Isa will stay the same for a defined period.

Tax Benefits of an Isa

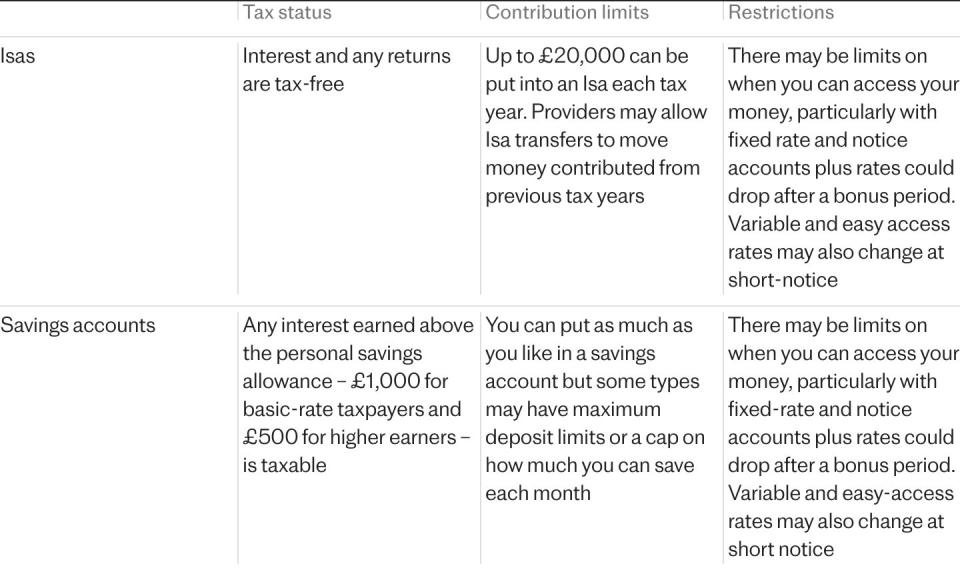

The main tax benefit when comparing an Isa with savings accounts is that any interest earned is tax-free. HM Revenue & Customs (HMRC) can’t get its hands on any of your hard-earned Isa savings.

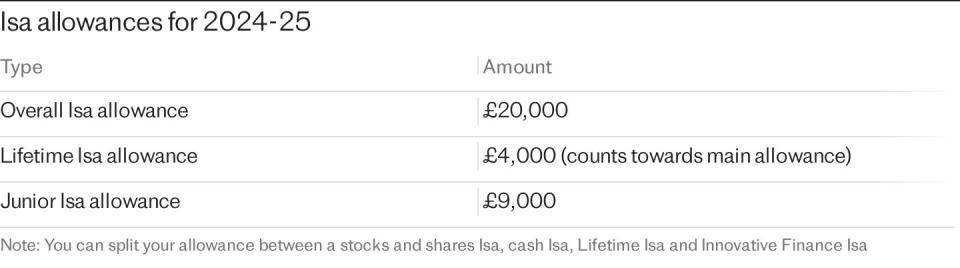

You can put up to £20,000 into a cash Isa, or spread across different types of the wrapper each tax year.

Plus, you can transfer Isa money that has been contributed in previous years to accounts paying higher returns on top of whatever you are putting away for the current year.

Deposit limits in an Isa

You can put up to £20,000 into an Isa each tax year. You can usually pay the full amount into one account, or choose to split it among several. However, there is a £4,000 annual limit on Lifetime Isa, which comes out of your main allowance.

Since April 2024 it has also been possible to contribute to multiple types of the same Isa, meaning you can have more than one newly opened cash Isa that you put money into at the same time, as long as the provider supports this and you stay within the £20,000 limit.

It is also possible to transfer Isa money from previous tax years to combine into different cash Isas and retain its tax-free status, which may be a good idea if you find a better interest rate.

Account limits in an Isa

Some of the best cash Isa rates will require you to lock up your money for a few years, typically between one and five.

There may be limits on how many times you can access your money without penalties, or you could lose interest if you withdraw your cash before the end of the term.

It may be worth opting for an easy-access account if you think you will need regular access to your money. However, the rate may be lower and is likely to be variable, so could change at any point.

What is a savings account?

In contrast to an Isa, a savings account pays interest – but there may be tax to pay depending on how much you have saved and the interest rate.

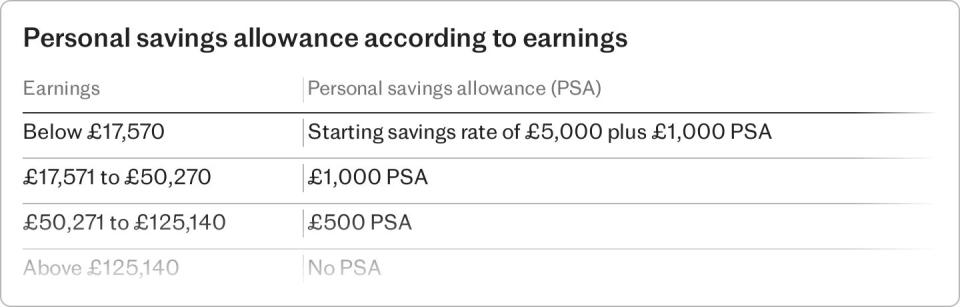

Savers benefit from the personal savings allowance. This lets basic-rate taxpayers earn up to £1,000 a year from their savings tax-free, dropping to £500 for higher earners.

It was hard to get close to the allowance limit when savings rates were low, but the chances of breaching it have got higher as returns have improved.

Types of savings accounts

Similar to an Isa, savings accounts can be offered as easy access, where you can make withdrawals as and when you wish or as a fixed rate where your money is locked away.

There may also be notice accounts that limit the number of withdrawals over a year or let you take money out after a set period.

Another option is a regular saver account, where you set up a monthly direct debit in return for a fixed rate.

Some current account providers may offer special savings rates for customers so it is also worth checking your own bank for exclusive deals.

Interest rates in a savings account

Rates of interest will vary depending on the type of account but are typically higher if you fix for longer periods.

Some of the best deals in recent months have been on regular saver accounts or products for existing current account customers.

Watch out for accounts that attract you with bonus rates, which then drop after a year. It is worth checking what a rate will drop to so you can work out just how competitive the product is.

Accessibility and withdrawal limits

Savings accounts have different levels of flexibility when it comes to how much you can put in and take out.

The most flexible is usually an easy-access account, where savers can typically put in and take out as much as they want.

Some may limit how much you can deposit, particularly on regular savers. This is how providers can afford to offer high rates as you will typically only be able to contribute a few hundred pounds each month.

Other savings accounts may also have restrictions. A notice account may require savers to give 30, 60 or 90 days’ notice to access their money. Some may even say you can only make withdrawals a set number of times each year.

Fixed rate accounts may let you make early withdrawals but you could lose any interest.

Comparing Isas and savings accounts

Tax implications

Any money earned in an Isa is tax-free.

There may come a point where you need to think about tax when it comes to a savings account though.

With interest rates at 15-year highs of around 5pc, it can be very easy for a big sum in savings to push you over the personal savings allowance. That could mean owing money to the taxman.

For example, if you earn 5pc on your savings, you can put away £20,000 before owing any tax on the interest if you are on the basic rate but £10,000 if you are a higher-rate taxpayer.

Higher-rate taxpayers may be better off making use of your Isa allowance as the limit is much higher.

Contributions

Isas have a high contribution limit, at £20,000 a year, plus you don’t have to worry about tax.

Savers may have to think about how much they put into a cash savings account if they are coming close to breaching the personal savings allowance.

Some savings accounts could have limits on how much you can deposit, while Isa savers may benefit from transferring money from previous tax years into an account to earn more interest if the provider supports this.

Both types may have a minimum amount you need to deposit to open the account.

Flexibility in accessing funds

Both cash Isas and savings accounts may have limits on how often you can access your money, particularly on fixed rate or notice accounts.

Some Isas require you to close your account when moving money but others can be flexible, which lets you take money in and out of a cash Isa throughout the tax year until you find a rate you are happy with, without affecting your allowance.

Should you open an Isa or a savings account?

Choosing between a cash Isa and savings account will depend on your needs and savings goals.

The rates on a cash Isa tend to be slightly lower than savings accounts, although you get the tax-free status. Both types have best buys at around 5pc.

It is more tax efficient to use a cash Isa for the tax-free returns, especially if you are a higher rate taxpayer as you have a lower personal savings allowance.

But basic-rate taxpayers may benefit from more choice if they can also make use of the personal savings allowance as they can see if a cash savings account or cash Isa suits them better.

Isa and savings rates can change though and you may not always get the initial rate you are on, especially when your fixed deal ends or if you have a variable rate.

Alternatively, stocks and shares Isas typically outperform a savings account and cash Isa over the long-term and provide tax-free inflation-beating returns.

Rachell Springall, of analyst Moneyfacts, said: “Cash Isa could be a better option, particularly for higher-rate taxpayers with a large nest egg.

“The longer-term tax-free wrapper is the benefit of a cash Isa, protecting returns regardless of interest rate rises. Despite its introduction in April 2016, the personal savings allowance limits have not been increased and interest rates are much higher.”

Sarah Coles, of stockboker Hargreaves Lansdown, said the benefits of a cash Isa don’t start and end with the immediate tax saving.

She said: “If the frozen income tax thresholds mean pay rises push you into a higher tax bracket, the Isa will be more rewarding.

“Likewise, if you build your savings, you’ll be grateful for your Isa. A basic-rate taxpayer with £20,000 is marginally better off in the savings account in the first year. However, if this is their second year and they have more to save on top of last year’s £20,000, they’ll be better off with the Isa – and they’ll wish they’d secured last year’s Isa allowance too.”

Ms Coles added that Isas can be very useful for providing some income in retirement.

She said: “If you’re using interest from a savings account to boost your overall income, the frozen tax thresholds mean there’s a risk it will push you into a new tax bracket, so you pay a higher rate of tax. By taking interest from an Isa, this portion of your income will be tax-free, so you can take a pension income up to a threshold, and Isa income on top.”