Yahoo Finance

Yahoo Finance JPMorgan’s Risk Swap Ends Up at a Familiar Place: Rival Banks

(Bloomberg) -- When JPMorgan Chase & Co. arranged a series of trades to shift the risk of losses from $20 billion of its loans, some of those dangers wound up at a familiar place: rival banks.

Most Read from Bloomberg

US Inflation Broadly Cools in Encouraging Sign for Fed Officials

Blinken Casts Doubt on Cease-Fire Hopes After Hamas Responds

Hunter Biden Was Convicted. His Dad’s Reaction Was Remarkable.

Britain’s ‘Quiet Quitters’ Are Costing the Economy £257 Billion

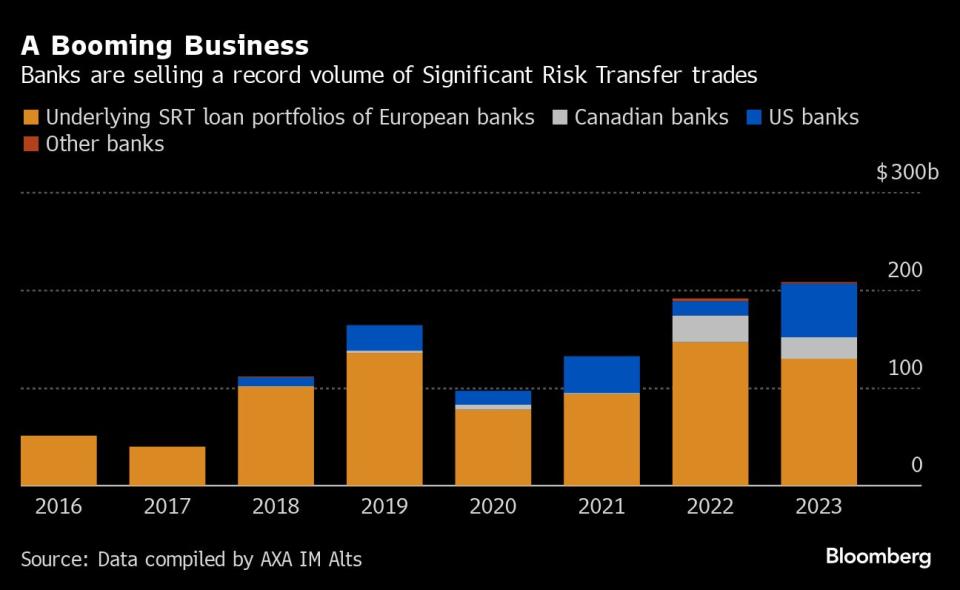

The deal, struck late last year, was one of the biggest ever Synthetic Risk Transfer trades, or SRTs, opaque transactions heralded by Wall Street and approved by regulators that are supposed to hand possible loan losses to hedge funds and other nonbank investors. Yet some buyers in the JPMorgan deal — and in multiple other SRT trades — borrowed money from other banks to help finance their stakes and inflate returns, people familiar with the matter say.

Nomura Holdings Inc., Morgan Stanley and NatWest Group Plc, have emerged as some of the most active lenders to investors in SRTs, along with rivals including Banco Santander SA and Standard Chartered Plc. That leaves them well-placed to profit from an expected surge in the deals — but exposed to potential losses if debts end up going bad and the SRT investor hits trouble.

The lurking presence of Wall Street loans behind some of these complex trades suggests exposures that were meant to be shifted elsewhere remain tied to the banking system, an outcome that’s starting to spook regulators.

“If a bank’s lending against the SRT instrument as collateral, you’re clearly not transferring the risk outside the banking system,” says Sheila Bair, who led the Federal Deposit Insurance Corp. during the financial crisis. “Any counterparty investing in SRT using bank-provided leverage should be prohibited, full stop.”

Spokespeople for the banks declined to comment.

On the JPMorgan deal, DE Shaw & Co. and LuminArx Capital Management were among investors that used leverage, according to people with knowledge of the transactions. Both firms declined to comment.

Banks issued about $25 billion of SRTs in 2023, partially offloading the risk of $300 billion of loans, according to an estimate from Pemberton Asset Management. Market participants surmise that anywhere between 10% and 50% of the money for these deals could be borrowed, although it’s impossible to be certain given the private bilateral nature of such loans.

The US Federal Reserve is “very focused on this topic,” says Kaelyn Abrell, partner and portfolio manager at ArrowMark Partners. “They want to make sure if a bank issues an SRT it doesn’t just end up transferring risk between banks.”

Synthetic Craze

Although common in Europe for years, the craze for this generation of synthetic bonds only really took off in the US in 2023, when Wall Street was figuring out ways to get ahead of tighter Basel III capital rules. Once the Fed provided some guidance and approved several SRT trades, banks such as Wells Fargo & Co. started reaching out to investors to put together their own deals.

JPMorgan’s sale late last year, which transferred the loan risk in the form of $2.5 billion of synthetic bonds, took things up a notch. Douglas Charleston at TwentyFour Asset Management describes it as a “landmark” given its scale. Other buyers included Blackstone Inc. and Dutch pension fund PGGM NV, people familiar say. JPMorgan and the investors declined to comment.

Through the use of so-called “credit-linked notes,” which include a kind of financial insurance known as a credit-default swap, big banks use SRTs to sell the risk of loan losses to investors without having to offload the debt themselves. The notes often bring together pools of loans such as revolving-credit facilities for companies or leveraged loans used on private equity buyouts, as well as mortgages or car debt. Policymakers have been broadly supportive, especially in the euro zone.

As US banks have started ramping up SRT issuance, luring investors with sometimes double-digit returns, firms such as Ares Management Corp., Blackstone and Magnetar Capital have jumped in. Hedge funds have been very active in European deals for years, but private credit firms awash with cash are becoming keen buyers in the US, too.

To help pay for these trades, some firms will seek outside financing. Hedge funds usually do so through a class of bank lending known as repurchase agreements, or “repos,” in which the lender takes the investing fund’s SRT securities as collateral, according to people with knowledge of the practice.

Others use different types of bank borrowing such as net asset-value — or NAV — loans, a kind of financing popular with private equity firms that’s secured against a portfolio of their holdings. To back its JPMorgan deal, LuminArx used a non-repo form of borrowing, a person familiar with the matter says.

While European SRT buyers haven’t used much leverage in the recent past, the trade’s economics are different on the other side of the Atlantic where borrowed money is often needed to deliver stellar returns. “Leverage in various forms has been employed by most investors” on recent US SRT deals, says Alan Shaffran, senior portfolio manager at Magnetar.

European and Canadian SRTs are commonly made up of only the riskiest portion of a bank’s loans, which offers the best returns. But the US equivalents are broader — or “thicker” — because the buyers have to insure larger portions of the debt, meaning the securities they buy yield less. That creates an incentive to use borrowed money to juice profit.

If an investment fund just uses its own cash for a US SRT trade, it can make loss-adjusted returns in the high single digits, market participants say. When the booster shot of leverage is added, returns can jump to the mid-teens.

“In the US we’re seeing thicker tranches on potentially higher quality portfolios and the net effect is much lower coupons,” Jason Marlow, a Barclays Plc managing director who manages its Colonnade SRT programme, said at a conference in Barcelona last week. “So different forms of leverage are necessary.”

Repo Rewards

A sustained surge in SRTs would be lucrative for Nomura, Morgan Stanley and other banks that specialize in lending on these deals. They can typically provide up to 60% of the value of a trade through repo financing, people with knowledge of the matter say.

However, seasoned market players fret about potential perils from borrowing on US deals, especially repo finance. “We don’t use repo leverage that could expose our funds or investors to margin calls,” says Richard Robb, chief executive officer of Christofferson Robb & Co., a New York investment firm that was among the first to buy SRTs. “We’ll leave that risk for the other guy.”

In a recent paper, several securitization experts including Georges Duponcheele at Great Lakes Insurance and Jeremy Hermant, until recently head of capital markets at Allica Bank Ltd., warned that if riskier loans in an SRT turned sour that would trigger margin calls — a demand for more collateral — from lending banks. If a borrower had to foreclose, the lender would end up “holding illiquid junior tranches in SRT trades,” they wrote.

An overarching worry is the mismatch between repo — shorter-term lending where banks regularly mark the asset price to market — and SRTs, which are by nature hard to value because there isn’t much buying and selling of the securities. “Usually in those repos, the banks are free to mark in the way they want,” says Deborah Shire, deputy head of AXA IM Alts in Paris, giving them a large degree of control over borrowers.

Investors are pushing back, asking bank lenders to be more forgiving on how they mark the SRT loans to market. But the more power they wrestle back, the more exposed the banks will be if things go wrong.

That’s a challenge for regulators, who’d bought into the idea that SRTs are a societal good because “risk is leaving the banking sector,” according to Alec Innes, cohead of financial risk and resilience at KPMG LLP, who advises banks worldwide.

“My personal preference is not to see material growth in the repo market,” Marlow at Barclays concludes, arguing that it’d be better to find other ways of hitting returns targets “without introducing more systemic risk.”

--With assistance from Laura Benitez and Neil Callanan.

(Updates with quote in penultimate paragraph.)

Most Read from Bloomberg Businessweek

China’s Economic Powerhouse Is Feeling the Brunt of Its Slowdown

As Banking Moves Online, Branch Design Takes Cues From Starbucks

Food Companies Hope You Won’t Notice Shortages Are Raising Prices

The World’s Most Online Male Gymnast Prepares for the Paris Olympics

©2024 Bloomberg L.P.