Yahoo Finance

Yahoo Finance Kelsian Group And Two Other ASX Stocks That Could Be Trading Below Their Estimated Value

The Australian stock market has experienced a period of stability over the last week, maintaining its position after achieving a 9.8% increase over the past year, with earnings expected to grow by 13% annually. In this environment, identifying stocks that may be trading below their estimated value could offer attractive opportunities for investors looking to capitalize on potential growth.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

Name | Current Price | Fair Value (Est) | Discount (Est) |

GTN (ASX:GTN) | A$0.435 | A$0.85 | 48.6% |

Ansell (ASX:ANN) | A$25.59 | A$49.32 | 48.1% |

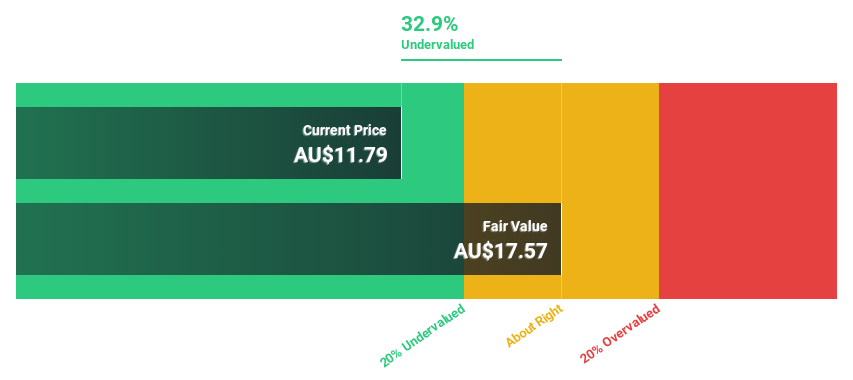

Elders (ASX:ELD) | A$8.59 | A$16.28 | 47.2% |

Credit Corp Group (ASX:CCP) | A$14.13 | A$25.33 | 44.2% |

Australian Clinical Labs (ASX:ACL) | A$2.41 | A$4.69 | 48.6% |

hipages Group Holdings (ASX:HPG) | A$1.06 | A$2.05 | 48.4% |

IPH (ASX:IPH) | A$6.20 | A$11.96 | 48.2% |

ReadyTech Holdings (ASX:RDY) | A$3.27 | A$6.22 | 47.5% |

Millennium Services Group (ASX:MIL) | A$1.145 | A$2.24 | 48.9% |

SiteMinder (ASX:SDR) | A$4.99 | A$9.96 | 49.9% |

Let's dive into some prime choices out of from the screener.

Kelsian Group

Overview: Kelsian Group Limited operates in the provision of land and marine transport and tourism services across Australia, the United States, Singapore, and the United Kingdom, with a market capitalization of approximately A$1.34 billion.

Operations: The company generates revenue through three primary segments: Australian Bus operations at A$934.76 million, International Bus services at A$448.87 million, and Marine and Tourism activities contributing A$337.90 million.

Estimated Discount To Fair Value: 22.9%

Kelsian Group, valued at A$4.99, trades 22.9% below its estimated fair value of A$6.47, signaling potential undervaluation based on discounted cash flow analysis. Despite a decrease in net profit margin from last year and challenges in covering interest payments with earnings, Kelsian is poised for significant earnings growth, forecasted at 25.85% annually over the next three years—outpacing the Australian market's expectation of 12.9%. However, its dividends are poorly backed by earnings and free cash flows.

Megaport

Overview: Megaport Limited offers elastic interconnection services across multiple regions including Australia, New Zealand, Hong Kong, Singapore, Japan, North America, and Europe, with a market capitalization of approximately A$1.86 billion.

Operations: The company generates revenue from three primary geographical segments: Europe (A$28.88 million), Asia-Pacific (A$48.84 million), and North America (A$99.78 million).

Estimated Discount To Fair Value: 40.2%

Megaport, priced at A$11.63, is considered undervalued with a fair value estimate of A$19.44 according to discounted cash flow analysis, suggesting a 40.2% undervaluation. Recent strategic alliances, including partnerships with Aviatrix and Lufthansa Systems, enhance its position in multicloud connectivity crucial for regulated industries. Despite slower revenue growth forecasts (16.3% annually), Megaport's earnings are expected to surge by 34.72% annually over the next three years, outperforming the broader Australian market growth projections.

Nanosonics

Overview: Nanosonics Limited is an infection prevention company operating both in Australia and internationally, with a market capitalization of approximately A$927.17 million.

Operations: The company generates its revenue primarily from the healthcare equipment segment, totaling approximately A$164.07 million.

Estimated Discount To Fair Value: 40.7%

Nanosonics, trading at A$3.06, appears undervalued based on a discounted cash flow valuation of A$5.16, reflecting a significant discount. While its revenue growth is projected at 9.9% annually, slower than some market segments but faster than the Australian average of 5.3%, earnings are expected to increase by 23% per year, outpacing the market's 12.9%. However, its forecasted Return on Equity in three years is relatively low at 12.6%, tempering some optimism around its growth prospects.

Seize The Opportunity

Take a closer look at our Undervalued ASX Stocks Based On Cash Flows list of 52 companies by clicking here.

Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Seeking Other Investments?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ASX:KLSASX:MP1 and

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com