There Is Light at the End of the Tunnel for Alibaba

Shares of Alibaba Group Holding Ltd. (NYSE:BABA) seem to have begun a bottoming out process after trading near lows between $55 and $80 for some time. Nevertheless, now at $85, shares are still down 72.40% from their peak in 2020, when shares were $308 per share.

While we would expect a company with this kind of price action to have seen its fundamentals crumble, we believe the opposite is happening with Alibaba, as we see great future prospects as the underlying fundamentals have recently stabilized. In addition to stabilizing its results and certain headwinds abating such as currency exchange rate fluctuations, Alibaba seems to have a lot of future prospects to look forward to, with Alibaba Cloud showing strong growth in both top and bottom-line results. Overall, we explain why Alibaba is an exception in the Chinese landscape and not a value trap, and why the current valuation of 6.48 times enterprise value/adjusted Ebitda is likely far too low for a quality company like Alibaba.

On the other hand, we also cover some of the serious risks the company faces at the macroeconomic level and the risks it, along with its Chinese competitors, could face. We also discuss how much upside potential we see for Alibaba and what a reasonable valuation would look like.

There is a light at the end of the tunnel

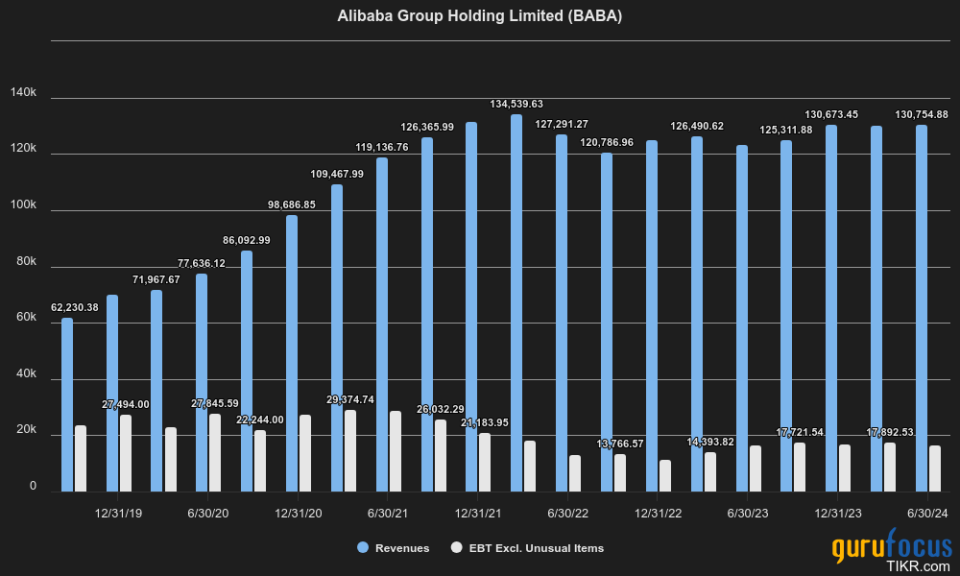

On a fundamental level, looking at Alibaba's second-quarter earnings, it seems like both top and bottom-line results have started showing a clear signal that they are stabilizing. Looking at revenue and earnings before taxes on a trailing 12-month basis in dollar terms, Alibaba clearly was hit in 2022 by adverse circumstances ranging from exchange rate headwinds to competitive and regulatory pressures as well as a very tough macroeconomic backdrop.

However, it does seem like there is finally light at the end of the tunnel, as exchange rate pressures have started to abate and competitive pressures have seemingly begun to ease. Revenue increased 5.70% year over year on a trailing 12-month basis to $130.75 billion, compared with $123.67 billion in the second quarter of last year. Alibaba's core earnings are also starting to stabilize, coming in at $16.64 billion on a trailing 12-month basis, looking at profit before tax and unusual costs, up just 0.54% from last year. We see these results as positive as investors have finally gained some clarity on the long-term outlook for Alibaba over the past quarter, after revenue and bottom-line unexpectedly contracted on a dollar basis in 2022 and growth faltered from high double-digits to nearly zero.

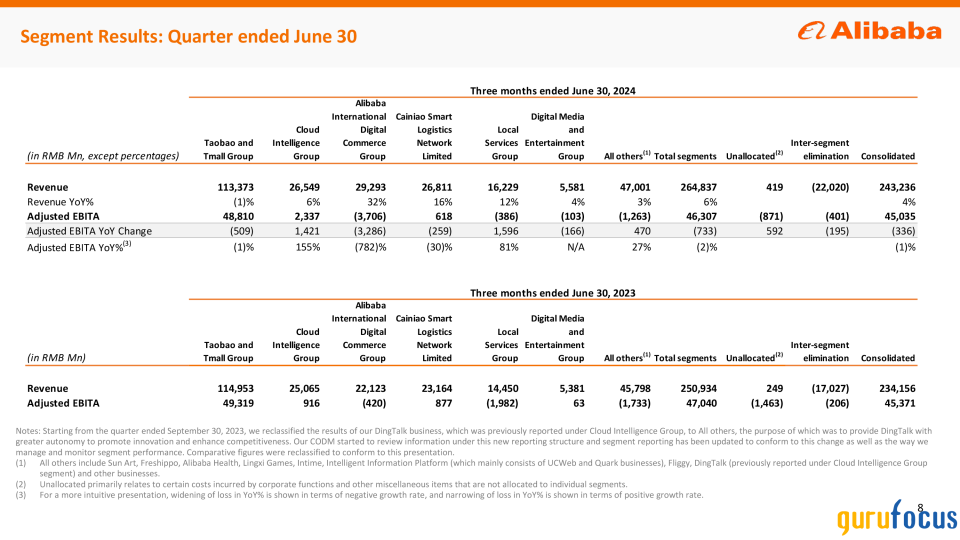

Looking at Alibaba's various business segments, its bread and butter still remains the Taobao/Tmall Group, where revenue remained largely flat and contracted slightly from 114.95 billion yuan ($16.30 billion) to 113.37 billion yuan, similar to adjusted Ebita, which went from 49.32 billion yuan to 48.81 billion yuan. The most notable changes occurred in the Alibaba Cloud & Alibaba International Digital Commerce (AIDC) Group, where revenue grew 6% and 32% year over year. Alibaba Cloud really shone this quarter by further increasing its margins and growing adjusted Ebita from 916 million yuan to 2.34 billion yuan.

The AIDC segment, however, saw adjusted Ebita sink from -420 million yuan to -3.29 billion yuan, which management said was due to the increase in investments in AliExpress and Trendyol's cross-border business, partly offset by Lazada's significant reduction in operating loss from the improvements in its monetization and operating efficiency, as quoted directly from the latest earnings call.

Alibaba reportedly earned 51.16 billion yuan in adjusted Ebitda, including depreciation and amortization, compared with the previously mentioned figures. Keep in mind, however, that Alibaba makes adjustments for things like non-cash share-based compensation and a provision for class-action lawsuits against shareholders. We believe that while it is justified to exclude the latter from adjusted Ebitda, we will henceforth deduct non-cash share-based compensation as it is dilutive to shareholders anyway. This gives us a figure of 47.05 billion yuan or $6.47 billion in adjusted EBITDA for the second quarter, or an impressive $25.88 billion on an annualized basis.

We believe Alibaba's valuation could actually be higher than this if we include only the profitable business segments, as it in theory should be able to wind down non-profitable segments in the long run. Including Taobao/Tmall Group, Cloud Intelligence Group, Cainiao and the unallocated/ inter-segment elimination, we arrive at an Ebita of 50.49 billion yuan. If we add depreciation and amortization and subtract non-cash share-based compensation, we arrive at 52.51 billion yuan or $7.23 billion adjusted Ebitda. This means that on an annualized basis at a run rate of $28.92 billion, Alibaba is likely only trading at 6.93 times adjusted Ebitda.

Valuation ridiculousness

While it is already remarkable for a quality company like Alibaba to trade at only 6.93 times adjusted Ebitda, even in times of turbulence, the company gets even cheaper when we take into account its huge cash and short-term investments of $61.77 billion.

To calculate Alibaba's enterprise value, we add $33.04 billion of total debt and subtract $61.77 billion of cash and short-term investments from its $200.38 billion market cap. After also adjusting for minority interests of $15.87 billion, we are left with an enterprise value of only $187.52 billion. At $28.92 billion adjusted Ebitda, Alibaba is only trading at what we believe to be 6.48 times enterprise value/adjusted Ebitda. Also on a free cash flow basis, we see the company is extremely cheap, producing $17.44 billion over the past 12 months. In other words, Alibaba is only trading at 11.49 times price-to-free cash flow.

Even after adjusting for $2.55 billion of stock-based compensation, Alibaba would still generate $14.89 billion of adjusted free cash flow or trade at 13.46 times adjusted free cash flow. Along those lines, we can look at what the dividend yield would be for Alibaba if it used all of its free cash flow to return capital to shareholders. At a multiple of 13.46, this would amount to an impressive return of 7.43%, and this is while we believe the company is still experiencing growth and investing heavily in innovative projects such as artificial intelligence infrastructure. This is also why free cash flow has been lower recently, given the large capital expenditure that has gone to Alibaba's AI infrastructure.

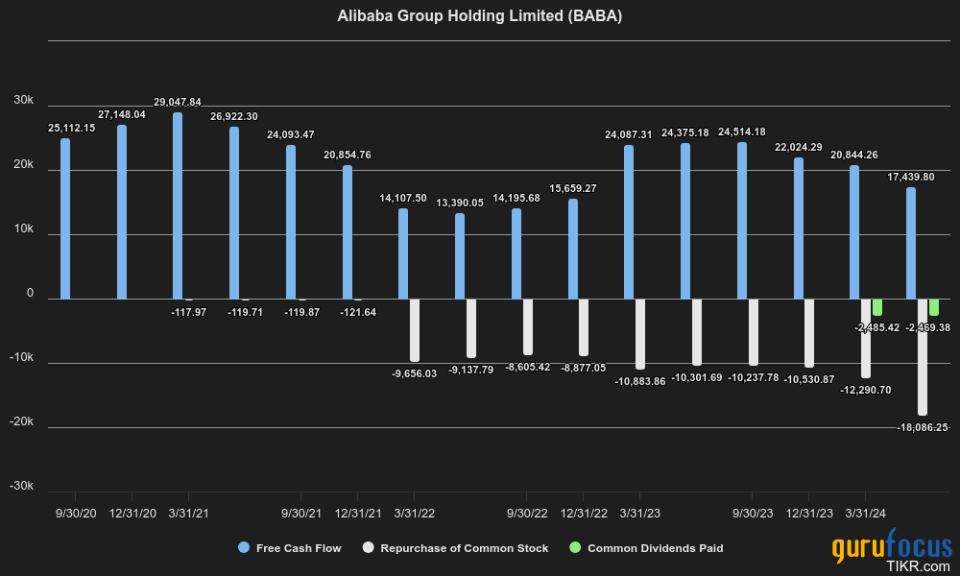

The biggest positive development we have actually noticed at Alibaba has to do with the company sticking to its promise to return capital to shareholders. Alibaba has long been, and perhaps still is, seen as a value trap by many because it traded at an incredibly low valuation but did not return enough of this capital to shareholders, which we believe was largely due to China's restrictive policies when it comes to capital outflows and protecting its currency, the Chinese yuan, which has become quite weak in recent years.

In contrast to other Chinese company, Alibaba has used virtually all of its free cash flow over the last few quarters to return capital to shareholders via buybacks and dividends, as can be seen in the graph above. On a trailing 12-month basis, Alibaba even used some of its balance sheet to return money to shareholders, returning a whopping $20.56 billion to shareholders in both dividends and share repurchases. In addition, the company said in its second-quarter earnings call it has $26.10 billion left of its current share repurchase program:

"As of June 30, 2024, we had 90 billion ordinary shares or approximately $2.4 billion ADSs outstanding. Compared to March 31, 2024, there was a 2.3% net reduction in our outstanding shares after accounting for shares issued in our ESOP. As of June 30, 2024, we still have $26.1 billion remaining in our share repurchase program."

In a sense, we do not see Alibaba being a value trap anymore looking at these metrics, meaning the low valuation must be largely due to competitive and macroeconomic pressures, which we believe it has been navigating quite successfully. We believe that Alibaba, despite all pressures, should at least be trading at 12 times enterprise value/Ebitda, which would be a $347.04 billion Enterprise Value or a $359.9 billion market cap. This would translate into a $149.96 share price, or 79.38% upside.

The gloomy macroeconomics

Taking all these positive developments aside, we do have a serious note on the possible risks to our thesis. Firstly, while Alibaba's results have stabilized, we cannot rule out that increased competitive pressures, especially from JD.com (NASDAQ:JD) and Pinduoduo (NASDAQ:PDD) may continue to weigh down on Alibaba's results, especially in the international domain, where we believe AliExpress faces some serious competition from PDD's Temu.

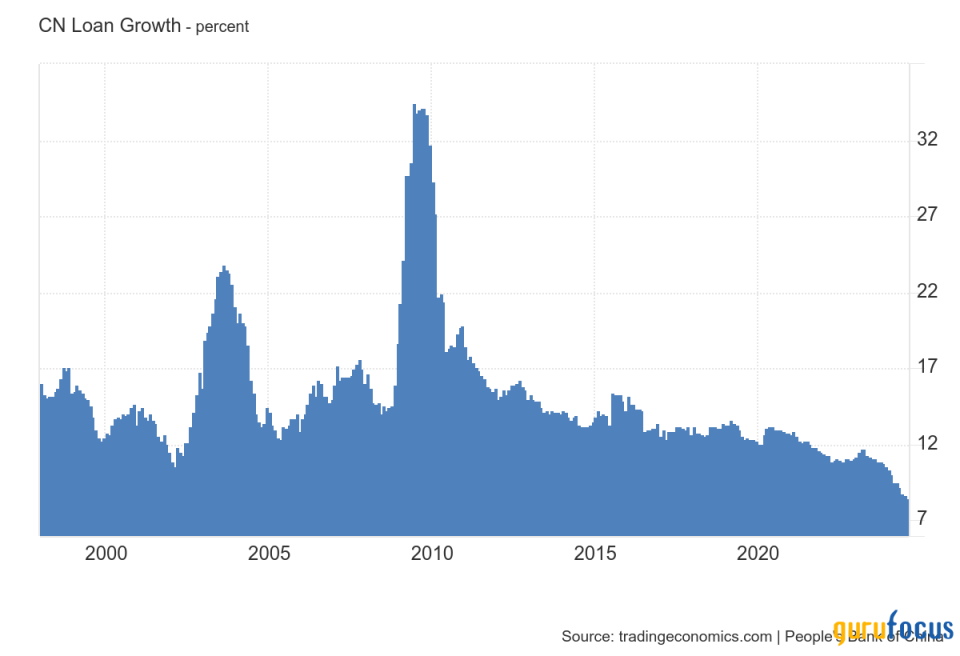

Especially in bad macroeconomic times, with consumers ordering increasingly lower ticket items, could favor players like PDD. Speaking of macroeconomic data, we see macroeconomic headwinds as the most important threat to Alibaba's business currently, given its massive reach and gross merchandise volume. Looking at some signals, they all point to a very gloomy future, with CNY Loan Growth, for example, continually falling to new all-time lows, currently at 8.50% year over year versus previous decades where growth was well into the double digits.

We think China is currently facing a deflationary spiral, similar to the one in Japan in the late 1980s and early 1990s. We see the Chinese economy is currently facing a very heavy debt burden, especially in terms of private debt, but also public debt at the local government level. Currently, banks are reluctant to lend to companies because these companies themselves prioritize paying off existing loans to reduce their debt burden. The above catalysts, in our opinion, make it so that China currently faces an economy where domestic demand is too weak, and the trade balance is already too large to increase exports for political reasons.

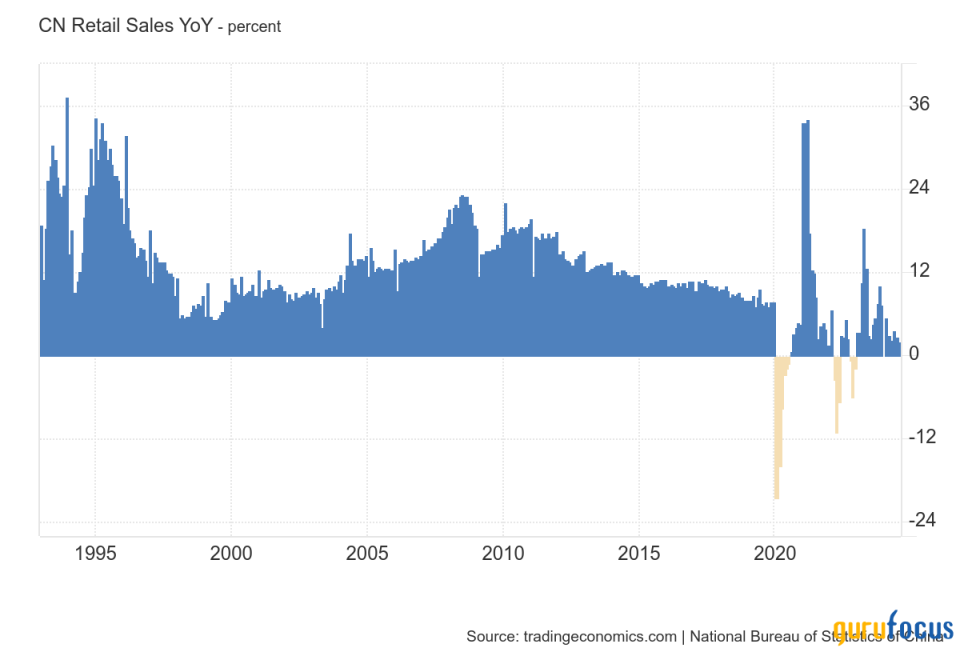

In short, it remains to be seen when and if the Chinese government will come to the rescue with fiscal support to help China out of this deflationary spiral. Importantly for Alibaba, Chinese retail sales were 2.10% year-over-year, far lower than the historical trend and coming in below expectations which were set at 2.50% year-over-year growth.

Other signals, such as changes in home prices year-over-year, inflation and producer price index all signal a very gloomy outlook, coming in below expectations and remaining far below its pre-2020 trend. Regarding Alibaba, we would be on the lookout for any announcement from the Chinese government regarding any potential future fiscal stimulus, as we believe it definitely would materially impact its results.

Conclusion

Although the macroeconomic outlook for China and thus Alibaba remains very bleak, we believe there is light at the end of the tunnel as the company is currently undervalued at 6.48 times EV/adjusted Ebitda.

We also do not see Alibaba as a "value trap" because it returns more than enough capital to investors compared to some other Chinese companies. Even from a free cash flow perspective, amid increased capital expenditures, we estimate the actual free cash flow return to investors to be around 7.43%. This is unusually cheap, especially for a quality company like Alibaba, which is the fourth-largest cloud provider in the world. We believe that if Alibaba were an American company, it might be trading at similar valuations to its American big tech counterparts of over 30 times forward earnings.

In conclusion, we think Alibaba could get at least a 12 times EV/Ebitda multiple, after which we believe the shares could trade north of $150 per share, representing nearly 80% upside over current prices.

This article first appeared on GuruFocus.