Yahoo Finance

Yahoo Finance We Take A Look At Why Seeing Machines Limited's (LON:SEE) CEO Compensation Is Well Earned

The performance at Seeing Machines Limited (LON:SEE) has been quite strong recently and CEO Paul McGlone has played a role in it. The pleasing results would be something shareholders would keep in mind at the upcoming AGM on 28 November 2022. The focus will probably be on the future company strategy as shareholders cast their votes on resolutions such as executive remuneration and other matters. Here is our take on why we think CEO compensation is not extravagant.

See our latest analysis for Seeing Machines

Comparing Seeing Machines Limited's CEO Compensation With The Industry

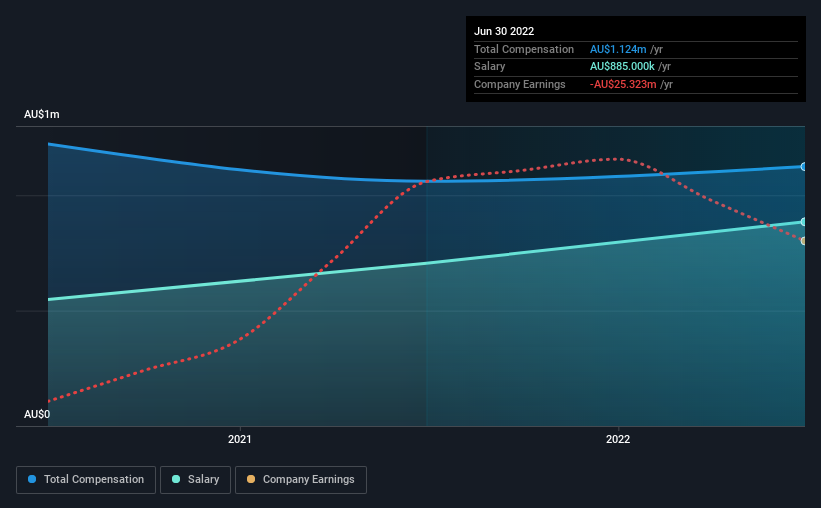

At the time of writing, our data shows that Seeing Machines Limited has a market capitalization of UK£279m, and reported total annual CEO compensation of AU$1.1m for the year to June 2022. That's a fairly small increase of 5.9% over the previous year. In particular, the salary of AU$885.0k, makes up a huge portion of the total compensation being paid to the CEO.

In comparison with other companies in the industry with market capitalizations ranging from UK£168m to UK£671m, the reported median CEO total compensation was AU$1.1m. This suggests that Seeing Machines remunerates its CEO largely in line with the industry average.

Component | 2022 | 2021 | Proportion (2022) |

Salary | AU$885k | AU$705k | 79% |

Other | AU$239k | AU$356k | 21% |

Total Compensation | AU$1.1m | AU$1.1m | 100% |

On an industry level, roughly 75% of total compensation represents salary and 25% is other remuneration. There isn't a significant difference between Seeing Machines and the broader market, in terms of salary allocation in the overall compensation package. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

Seeing Machines Limited's Growth

Over the past three years, Seeing Machines Limited has seen its earnings per share (EPS) grow by 54% per year. Its revenue is up 15% over the last year.

Shareholders would be glad to know that the company has improved itself over the last few years. It's a real positive to see this sort of revenue growth in a single year. That suggests a healthy and growing business. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Seeing Machines Limited Been A Good Investment?

Most shareholders would probably be pleased with Seeing Machines Limited for providing a total return of 61% over three years. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

To Conclude...

Seeing that company performance has been quite good recently, some shareholders may feel that CEO compensation may not be the biggest focus in the upcoming AGM. Seeing that earnings growth and share price performance seems to be on the right path, the more pressing focus for shareholders at the AGM may be how the board and management plans to turn the company into a sustainably profitable one.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. We've identified 1 warning sign for Seeing Machines that investors should be aware of in a dynamic business environment.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here