Yahoo Finance

Yahoo Finance M&S chairman warns Labour over employment rights reforms

The chairman of Marks & Spencer has warned that Britain risks being unable to attract investment if a Labour election victory results in an overhaul of worker rights.

Archie Norman said the UK’s biggest problem was a “lack of growth in productivity and investment” going into a general election this year, with Labour predicted to win a landslide victory according to most polling.

Mr Norman said: “Any incoming government should consider carefully whether a package that reduces flexibility, makes it more costly to hire people, and seeks to bring unions back into the workplace will help attract new investment.”

The former Conservative MP said the country already has “some of the best employers, terms and practices in the world”.

He added: “Of course there are exceptions but in a knowledge-based economy most businesses are very focused on building motivated engaged workforces.”

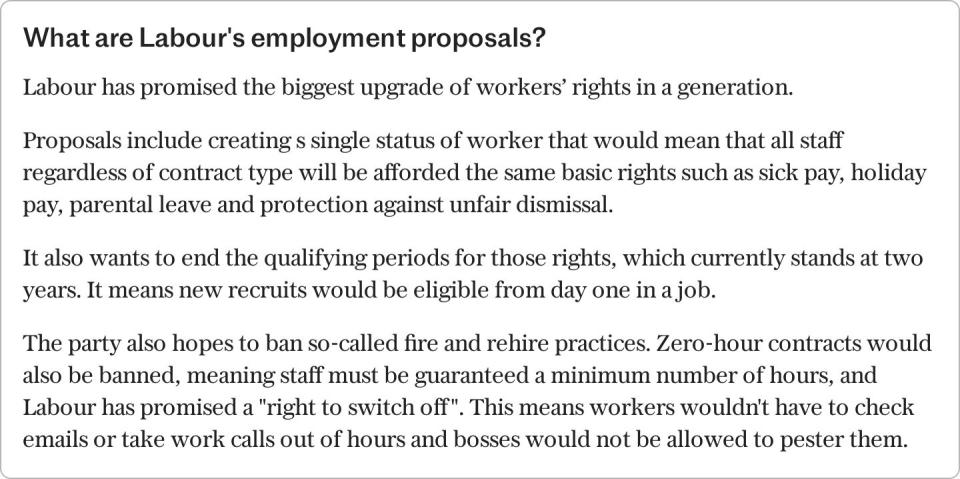

Labour has pledged to “strengthen workers’ rights and make Britain work for working for people” if it comes into power. This would include scrapping qualifying periods for full employment rights, getting rid of the gig economy and giving staff the right to claim unfair dismissal on day one of a new job.

Labour is ramping up its charm offensive with business leaders amid fears that a lack of clarity on its employment reforms is preventing it from winning support from industry.

Mark Carney, the former Bank of England governor, and Barclays chief executive C S Venkatakrishnan are among the influential leaders now working with the party to unlock billions of pounds in investment.

One Labour insider admitted party officials had “not done a great job of being super clear” with business on its workers rights reforms.

They added: “This is a core part of our economic offer, it’s not something we want to hide in a cupboard.

“Investors are still ringing us every week, those looking at an IPO want to know what we think. The idea that Labour could damage investment is just for the birds.”

Senior Labour officials plan to meet major business lobby groups including the Confederation of British Industry (CBI) over the coming weeks to discuss concerns about its workers rights. Feedback so far has been a “mixed bag”, the insider said.

Lobbyists have been urging Labour to tread carefully with their changes. Rupert Soames, the president of business group the CBI and Winston Churchill’s grandson, has cautioned against adopting a “European model” of employment and told CBI members to “wake up, smell the coffee – this is a major thing that’s coming up”.

Sir Keir Starmer has said that Labour would overhaul the system on a scale which has “not been attempted for decades”.

Business leaders have raised the alarm over whether “day one” rights could effectively mean the end of probation periods.

Alex Baldock, the boss of electrical retailer Currys, told The Telegraph last month that he would be “very loath” to see probationary periods axed. He warned that Labour’s plans risked “making people inadvertently poorer”, adding: “The more restrictions that you put in place, the less flexibility you allow in businesses’ relationships with their colleagues, the less likely businesses are to hire and the less likely they are to invest.”

Labour has sought to ward off concerns and insists that its changes will not end probation periods and are designed to make workplace rights “fit for a modern economy”.

Jonathan Reynolds, the shadow business secretary, hit out at Mr Norman’s comments, criticising the Conservative government for “presiding over a high tax, low growth economy”.

He added: “Business leaders aren’t asking for a watering down of workers’ rights. They want the policy certainty they need to make long-term investments, stable corporation tax, reform of business rates and action on late payments. That is what they will get with Labour.”

The warning from Mr Norman comes after years of stagnating business investment in the UK. According to official figures, business investment has grown by around 6pc in real terms between the middle of 2016 and the end of 2023. This compares to growth of more than 25pc in the US.

The Office for Budget Responsibility (OBR) last year said that “uncertainty surrounding the UK’s future trading relationship with the EU, the pandemic, the energy crisis, and rises in the post-tax cost of capital [were] all weighing on investment decisions.”

It added that under-investment has weighed on productivity, which has grown at less than half its pre-financial crisis rate since 2010. The UK lags France, Germany and the US for productivity.

Recommended

Inside Labour's plan for a storm of regulations at work