Yahoo Finance

Yahoo Finance Magna (MGA) Hits 52-Week Low: Should You Still Hold the Stock?

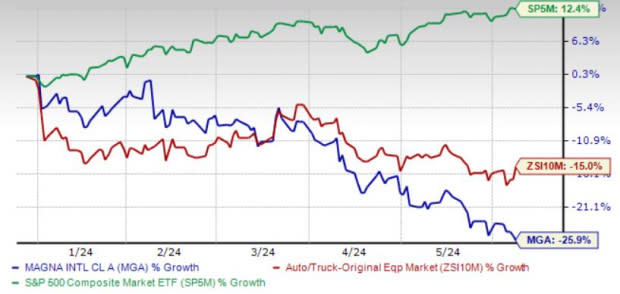

Shares of auto equipment supplier Magna International MGA slipped to a 52-week low of $43.44 per share in the last trading session on June 7, before closing a tad bit higher at $43.76. Year to date, Magna has lost 26% of its value, underperforming the industry’s decline of 15%. Meanwhile, the S&P 500 index has risen 12.4% over the same timeframe.

Image Source: Zacks Investment Research

What’s Dragging Down MGA Stock?

Investors seem to be disappointed with the company’s earnings miss in the last two quarters and a bleak full-year sales outlook.

Weak Q1 Results: Magna reported first-quarter 2024 adjusted earnings of $1.08 per share, which declined from the year-ago quarter’s $1.11 per share and also missed the Zacks Consensus Estimate of $1.28. Sales, although inching up 2.7% year over year, fell short of the consensus mark. Free cash flow was negative $270 million in the quarter as the company continues to invest heavily in the development of technologically advanced products. While that would indeed create new opportunities for the firm, it is likely to strain near-term cash flows and financials.

2024 Sales Guidance Cut: Magna has made a downward revision in its 2024 sales outlook, citing the absence of additional Fisker Ocean production, program delays and changes in product mix. It now expects full-year 2024 revenues in the band of $42.6-$44.2 billion, down from the previous guidance of $43.8-$45.4 billion. One major setback is the halted production of Fisker Ocean, expected to impact 2024 sales by approximately $400 million and reduce the adjusted EBIT margin by 25 basis points.

Magna’s Long-Term Prospects Encouraging

Despite near-term challenges, Magna is well-positioned for long-term growth on the back of several catalysts.

A broad range of product and service offerings coupled with a focus on innovation in electrification and autonomous driving augur well for the long term. The company expects these areas to add more than $4 billion in sales within three years, with a projected 50% CAGR from 2022 to 2027.

Magna’s portfolio strength is evident from recent business wins, including front camera modules, battery enclosures, and eDrive systems with global OEMs.

Additionally, Magna's acquisition of Veoneer's Active Safety business has bolstered its ADAS segment, aiming for more than $70 million in annual savings by 2025.

To mitigate economic pressure, Magna has undertaken consolidation, restructuring, and cost-saving measures, maintaining its adjusted EBIT margin outlook in the range of 5.4-6%.

Magna’s balance sheet is strong, with $4 billion in liquidity and a manageable debt-to-capitalization of 34%. The company has investment-grade ratings from S&P and Moody’s.

Its commitment to shareholder returns is demonstrated by nine dividend increases in the past five years, achieving a 5.55% annualized growth rate. The company’s annual dividend yield is more than 4%.

MGA Stock Holds Promise

Despite global EV sales growth, the pace has slowed in 2024, prompting North American OEMs to update their electrification strategies by deferring new programs and reducing production shifts. Consequently, MGA is expected to face challenges in recovering pre-production, tooling, and engineering costs within the anticipated timeframe. A slashed sales outlook for the current year has indeed spooked investors. But MGA’s long-term narrative is still strong.

From a valuation standpoint, MGA is trading cheaper than the industry. If we look at the price/earnings ratio, the company shares currently trade at 6.91 forward earnings, well off its five-year high of 21.36 and below the median of 9.80. The company carries a Value Score of A.

Image Source: Zacks Investment Research

Out of the 18 brokers covering MGA stock, seven have Strong Buy recommendations and 11 have Hold Rating, giving the company an average broker recommendation (ABR) of 2.22.

As the stock has dipped significantly this year, the Zacks average price target of $59.06 is 33.7% above the current levels.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Magna's 2024 sales and EPS implies year-over-year growth of 2% and 6%, respectively. The consensus mark for 2025 sales and EPS points to another 4% and 20% uptick, respectively, from the estimated 2024 projections.

We think that it's prudent to hang on to this Zacks Rank #3 (Hold) stock as of now. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Magna International Inc. (MGA) : Free Stock Analysis Report