Yahoo Finance

Yahoo Finance Market rally continues as China eases trade tensions: as it happened

European indices rally for second day after China offers olive branch on trade

Pound wobbles as battle over Brexit intensifies

Micro Focus faces axe from FTSE 100 after shock shares slump

Garry White: Donald Trump is losing the trade war with China

Wrap-up: Europe takes gains while it can after mad month

August is known for its volatility, but the tumult of the past month was quite something to see.

Global markets were rattled at the start of the month after US president Donald Trump announced ramped-up tariffs against China, sparking a back-and-forth of retaliatory responses.

Investors spent the month fighting a rearguard action, broadly swinging towards safe-haven assets such as gold and bonds, while dipping back into equities whenever it appeared the coast was clear.

We saw two contractions (the UK and Germany), a yield curve inversion, tariff battles and continued upheaval in Hong Kong.

From Monday, thing should return to more of a sense of normality, but there will still be two spectres hanging over the market: Brexit, and the beginning of new tariffs between the US and China. We’ll have to wait and see how both develop.

That’ll all from me today. I’ll be back on Monday with the latest business, markets and economics news. Have a good weekend!

Euro storm continues

The euro is shedding further against the dollar, now down to $1.0991 — plunging further into lows not seen since early 2017.

Euro in free fall. Plunges below $1.10, lowest since May 2017 w/ Trump pouring oil on the fire. pic.twitter.com/NgdtBewKsN

— Holger Zschaepitz (@Schuldensuehner) August 30, 2019

Active FX specs are heavily short USD as it rages higher. This is going to blow some accounts up. pic.twitter.com/7SiDa4QNfF

— Brent Carlile (@BrentCarlileFX) August 30, 2019

Here’s where European markets ended up

The FTSE 100 closed up 0.32pc, or 22.86 points, at 7,207.18

The FTSE 250 closed up 0.52pc, or 101.13 points, at 19,393.63

France’s CAC 40 closed up 0.56pc, or 30.51 points, at 5,480.48

Germany’s DAX closed up 0.85pc, or 100.4 points, at 11,939.28

Spain’s IBEX closed up 0.21pc, or 18.6 points, at 8,812.90

Italy’s FTSE MiB closed down 0.35pc, or 75.27 points, at 21,322.90

FTSE suffers biggest monthly loss since October

Breaking: The FTSE 100 has suffered its biggest monthly loss since October after a storm of recession fears, Brexit uncertainty and trade tensions (–5.00pc August month-to-date according to Bloomberg).

The blue-chip index was within inches of a bigger drop (which would have taken it to its sharpest month fall since August 2018), but it gained around 0.3pc in the absolute final minute of trading, as funds adjusted their positions. That was a close one!

Euro falls below $1.10 for first time since May 2017

Widespread demand for dollars as the end of the month approaches has left Europe’s common currency at its lowest level since May 2017 against the US currency. It’s currently at about $1.098. Has Donald Trump created a self-fulfilling prophecy?

EURUSD below $1.10 handle. Trump can't be liking that!

— David Cheetham (@DavidCheetham3) August 30, 2019

Full report: Mortgage lending rises

Here’s Tim Wallace and Michael O’Dwyer with more on those mortgage lending figure from earlier today:

July was the biggest single month for mortgage lending since the eve of the financial crisis, while house prices inched higher over the summer, as the UK's sluggish housing market showed flickers of life.

More than £13bn of loans were offered by banks and building societies to movers last month, the highest total since September 2007, according to figures from the Bank of England.

You can read their full report here: Mortgage lending jumps to pre-crisis levels in July

Sterling rises...

...and the FTSE drops.

The Italian drop, combined with Mr Trump’s latest sabre-rattling against the Fed, have put a bit of a nervous twinge on things. There’s still an hour left of trading, however, a further shift is possible.

As a reminder, we might see some corrective twitches in the very final minutes as funds adjust their positions ahead of what is going to be a big week for British politics.

Italian stocks head into reverse after Di Maio warning

Uh oh. It looks like one of the week’s big comebacks might have come to an end.

Italy’s FTSE MiB is now around 0.35pc in the red, after Italy’s Five Star (MS5) party leader Luigi Di Maio warned the country could face fresh elections if an agreement cannot be reached on the programme of a new government.

MS5 is in negotiations with the Democratic Party (PD) over a power-sharing agreement that would maintain Giuseppe Conte as Prime Minister.

Senior PD lawmaker Graziano Delrio has said Mr Di Maio’s ultimatums are “really unacceptable”.

That has spooked investors, who want to avoid the uncertainty of fresh elections.

Italian spread widens as Di Maio says his program gets implemented or a new election is a better option.

Di Maio freaking out over Conte, his job and control for 5star. On top of that, add tensions with PD. It’s a boiling pot this government. #BTP— Maria Tadeo (@mariatad) August 30, 2019

Biggest fall in US consumer sentiment since 2012

Consumer sentiment in the United States fell by the biggest amount since 2012 in August according to a report by the University of Michigan, dropping to 89.2 from 92.1. Economist had been expecting it to stay steady. The gauge of current conditions hit its lowest level since October 2016.

The drop suggests trade headwinds are starting to weigh on the minds of regular consumers, as worries about increased levies made many think twice about key purchases. Sentiment over vehicle purchases was especially heavily-hit.

University of Michigan Survey August 2019

Sentiment: 89.8 -8.7%

Conditions: 105.3 -4.9%

Expectations: 79.9 -11.7%https://t.co/4yqgtqll9A$USD$SPX$TYX$TNXpic.twitter.com/MshhBQ9fXO— RT Economic Alerts (@RTFilings) August 30, 2019

Wall Street joins rally for second day

The top US stocks indices are all registering reasonable gains.

Donald Trump is taking the opportunity to push the Fed further for rate cuts:

....We don’t have a Tariff problem (we are reigning in bad and/or unfair players), we have a Fed problem. They don’t have a clue!

— Donald J. Trump (@realDonaldTrump) August 30, 2019

FACT CHECK: His claim that the dollar is “the strongest in history” is untrue with regards to both its price versus the euro and against a basket of currencies as measured by Bloomberg.

Canada stats put UK bottom of the G7 GDP growth pile

Canada’s solid growth figure means Britain was the worst-performing G7 economy during second quarter of the year (the three months to June).

The UK is alongside Germany at the bottom of the pile, with Europe’s second-largest and largest economies both contracting during the period. A further decline in the third quarter would put the countries into a technical recession.

Canada: Grew 0.9pc

United States: Grew 0.5pc

Japan: Grew 0.45pc

France: Grew 0.3pc

Italy: 0pc growth

Germany: Shrunk 0.1pc

UK: Shrunk 0.2c

There’s reason to believe the likelihood of a recession is slightly greater for Germany: analysts speculated that the UK might repeat the cycle it carried out in the first half of the year: three months of stockpiling-stimulated growth in the build-up to a Brexit deadline, followed by a subsequent quarter dictated by whatever happens at the deadline. If there is a fresh delay, the growth/shrink pattern may well repeat itself.

As for Germany, it is growing at a far more sluggish pace year-on-year, as trade pressures drag the manufacturing giant down.

Trade war fears have an overlooked victim: lithium

Lithium — widely known for its medicinal capacity (referenced in a classic Nirvana track) — was supposed to be be a shining light in the current global economy, with its potential use in high-capacity electric car batteries sending its value surging.

Now, however, it may have gone from “white gold” to “white dust”, writes Andy Critchlow. He says:

Before the advent of modern electric vehicles (EV), lithium was known for decades as a medicinal cure for depression. But plummeting prices have given investors in the commodity – which is a crucial raw material in the manufacture of high-powered lithium-ion EV car batteries – the blues.

Lithium carbonate prices assessed by S&P Global Platts have tumbled more than 20pc this year to around $10,000 per metric tonne amid a global glut of supply, which has outstripped demand for EVs.

So where next for the struggling compound? You can read Andy’s full thoughts here: Slow take-up of electric vehicles is turning lithium dreams into dust

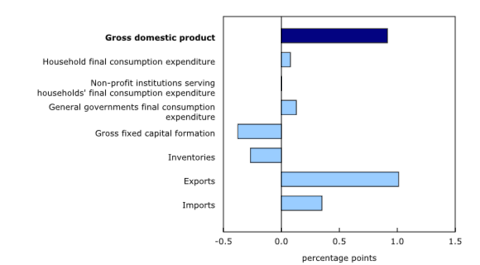

Canadian economic rebound beats expectations

Some mixed news from Canada: the country’s economy beat growth expectations, expanding by 0.9pc in the second quarter, but a susrpise fall in consumption left room for worries.

Here’s how the figures have looked recently:

In its official report, Statistics Canada said:

Expressed at an annualized rate, real GDP advanced 3.7% in the second quarter. In comparison, real GDP in the United States grew 2.0%.

Exports of goods rose 3.7% in the second quarter, following declines in previous two quarters. The increase was led by energy products, which grew 5.9% after a 3.0% decline in the first quarter. Exports of services rose 1.1%, maintaining the pace of the previous quarter. Import volumes declined 1.0%.

GDP growth was moderated by a 1.6% decline in business investment; notable declines occurred in outlays on machinery and equipment and engineering construction. Growth in consumer spending slowed to 0.1%.

Here’s what contributed to the growth on a sector-by-sector basis.

Round-up: Homeowners warned price rebound may not be coming, iPhone vulnerability revealed, lab-grown brain prompts more questions than answers, PLUS: Uncovering the lingerie sector’s struggles

Although US Labor Day (on Monday) will offer a slight reprieve, we’re back to full-blown business season from next week. That doesn’t mean things have been totally silent today, however. Here are some of the top stories from our Business and Tech teams:

Homeowners warned house prices are unlikely to rebound this year after a sluggish August: House price growth remained sluggish in August prompting warnings that the market is unlikely to rebound from its slump for the rest of the year.

Lab-grown brains start producing human-like ‘brain waves’: Tiny brains grown in a lab using stem cells have begun transmitting brainwaves similar to that of a pre-term baby.

Major attack on iPhones ‘lasting years’ exposes data: Hackers have been using compromised websites to install “monitoring implants” in iPhones for years, according to researchers at Google.

If you have an iPhone and are worried about security, here is some guidance on staying safe:

And here’s something you may want to know more about:

From boom to bust: changing tastes and hefty costs leave Victoria’s Secret and lingerie rivals exposed

Retail reporter Laura Onita has taken a closer look at the lingerie sector, where the giants are struggling amid high business costs and increased competition. She writes:

Although the industry is typically somewhat protected, given that most shoppers buy underwear at one point or another, the majority of brands have been selling less since 2017, industry data shows.

“A lot of the traditional chains have a bit of a battle on their hands because they have a lot of stores, a lot of real estate, some are in shopping centres, where they are out-of-fashion. Stores notoriously need to be updated all the time,” says ex-M&S executive Janie Schaffer, nicknamed the “Knickers Queen”.

You can read her full piece here.

Grafton shares jump after earnings beat

Grafton is one of the biggest movers on the FTSE 250 today, beaten only by a typically-volatile Intu and post-plummet Amigo. My colleague Jack Torrance reports:

Shares in builders’ merchant Grafton Group have leapt about 8pc after it revealed better than expected half-year results and announced the sale of its Belgian business.

The FTSE 250 member, whose brands include Selco, Plumbase and Leyland SDM, made profits of £91m in the six months to June, up 5pc, on £1.5bn of revenues.

Gavin Slark, chief executive, said selling the Belgian unit would allow Grafton to invest cash in areas with higher margins.

That update was welcomed by Liberum analysts, but they warned rival Travis Perkins could steal a march on Grafton, writing:

Travis is becoming a tougher competitor, with its management promising improving local service and more competitive pricing.

Tesla exempted from Chinese auto-sales tax

Some good news for electric carmaker Tesla, which will be exempted from China’s planned auto tariffs (set to hit 25pc in December). It is possible that the company has been given preferential treatment because of its heavy investment in the country (a case of mates’ no-rates).

Tesla To Be Exempt From China’s Auto Purchase Tax $TSLA

— LiveSquawk (@LiveSquawk) August 30, 2019

Here’s how auto tariffs currently stand:

Tesla shares are currently gaining on futures trading as investors welcome the news.

Micro Focus holds bounce, M&S back at bottom of FTSE 100

Big moves in the battle for last place on the FTSE 100: Micro Focus’s bounce has brought it off the index’s bottom slot, with a market cap (as of a few minutes ago) of £3.79bn.

That means Marks & Spencer, at a market cap of £3.75bn, is back in the ejector seat, set for an almost-certain relegation from the blue-chip index during next week’s reshuffle.

It might be too little, too late for Micro Focus, which could find its FTSE 100 place usurped by an out-performing mid-cap (of which there are several).

At the close of trading last night, both shares were in relegation territory,

Here’s my colleague Matthew Field’s close look at Micro Focus’s problems:

Investors in ‘wait-and-see’ mode

European equity markets have got their heels dug in, and gains are exceeding 1pc on Germany’s DAX and Italy’s FTSE MiB up 1.25pc.

As it’s the last day of trading, we may also be seeing the impact of funds (particularly pension giants), adjusting their positions to strategise for the coming weeks. Usually (not always), that means the worst losses are rounded off.

On current numbers, the FTSE 100 is likely to have had its worst monthly performance since October — it looked very close to being worse only days ago.

Oanda’s Edward Moya writes:

Global equities are all green as investors squared up positions on the last trading day of the month. With no major updates on the trade war, investors will wait-and-see if September will see any de-escalations with tariffs as we start to see the economic pain be passed onto the US consumer

Mr Kipling owner names new chief exec

Some good, old-fashioned UK corporate news amid all the global uncertainty and economic foreboding: Mr Kipling owner Premier Foods has named a new chairman and chief executive. My colleague Michael O’Dwyer reports:

Colin Day will join the board as chairman while Alex Whitehouse, who has led the company’s drive to turn around its UK business, will become chief executive. Both appointments are effective immediately, the company said.

Alastair Murray, who acted as chief executive for the last seven months, will leave the business immediately. Mr Murray has been finance boss at the cake maker for six years. He will be replaced by an internal candidate, Duncan Leggett, on an interim basis until a permanent successor is found

You can read his full report here: Premier Foods names new chief executive and chairman on the same day

Tariff escalation approaches

Pending anything big happening this afternoon, investors will makes their moves today on the expectation that the trade war will have formally escalated by the time they return to their desks on Monday.

Live goats, baths, blouses, sewage and stoves are all among Chinese exports that will be slapped with tariffs from this Sunday (yes, I am afraid September is that close). Here is the key info you need:

Pound climbs against euro

Sterling has actually (incredibly narrowly) flipped into positive territory against the euro, after a Scottish judge threw out an attempt by anti-no-deal campaigners to have an injunction placed on the government’s attempts to prorogue parliament.

It’s almost flat against the dollar now, which might lead to a worsening picture for the FTSE.

As was noted earlier, most days in August have been a game of two halves, however, and there’s still a chance noises from Washington could shake things up later in the day.

You can keep up with the latest political updates here: Brexit latest news: Sir John Major intends to join legal action to stop Boris Johnson proroguing Parliament

Economist: Temporary distortions are ‘depressing the core’ of eurozone CPI

Pantheon Macroeconomics economist Claus Vistesen has given his take on the inflation and unemployment figures coming out of the eurozone today (see 10:06am update). He writes:

The unchanged core rate looks a bit odd, given that services inflation is estimated to have increased, by 0.1pp to 1.3pc, while non-energy goods inflation was unchanged, at 0.4pc. This is due to rounding, though the main story is that core inflation pressures remain weak overall...

In the labour market, the trend still looks solid, but the rate of improvement is now slowing as a lagged response to the slowdown in GDP growth.

Sterling fall continues

The pound is narrowly down against the dollar and euro today, its third consecutive day of softening. As ever, that is likely to be a help to the FTSE 100, which is up just under 0.5pc.

Looking at the bigger picture, sterling is very much on a longer-term decline: drops over the past six months have be sizeable and steady.

The Boris Johnson era (now past its first month) has been pretty volatile: sterling slumped hard as the new PM’s no-deal stance raised fears among investors, but there was a measured recovery after lows at the start of the month.

All the talk of proroguery and constitutional crisis seems to have put the pound back on a downwards descent, but at the current rate of decline we might still be a couple of weeks from a return to the doldrums.

Of course, a lot could happen in those weeks.

Eurozone inflation and employment stay stable

Inflation and unemployment in the eurozone both remained stable in the latest figures, with annual inflation at 1pc in August and unemployment at 7.5pc in July, its lowest rate in eleven years. No shocks there.

Euro area #inflation stable at 1.0% in August: food +2.1%, services +1.3%, other goods +0.4%, energy -0.6% - flash estimate https://t.co/B9tlBrvDNVpic.twitter.com/sOm5lEccOW

— EU_Eurostat (@EU_Eurostat) August 30, 2019

Euro area #unemployment stable at 7.5% in July; lowest rate since July 2008. EU at 6.3% - lowest since the start of the series https://t.co/A1A8bDAc6opic.twitter.com/fFA4uYMlNz

— EU_Eurostat (@EU_Eurostat) August 30, 2019

UBS: Risks of a no-deal Brexit ‘have not increased’

Swiss investment banking giant UBS has released its latest assessment of the Brexit situation, after Prime Minister Boris Johnson lobbed a cat at a flock of pigeons by revealing plans to prorogue parliament.

They have taken a balanced view, judging the the likelihood of whether a gaggle of rebels, soft Brexiters, and Remainers can stop a no-deal exit hinges on how willing Conservatives are to support Jeremy Corbyn leading a caretaker government. UBS’s strategists say:

In our view, the risks of a no-deal Brexit on 31 October have not increased, but the situation should come to to a head sooner. The currency market appears to be pricing a 50pc chance of a no-deal Brexit in October, which we consider too high. The pound is also very undervalued in purchasing power parity terms. In our FX strategy, we overweight the British pound versus the US dollar. Within international developed market stocks, we are tactically neutral on UK equities. The longer-term risk-return outlook for UK equities looks uncertain, in our view.

Mortgage approvals jump to highest in two years

UK mortgage approvals rose to their highest level in two years during July, the Bank of England says this morning.

Approvals jumped to 67,306 from 66,500 in June, as activity remained stable in the run-up to Britain’s exit from the EU.

Other July stats out from the BoE today:

Consumer credit rose 5.5pc from a year earlier, the same as in June (growth rates were around 10pc back in 2017)

Businesses repaid £2.5bn, the first drop in outstanding borrowing since February

Borrowing on credit cards rose 5.3pc on the year

Non-resident investors sold £2.9bn of UK government bonds, the first net sale since February

Uptick in UK mortgage approvals for house purchase in July to 67k (c. 3%y/y rise). Still pretty comparable to the post 2016 average & consistent with the general "bumping along" picture painted by house price changes. pic.twitter.com/X6iuILnr4F

— Rupert Seggins (@Rupert_Seggins) August 30, 2019

Government announces £30m port investment

Time to crack out the wish list if you happen to run an English port.

The Government has announced £30m in investment for the UK’s ports, inviting ports in England to bid for £10m of the pot “to help deliver upgrades which will enhance capacity and maintain trade flow”.

Ports have until next Friday to get a bid in (which personally feels like quite a rush when millions are at stake, but Brexit is just 62 days away):

The [Port Infrastructure Resilience and Connectivity] competition will be open until 6 September, after which successful bidders will be given up to £1 million each to deliver infrastructure improvements. For example, this may include providing more HGV parking and container storage space or developing traffic systems to ensure the free flow of cars and lorries.

Transport secretary Grant Shapps said:

We are leaving the EU on 31 October and we will be prepared whatever the circumstances.

As the UK continues to develop as an outward-facing global trading nation ready for a post-Brexit world, the resilience of our trading hubs is more critical than ever before.

This £30 million investment supports our ports in their work to boost capacity and efficiency, ensuring they’re ready for Brexit and a successful future.

Micro Focus bounces after deadly drop

Micro Focus, the FTSE 100 software and IT firm that ended up being yesterday’s biggest loser after slashing its forecasts, is having what may well be a dead-cat bounce this morning, with its shares up 6pc currently.

It needs a strong comeback to get itself out of the danger zone for relegation for the danger zone next week — stronger than what we’re seeing so far today.

Hole in the sole: Shoe Zone shares stamped down after boss quits

Shares in Shoezone are off nearly a third currently, after the footwear retailer’s boss announced a sudden exit, and the company slashed its forecast for the full year.

The AIM-listed company’s shares are down 30.7pc currently. It said in a statement this morning:

Nick Davis, the Group's Chief Executive, has tendered his resignation in order to leave Shoe Zone and pursue other business interests. As a result, Nick will be leaving the Group with immediate effect...

...Trading conditions since the Group's Interim Results on 21 May 2019 have been challenging and as a result, the Board now expects to deliver a full year performance below its expectations.

It added that an exceptional charge following a property value write-down would also hurt its bottom line:

The Board has also undertaken a review of its freehold property valuations and has concluded that it will be writing down the value of its 17 freehold properties by £3.1m to £5.3m. This will result in a non-cash exceptional charge in its full year results for the year ending 5 October 2019.

FTSE lags as European rally continues

European markets opened in positive ground as expected, with the FTSE 100 currently lagging behind its continental peers.

Spreadex’s Connor Campbell says:

Clawing its way back to 7200, the FTSE was up 0.2-0.3%, sitting at levels that vary between a one week peak and a fortnight high. Still, unless it manages an unprecedented rally this Friday, August has been an incredibly costly month, given that it closed out July with a foray past 7700...

...Looking ahead – which is maybe a tad premature; the gap between morning and afternoon sessions has often been massive this month – and the Dow Jones is also set to post some milquetoast growth. A 60 point increase would put the index back above 24600; like the DAX, its best price since near the start of August, but 800 points off of where it was at the end of July.

Oanda’s Craig Erlam adds:

We may be facing up to the reality of recession but optimism continues to flow through the veins of investors following comments from the Chinese Commerce ministry on Thursday.

Consumer confidence slips to lowest level since January, as business outlook wanes

UK consumer confidence dropped to its lowest rate in seven months in August, according to a closely-watched index. GfK’s meter gave a reading of –14, down from July’s score of –11. That’s worse than an expected drop to –12, so jitters might be growing quicker than analysts expected.

GfK’s Joe Staton says:

Until Brexit leaves the front pages — whenever that will be — consumers can be forgiven for feeling nervous not just about the wider economy but also about their financial situation.

That’s an important distinction because a significant development in August is the sudden drop in views on personal finances ‘over the next 12 months’ after the encouraging jump in this measure last month.

For a long time, the downward momentum in the Overall Index Score has been associated with our views on economy. But reduced confidence is now affecting how we see our personal finances.

If there is a continuation of that dip in our feelings about our ‘future wallets’, we’d quickly see a headline score (the average of our five sub-measures) crash to a level that approaches the worrying figures seen in the worst days of the 2008/2009 financial crisis.

We are not there yet, and we may not necessarily get there, but it’s a trend we need to watch carefully.

Adding to the gloomy picture, a barometer of business confidence compiled by Lloyds found business confidence had hit its lowest level since 2011:

Surveys suggest UK economy is flagging. ��

Lloyds Bank Business Barometer weakest since late 2011 - unfortunately corroborates the weak European Commission data from yesterday. https://t.co/AjbQKoPPF4pic.twitter.com/HsGloSzFsg— Andy Bruce (@BruceReuters) August 30, 2019

The lender found:

Overall business confidence was down 12 points to 1pc, the first fall since May, and the second largest month-on-month decline this year, bringing levels to just below those seen in June 2016.

Confidence fell across all 12 regions, with the smallest declines in the West Midlands and East of England, and the most notable decline in the East Midlands.

Confidence in manufacturing, retail and services was down, although the construction sector bucked the trend, improving 6 points to 12pc.

Hann-Ju Ho, Lloyds’ senior economist, says:

We have seen a dip in overall business confidence this month, with firms appearing less positive about their own trading prospects and the broader economy, and remaining low against the historic average. While ongoing economic uncertainty is likely a key driver, it’s worth noting that companies’ assessment of the expected impact on their business of the UK leaving the EU has remained broadly unchanged this year.”

Worrying news on #UK#economy as #Lloyds report sharp drop in #business confidence in August & #GfK report #consumer confidence dipped markedly to lowest level since January. Likely reflects concerns over a “no deal” #Brexit. Global outlook hardly helps https://t.co/sR1Eu0rkoU

— Howard Archer (@HowardArcherUK) August 30, 2019

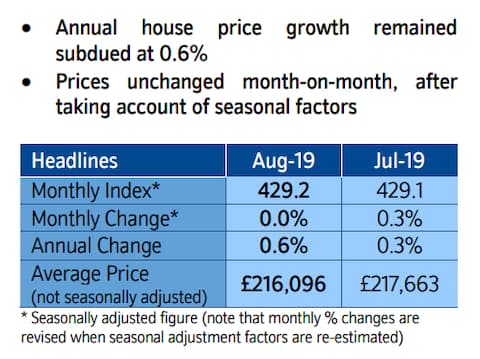

House prices rise defies uncertainty

House price growth rose 0.6pc in August despite Brexit uncertainty, according to the latest index compiled by Nationwide. My colleague Michael O’Dwyer reports:

The annual increase was the biggest since May and means the average UK home now costs just over £216,000 but prices in August were flat month-on-month. Annual house price growth has remained stubbornly below 1pc for the last nine months and almost completely stagnated at the start of the year.

The figures come after mortgage figures on Tuesday showed that banks approved more mortgages than in any month since February 2017 and could indicate that the worst of the pre-Brexit slump in the industry is ending.

You can read Michael’s full piece here: House prices rise in August despite ‘uncertain’ economy

Here are the key figures:

Robert Gardner, Nationwide’s chief economist, said:

Annual house price growth remained below 1pc for the ninth month in a row in August, at 0.6pc. While house price growth has remained fairly stable, there have been mixed signals from the property market in recent months.

Surveyors report that new buyer enquiries have increased a little, though key consumer confidence indicators remain subdued. Data on the number of property transactions points to a slowdown in activity, though the number of mortgages approved for house purchase has remained broadly stable.

Housing market trends will remain heavily dependent on developments in the broader economy. In the near term, healthy labour market conditions and low borrowing costs will provide underlying support, though uncertainty is likely to continue to exert a drag on sentiment and activity.

And here’s Personal Finance editor Lauren Davidson, asking what has happened to Chancellor Sajid Javid’s big ideas for addressing housing market issues:

We were promised ‘bold’ ideas on fixing the housing market. Where are they?

Europe set for gains at open

With just a few minutes until European stock markets open, things are looking upbeat — with futures trading up on all the region’s blue-chip indices.

Investors were given a slight spook by hawkish words from European Central Bank policymakers, who yesterday began to talk down expectations for stimulus efforts following their next meeting, on September 12. Here’s more from my colleague Tim Wallace:

Micro Focus under the microscope

Good morning. One of the UK's biggest tech firms risks being relegated from the FTSE 100 in next week’s reshuffle after a share price collapse yesterday. Shareholders in Micro Focus will be hoping the shares rebound today in the last trading day of a turbulent month for markets.

5 things to start your day

1) Over £1bn was wiped from the valuation of Micro Focus yesterday after Britain’s second-biggest listed tech company issued a revenue warning which could trigger its ejection from FTSE 10 next week and pave the way for a possible sale or break-up of the business.

2) The last prop supporting the economy could be kicked over in the coming months. There are growing warning signs that consumers will stop spending and start saving, hitting sales growth and risking a recession. Business investment is falling, factories are struggling as the world suffers a manufacturing slump, and Britain’s GDP fell by 0.2pc in the three months to June.

3) Toyota will halt production at its Derbyshire plant on November 1 as the Japanese car maker braces for the likelihood of Britain bowing out of the EU without a trade deal. The company described the decision to stop work for at least a day after the October 31 Brexit deadline as “part of our contingency activity”.

4) The trade war is already dragging down China’s economic growth and could end up costing it another $2.5 trillion of lost potential GDP if the battle with the US intensifies further, credit ratings agency Standard and Poor’s has warned. After years of growth at above 6pc per year, S&P anticipates a sharp slowdown to 4.6pc per year over the next decade.

5) Silver shines as prices hit two-year high. It has sometimes been seen as the poor relation to gold: less valuable and less shiny. Now silver has a chance to shine after the precious metal hit its highest price in more than two years, boosted by a wave of investors seeking safe havens. Silver is now worth $18.51 an ounce, a level it last touched in April 2017. It has risen 14pc in August alone and a fifth this year, matching gold's gains.

What happened overnight

Stocks in Asia rallied on Friday morning after China indicated that it would not immediately retaliate against the latest US tariff increase. However the Shanghai Composite index swung into the red as the day wore on reflecting the continuing fragility of investor sentiment. Treasuries steadied and a gauge of the dollar remained near a two-year high.

Shares in Tokyo, Sydney and Seoul advanced on the final trading day of a tumultuous month dominated by the trade war. Yesterday, the S&P 500 Index rose for a second day after a spokesman for China’s commerce ministry said that escalating the conflict won’t benefit either side and that it was more important to discuss removing the extra duties.

But investor sentiment remains fragile after Donald Trump’s recent pronouncements on trade. Mr Trump said the US and China were scheduled to have a conversation about trade, but it was unclear whether such talks took place on Thursday.

Elsewhere, West Texas crude held above $56 a barrel. Italian bonds rose as the country moved toward forming a new government. Argentina’s long-term foreign currency debt rating was downgraded by S&P Global Ratings, which said the government’s extending maturity of all short-term paper constitutes default.

Coming up today

Healthcare software and solutions company EMIS will issue its half-year results. The company recently shed its non-core Specialist and Care business, giving it more cash to play with. Despite the benefits of a close relationship with the NHS, EMIS’s leadership is seeking to diversify its operation to include more private sector work, and investors will be watching closely for evidence of how that shift is going.

Interim results: EMIS Group

Economics: GfK consumer confidence (UK), consumer credit (UK), mortgage approvals (UK), UoM sentiment (US), personal income and spending (US), inflation (eurozone)