Yahoo Finance

Yahoo Finance

MOODY'S: Normal interest rates are history

REUTERS/Sang Tan

Remember interest rates?

Moody's, the credit-rating company, does.

And, according to Moody's managing director Colin Ellis, there's a good chance that they're not coming back.

At least not at the levels we became accustomed to before the 2008 financial crisis.

Ellis lists numerous reasons, but at the core is the changing relationship between interest rates and inflation and the difficulties central banks are having in getting prices and economic activity to gradually increase.

"Over the past seven years, policy rates have been at low levels in most economies, and central banks have dramatically expanded balance sheets," Ellis said. "Despite this, there has been little sign of a genuine and pervasive increase in inflation."

Low interest rates have failed to raise inflation because economic growth has remained stubbornly low. This leads to less investment spending and a vicious circle of sluggish growth and low interest rates.

Here's Ellis (emphasis ours):

There are several hypotheses why the natural rate of interest has shifted downwards over time. One is an exogenous decline in the trend rate of global growth.

However, while demographic factors and in particular aging populations have lowered trend growth in several countries — and will continue to do so over the coming decade — recent lower growth also reflects weak investment spending, rather than just weaker exogenous productivity growth.

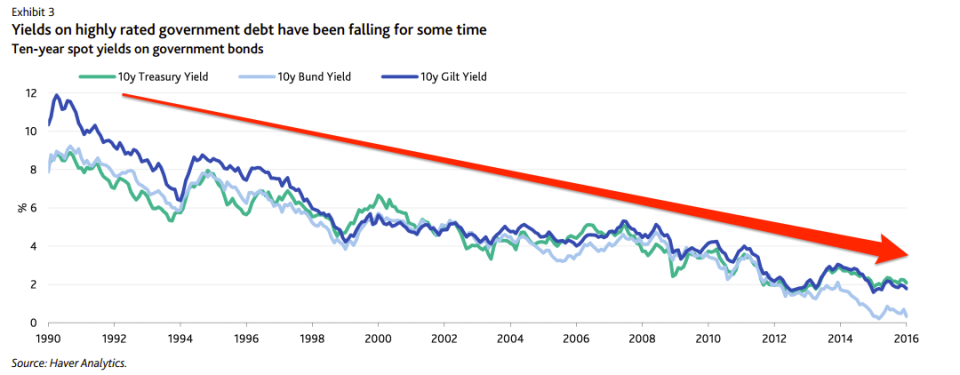

And here's the chart showing rates declining over time:

REUTERS/Sang Tan

This is not a problem that will be solved within the next 10 to 20 years, Ellis argues, because of the demographic makeup of the global economy, which favours saving over spending and investment (emphasis ours):

One potentially relevant factor here is the global demographic profile.

In general, 'peak' saving ages are often thought to be between 40 and 60, especially in advanced economies. As such, when population concentrations move through this bracket, saving may increase, putting downward pressure on the natural rate.

NOW WATCH: This behavior could kill your chances in a Goldman Sachs interview

See Also: