Yahoo Finance

Yahoo Finance Premier Miton Group (LON:PMI) Has Announced A Dividend Of £0.03

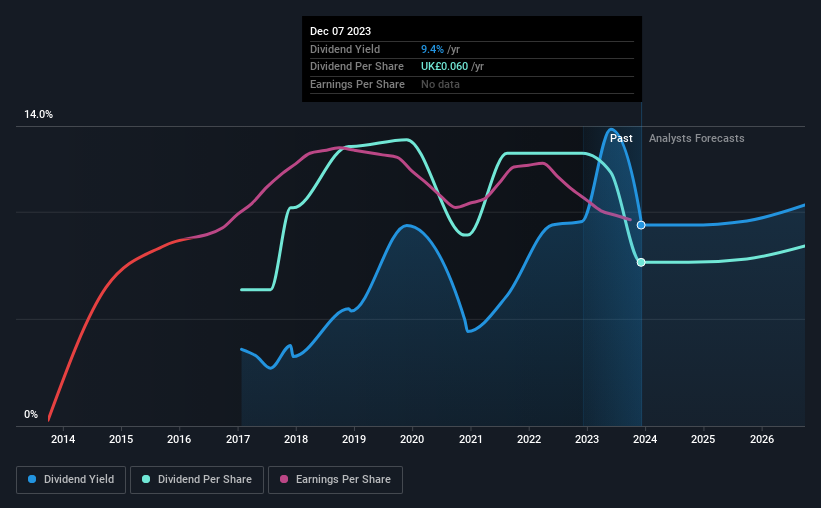

The board of Premier Miton Group plc (LON:PMI) has announced that it will pay a dividend on the 16th of February, with investors receiving £0.03 per share. The yield is still above the industry average at 9.4%.

Check out our latest analysis for Premier Miton Group

Premier Miton Group Is Paying Out More Than It Is Earning

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Prior to this announcement, the company was paying out 240% of what it was earning. It will be difficult to sustain this level of payout so we wouldn't be confident about this continuing.

The next 12 months is set to see EPS grow by 100.1%. If the dividend continues on its recent course, the payout ratio in 12 months could be 127%, which is a bit high and could start applying pressure to the balance sheet.

Premier Miton Group's Dividend Has Lacked Consistency

Looking back, Premier Miton Group's dividend hasn't been particularly consistent. If the company cuts once, it definitely isn't argument against the possibility of it cutting in the future. The annual payment during the last 7 years was £0.05 in 2016, and the most recent fiscal year payment was £0.06. This implies that the company grew its distributions at a yearly rate of about 2.6% over that duration. Modest growth in the dividend is good to see, but we think this is offset by historical cuts to the payments. It is hard to live on a dividend income if the company's earnings are not consistent.

The Dividend Has Limited Growth Potential

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. Over the past five years, it looks as though Premier Miton Group's EPS has declined at around 27% a year. This steep decline can indicate that the business is going through a tough time, which could constrain its ability to pay a larger dividend each year in the future. Over the next year, however, earnings are actually predicted to rise, but we would still be cautious until a track record of earnings growth can be built.

We're Not Big Fans Of Premier Miton Group's Dividend

In summary, it's not great to see that the dividend is being cut, but it is probably understandable given that the current payment level was quite high. The company seems to be stretching itself a bit to make such big payments, but it doesn't appear they can be consistent over time. Considering all of these factors, we wouldn't rely on this dividend if we wanted to live on the income.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Just as an example, we've come across 2 warning signs for Premier Miton Group you should be aware of, and 1 of them can't be ignored. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.