Yahoo Finance

Yahoo Finance Questor: This company is the golden egg of ethical shopping

“Never invest in a business you cannot understand”, warned the legendary American investor Warren Buffett. The stock Questor is tipping today passes that test from the so-called “Sage of Omaha” at the very least.

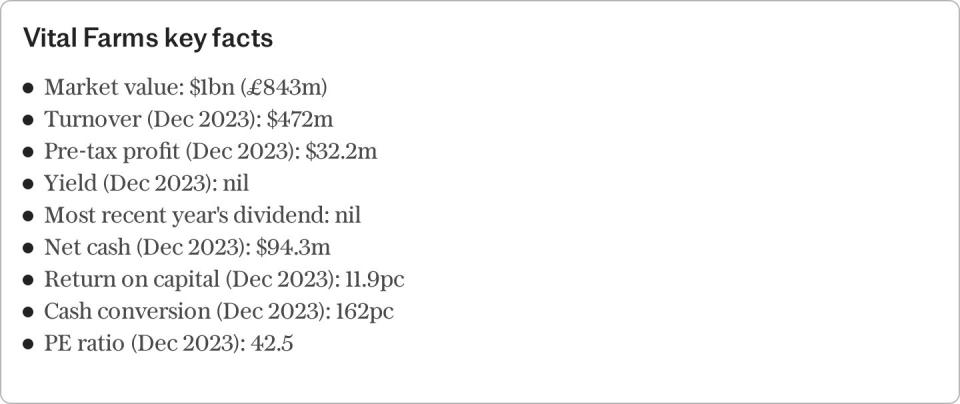

America’s Vital Farms has grown to become a $1bn (£843m) company thanks to its extraordinary success in the simple business of selling eggs.

Customers are prepared to shell out $4.87 more for a dozen of its eggs than those of conventional brands, and $1.94 more than those offered by “premium” rivals.

Its business is growing rapidly, too, with net turnover up tenfold since 2015 and expected to more than double again by the end of 2027.

This success comes down to Vital Farms’ ability to tap into the lucrative growth of ethical shopping.

The company’s trendily packaged products sell a lifestyle as much as a culinary staple. And in creating a business model that aligns with its customers’ values, Vital Farms has created a far stronger competitive advantage than one would expect from a company selling a commodity foodstuff.

This has not been lost on some of the world’s best-performing fund managers. Ten of these investors, each among the top 3pc of the 10,000 equity fund managers tracked by financial publisher Citywire, own shares in Vital Farms. That results in an AAA rating from Citywire Elite Companies, which rates companies on the basis of their backing by the world’s best professional investors.

Vital Farms sources eggs from a network of American family farms with prime conditions for raising pasture-fed chickens. Not owning farms substantially reduces capital requirements, but the company does own a central egg processing and packing facility built in 2017 and expanded in 2022. Eggs are distributed through a growing network of stores that appreciate the speed at which boxes fly off shelves.

The relationships Vital Farms has built with farmers, distributors and customers since it was founded in 2007 are hard for competitors to replicate. This underpins its formidable pricing power. However, it also means growth hinges on attracting suppliers as well as customers. Fortunately, it does well on both fronts.

Marketing efforts, such as enabling customers to find out which farm their eggs came from, focus on boosting awareness about the benefits of pasture-fed chicken eggs and underlining the authenticity of the brand. Customer numbers have risen from 800,000 to 10.5 million between 2015 and 2023.

The number of stores stocking products has also rocketed over the same period, from less than 5,000 to 24,000. Moving beyond the natural food market into mainstream American supermarkets, such as Kroger and Albertsons, has helped to drive this. Vital Farms’ first big customer, Whole Foods, delivered 23pc of the company’s sales last year, but was the only retailer accounting for more than a tenth of the total.

Management expects to grow sales by raising the number of product lines stocked by existing retailers as well as supplying new stores. It also believes there is significant growth potential in selling to like-minded food services companies that want to align with its brand – this currently accounts for just 6pc of sales.

Since 2015, the number of farms that supply Vital Farms has ballooned from 50 to over 300, with a target of about 550 by the end of 2027.

Farms are required to make big upfront investments to meet the company’s ethical standards. A tougher lending environment means Vital Farms expects “working capital” – the assets and liabilities involved in its day-to-day operations –to rise by up to $12m as it helps finance these investments through advances on contracted egg purchases. Once farms meet standards, farmers get regular support, inspections, and guidance on best practice along with the purchase of all their eggs at good prices, including quarterly adjustments for feed fluctuations. Contracts generally last for three years.

Farmers benefit from Vital Farms taking on the risks associated with volatility in the egg market. The strength of the company’s brand and distribution is key to making this pay off for shareholders.

Increased scale is leading to increased profitability. Profit margins, based on the adjusted Ebitda (earnings before interest, tax, depreciation, and amortisation) measure, rose from 4.5pc in 2022 to 10.2pc last year and are expected to reach between 12pc and 14pc by 2027. The 2027 net revenue target is $1bn versus $465m last year. The company is looking for a site for a new egg plant to achieve this as the current facility can only support $700m of sales.

This fast-rising profitability has resulted in analysts upgrading their earnings per share (EPS) forecasts for the current financial year by nearly 50pc over the past 12 months. They expect earnings growth to average 27pc a year over the next three years, which helps to explain a price-earnings ratio of 33 times expected profits over the next 12 months.

Some of the world’s best-performing fund managers believe this is a price worth paying, given Vital Farms’ growth prospects and formidable pricing power. This column agrees.

Questor says: buy

Ticker: NYSE:VITL

Share price at close: $25.07

Algy Hall is investment editor of Citywire Elite Companies

Read the latest Questor column on telegraph.co.uk every Sunday, Monday, Tuesday, Wednesday and Thursday from 8pm.

Read Questor’s rules of investment before you follow our tips