Yahoo Finance

Yahoo Finance Questor: this oil and gas giant’s performance can be volatile but its rewards are consistent

There is no such thing as a risk-free dividend stock. Even companies that have made shareholder payouts without interruption for decades can experience unexpected financial difficulties which cause their dividend payments to abruptly come to an end.

Indeed, the pandemic is a prime example of the risks involved in relying on any company for a regular income. Previously ultra-reliable dividend stocks suddenly hoarded cash in response to exceptional circumstances that meant investors did not receive payouts for a prolonged period.

Despite this, Questor strongly feels that individual company shares should form the backbone of an income portfolio.

Yes, there are inherent risks. Cuts, postponement and even cancellation of dividends. But those threats must be weighed against the significant potential rewards provided by income shares, which can offer attractive yields, inflation-beating dividend growth and substantial capital gains over the long run.

Therefore, while BP’s financial performance is typically volatile due to its dependence on erratic energy prices, it becomes the latest addition to our income portfolio.

Its introduction aligns with our long-term plan to increase the number of direct equities held in the portfolio. The firm’s latest quarterly results were somewhat disappointing. Underlying profits in the first quarter of its financial year missed expectations, with profits falling by 45pc over the same period in the previous year and by 9pc compared with the prior quarter, partly as a result of lower energy prices.

Despite this, the company maintained dividends per share at the same level as in the previous quarter. This meant they were up 10pc compared with a year prior, which is significantly ahead of the rate of inflation.

And dividends were still being covered 2.2 times by underlying profits in the first quarter of the current year despite the aforementioned decline in profitability, there is sufficient headroom for shareholder payouts to further grow in future.

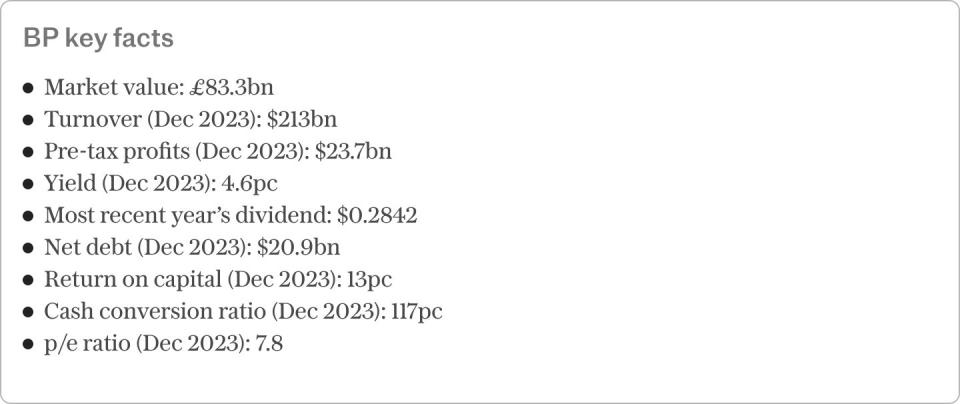

Moreover, BP’s dividend yield currently stands at 4.6pc.

This is around one percentage point greater than the FTSE 100 index’s yield. And this highlights that while the firm’s financial performance will be perennially volatile, the risk/reward opportunity for investors is relatively favourable. When combined with a price-to-earnings ratio of just eight, the total return potential on offer for long-term investors is significant.

Of course, the firm’s solid financial position reduces overall risk for investors.

Although net debt rose by 15pc in the first quarter of the year, the company’s net gearing ratio stands at a very modest 28pc. This provides sufficient financial strength to invest in new projects, with capital expenditure expected to amount to $16bn (£12.64bn) per year in 2024 and 2025.

The company is also seeking to become more efficient, with it aiming to generate at least $2bn of cash cost savings by the end of 2026. This forms part of a wider, refreshed strategy that seeks to maximise shareholder returns by aligning the company’s pace of transition to cleaner forms of energy with changes in consumer demand.

Encouragingly, energy demand is likely to be buoyed by an improving global economic outlook. Although inflation is proving to be stickier than many investors had anticipated, particularly in the US, it is nevertheless on track to fall to central bank targets over the coming months. This should provide scope for interest rate cuts that will (eventually) act as a catalyst on the world economy’s growth rate.

Since Questor first advised readers to purchase BP in August 2021, its shares have produced a 64pc capital gain. This equates to a 49 percentage point outperformance of the FTSE 100.

Dividends received or declared since our original tip, meanwhile, amount to 19pc of our notional purchase price.

In this column’s view, those returns have been well worth the seemingly constant volatility in the company’s financial performance and share price that are almost certain to continue in future.

The stock’s low valuation means further capital gains are on the cards, while a relatively high yield, well-covered shareholder payouts and dividend growth potential mean it is poised to produce an attractive income return.

With a solid financial position, sound strategy and an improving economic outlook, BP is a worthwhile addition to our income portfolio despite its inherent risks. Its purchase will be funded by cash raised from recent sales that has not yet been fully redeployed.

Questor says: buy

Ticker: BP

Share price at close: 489.3p

Read the latest Questor column on telegraph.co.uk every Sunday, Monday, Tuesday, Wednesday and Thursday from 8pm.

Read Questor’s rules of investment before you follow our tips.