Yahoo Finance

Yahoo Finance Reasons to Add Curtiss-Wright (CW) Stock to Your Portfolio Now

Curtiss-Wright Corp.’s CW expertise in supplying precision components to the aerospace, defense, general industrial and power generation markets is boosting its performance. The increasing adoption of alternative energy sources worldwide, which is fueling the value of nuclear technology, acts as a tailwind for the company. Given its growth prospects, CW makes for a solid investment option in the aerospace sector.

Let’s focus on the factors that make this Zacks Rank #2 (Buy) company a strong investment pick at the moment.

Growth Projections & Surprise History

The Zacks Consensus Estimate for CW’s 2024 earnings per share has increased 1.1% to $10.27 per share over the past 60 days. The Zacks Consensus Estimate for its 2024 revenues is pegged at $3.02 billion, which implies a rise of 6.3% from the 2023 reported sales figure.

The company delivered an average earnings surprise of 9.01% in the last four quarters.

Return on Equity

Return on equity (ROE) indicates how efficiently a company has been utilizing funds to generate higher returns. Currently, CW’s ROE is 16.79%, higher than the industry’s average of 11.64%. This indicates that the company has been utilizing funds more constructively than its peers in the electricity utility industry.

Solvency & Liquidity

CW’s times interest earned ratio (TIE) at the end of the first quarter of 2024 was 11. The TIE ratio of more than 1 indicates that the company will be able to meet its interest payment obligations in the near term without any problems.

The company’s current ratio at the end of the first quarter was 2.02, higher than the industry’s average of 1.54. The ratio, being greater than one, indicates Curtiss-Wright’s ability to meet its future short-term liabilities without difficulties.

Dividend History

Curtiss-Wright has been increasing its shareholders’ value through frequent dividend hikes. In May 2024, CW announced a quarterly dividend of 21 cents per share, an increase of 5% from the previous payout level of 20 cents per share, resulting in an annual dividend of 84 cents. The company’s current dividend yield is 0.30%, better than the industry's average of 0.18%.

CW’s Nuclear Power Expansion

Curtiss-Wright, a leading provider of advanced nuclear technologies, is expected to see increased opportunities due to the $3.2 billion allocated by the U.S. Department of Energy for advanced nuclear through its Advanced Reactor Demonstration Program. To further expand its footprint in this space, in April 2024, CW acquired WSC, Inc., a company that supports commercial nuclear power generation and process plants.

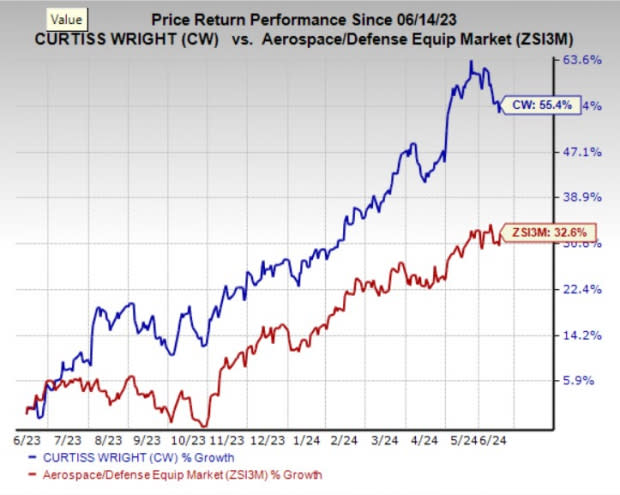

Price Performance

In the past year, the stock has rallied 55.4% compared with the industry’s growth of 32.6%.

Image Source: Zacks Investment Research

Other Stocks to Consider

A few other top-ranked stocks from the same sector are Leidos Holdings, Inc. LDOS, which sports a Zacks Rank #1 (Strong Buy), and BAE Systems BAESY and Safran SAFRY, each carrying a Zacks Rank #2 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Leidos’ long-term (three to five years) earnings growth rate is pegged at 11.1%. The Zacks Consensus Estimate for LDOS’ 2024 sales is pegged at $16.07 billion, which indicates an improvement of 4.1% from the 2023 reported sales figure.

BAE Systems’ long-term earnings growth rate is pegged at 12.2%. The Zacks Consensus Estimate for BAESY’s 2024 sales is pegged at $35.26 billion, which implies an improvement of 34.1% from the 2023 reported sales figure.

Safran’s long-term earnings growth rate is pegged at 34.7%. The Zacks Consensus Estimate for SAFRY’s 2024 sales is pegged at $29.4 billion, which indicates a rise of 42.9% from the 2023 reported sales figure.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Bae Systems PLC (BAESY) : Free Stock Analysis Report

Curtiss-Wright Corporation (CW) : Free Stock Analysis Report

Safran SA (SAFRY) : Free Stock Analysis Report

Leidos Holdings, Inc. (LDOS) : Free Stock Analysis Report