Yahoo Finance

Yahoo Finance Reasons Why You Should Retain HealthEquity (HQY) Stock for Now

HealthEquity, Inc. HQY has been gaining from its business model and strategy. The optimism led by a solid fourth-quarter fiscal 2024 performance and strength in Health Savings Accounts (HSA) are expected to contribute further. However, stiff competition and the possibility that integration of acquisitions may be unsuccessful are major downsides.

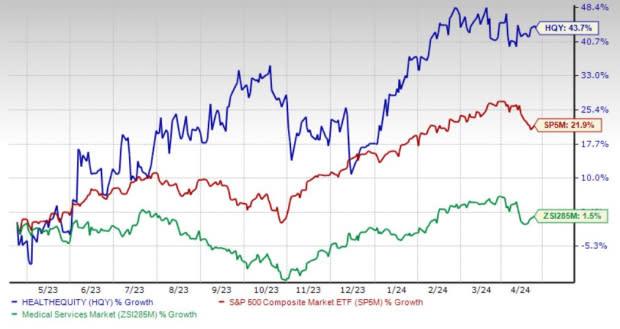

Over the past year, the Zacks Rank #3 (Hold) stock has gained 43.7% compared with the 1.5% rise of the industry and the S&P 500’s 21.9% growth.

The renowned provider of technology-enabled services platforms for healthcare savings and spending decisions has a market capitalization of $6.99 billion. The company projects 29% growth for the next five years and expects to witness continued improvements in its business. HealthEquity’s earnings surpassed the Zacks Consensus Estimate in all the trailing four quarters, the average earnings surprise being 17.4%.

Image Source: Zacks Investment Research

Let’s delve deeper.

Business Model and Strategy: We are optimistic about HealthEquity’s business model, which is based on a business-to-business-to-consumer distribution strategy. The company believes that there are significant opportunities to expand the scope of services that it provides to its current Clients. Per HealthEquity’s management, it has a diverse distribution footprint to attract new Clients and Network Partners. Its sales force calls on enterprise and regional employers in industries across the United States, as well as potential Network Partners from among health plans, benefits administrators and retirement plan record keepers.

Strength in HSA: HealthEquity’s total number of HSAs, as of Jan 31, 2024, rose 8.9% year over year. HealthEquity reported 610,000 HSAs with investments as of Jan 31, 2024, up 12.8% year over year. Total Accounts, as of Jan 31, 2024, were up 5.2% year over year. This uptick included total HSAs and 7 million other consumer-directed benefits (CDB). Total HSA assets at the end of Jan 31, 2024, were up 13.9% year over year. This included HSA cash and HSA investments.

Strong Q4 Results: HealthEquity saw solid top-line and bottom-line performances in fourth-quarter fiscal 2024. The top line benefited from robust contributions from the majority of its revenue sources. The expansion of both margins was also seen.

Downsides

Integration of Acquisitions Maybe Unsuccessful: The success of HealthEquity’s recent acquisitions depends partly on its ability to realize the anticipated business opportunities by combining the operations of the acquired businesses with its business in an efficient and effective manner. The integration of HealthEquity’s acquisitions could take longer and be more costly than anticipated, and it could result in the disruption of its ongoing business and the acquired business, among others, and could harm its financial performance.

Stiff Competition: HealthEquity faces stiff competition in the Medical Services market, which is a rapidly evolving and fragmented one. The company’s success depends to a substantial extent on the willingness of consumers to increase their use of HSAs and other CDBs, and its ability to increase engagement and demonstrate the value of its services to existing and potential clients.

Estimate Trend

HealthEquity has been witnessing a positive estimate revision trend for fiscal 2025. Over the past 90 days, the Zacks Consensus Estimate for its earnings per share has moved 3.6% north to $2.90.

The Zacks Consensus Estimate for first-quarter fiscal 2025 revenues is pegged at $278.8 million, suggesting a 14.1% rise from the year-ago reported number.

Key Picks

Some better-ranked stocks in the broader medical space are IDEXX Laboratories, Inc. IDXX, Becton, Dickinson and Company BDX, popularly known as BD, and Ecolab Inc. ECL.

IDEXX, carrying a Zacks Rank #2 (Buy) at present, has an estimated long-term growth rate of 11.6%. IDXX’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 8.3%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

IDEXX’s shares have lost 2.9% compared with the industry’s 1.8% decline in the past year.

BD, carrying a Zacks Rank of 2 at present, has an estimated long-term growth rate of 9.4%. BDX’s earnings surpassed estimates in three of the trailing four quarters and broke even once, with the average being 4.6%.

BD has lost 10.5% against the industry’s 1.9% rise in the past year.

Ecolab, carrying a Zacks Rank of 2 at present, has an estimated long-term growth rate of 13.3%. ECL’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 1.7%.

Ecolab’s shares have rallied 32% against the industry’s 10.3% decline in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Ecolab Inc. (ECL) : Free Stock Analysis Report

Becton, Dickinson and Company (BDX) : Free Stock Analysis Report

IDEXX Laboratories, Inc. (IDXX) : Free Stock Analysis Report

HealthEquity, Inc. (HQY) : Free Stock Analysis Report