Yahoo Finance

Yahoo Finance Restaurant Brands' (QSR) Comps Growth Aids, High Costs Hurt

Restaurant Brands International Inc. QSR continues to benefit from robust comps growth, expansion efforts and strategic investments. Strong digital ordering is also aiding the company. However, high costs and general softening in the consumer environment are a concern.

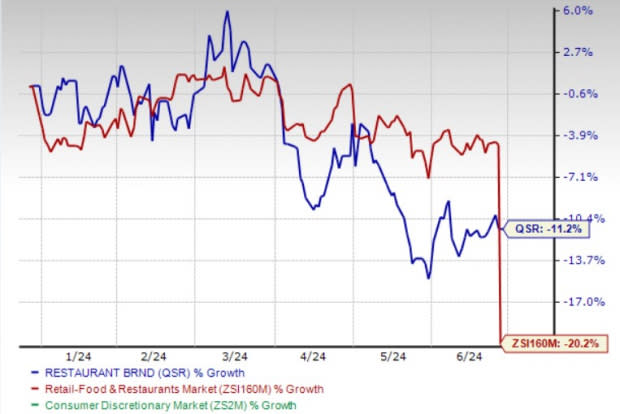

The company's earnings estimates for 2024 and 2025 have been revised upwards, reflecting analysts' optimism about a potential turnaround. Despite its shares having dropped 11.2% over the past six months, compared to the industry's 20.2% decline, the stock has demonstrated resilience in the past month, gaining 3.1% against the industry's 15.2% decline.

Growth Drivers

The company impressed investors with solid comps. In the fourth quarter of 2024, comps in Tim Hortons, Burger King and Popeyes came in at 6.9%, 3.8% and 5.7%, respectively, compared with 14.9%, 8.7% and 3.6% in the prior-year quarter. The upside was primarily driven by strengthening core offerings and enhanced restaurant operations.

Restaurant Brands sees immense potential to expand its brands globally by strengthening the company’s presence in existing markets and venturing into new ones. QSR is actively exploring avenues to accelerate the international growth of all three brands by establishing master franchisees with exclusive development rights and forming joint ventures with its new and existing franchisees.

In 2023, expansion efforts extended to over 75 markets beyond the United States and Canada, securing 15 development and master franchise agreements for new markets. This includes introducing Tim Hortons in Singapore and South Korea, Firehouse in Mexico and the UAE, and Popeyes and Burger King in Bosnia. Primary drivers of net restaurant growth in 2023 included Burger King in China and India, as well as in France and Spain. The company is also expanding Popeyes into Eastern Europe by launching in the Czech Republic and planning to introduce its Louisiana Chicken to Italy. Additionally, Firehouse began its global expansion by opening its first location in Mexico.

This Zacks Rank #3 (Hold) company is also taking initiatives to re-image its restaurants to more modern décor. The company is on track to complete nearly 400 remodels through its Royal Reset remodel program and regular re-imaging efforts by 2024, with close to 100 remodels already operational for at least six months. QSR is confident in the effectiveness of the Reclaim of the Flame initiative. It announced an expanded co-investment program, totaling $300 million, aimed at remodeling an additional 1,100 restaurants and achieving a modern image representation of between 85% and 90% by 2028.

Image Source: Zacks Investment Research

Concerns

The company has been bearing the brunt of high expenses for some time. In first-quarter 2024, total costs of sales came in at $606 million compared with $550 million reported in the prior-year quarter. The upside was primarily driven by inflationary pressures, increases in supply chain sales, increases in equipment sales, an increase in supply chain bad debt expense and an unfavorable FX Impact. The company is cautious about foreign exchange volatility, rising interest rates and general softening in the consumer environment (which have been exacerbated by conflicts in the Middle East), thereby affecting the business and result of operations.

In the first quarter of 2024, QSR faced adverse effects on its performance owing to the softer consumer backdrop in China, deceleration in pricing in Western Europe markets and the repercussions of the conflict in the Middle East. The conflict led to a 60-basis point decline in comparable sales for the quarter. Looking ahead, the company approaches this situation with caution.

Key Picks

Wingstop Inc. WING sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

It has a trailing four-quarter negative earnings surprise of 21.4%, on average. The stock has surged 112% in the past year. The Zacks Consensus Estimate for WING’s 2024 sales and earnings per share (EPS) indicates a rise of 27.5% and 36.7%, respectively, from the year-ago levels.

Brinker International, Inc. EAT currently sports a Zacks Rank #2 (Buy). It has a trailing four-quarter earnings surprise of 213.4%, on average. EAT’s shares have risen 85.4% in the past year.

The Zacks Consensus Estimate for EAT’s 2024 sales and EPS indicates 5% and 41.3% growth, respectively, from the year-earlier actuals.

El Pollo Loco Holdings, Inc. LOCO currently carries a Zacks Rank #2. It has a trailing four-quarter earnings surprise of 19.4%, on average. LOCO’s shares have risen 5.2% in the past year.

The Zacks Consensus Estimate for LOCO’s 2025 sales and EPS indicates 3.8% and 9.9% growth, respectively, from the prior-year figures.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Brinker International, Inc. (EAT) : Free Stock Analysis Report

El Pollo Loco Holdings, Inc. (LOCO) : Free Stock Analysis Report

Restaurant Brands International Inc. (QSR) : Free Stock Analysis Report

Wingstop Inc. (WING) : Free Stock Analysis Report