This article was contributed by Stockopedia guest author, marben100

Earlier this week, a very important article/study was reported on by Reuters, following on from the original press release from the University of Texas here.

I have been sceptical that shale gas is the panacea it's been touted as. My concern was whether the CAPEX required for drilling and fracking was economically justifiable, given the rapid decline rate of shale wells. Whilst such wells produce strongly initially, they decline rapidly, so are only economic if the CAPEX is quickly repaid from production.

The study reported on (which doesn't seem to be publicly available yet), does indicate that some areas of shale are economically viable, but (as I had understood from a presentation I attended a few years ago from a fracking specialist) not all. This study is extremely important because it is the first comprehensive review of the history of 16,000 wells drilled in the Barnett shale, through to mid 2011.

Here are my thoughts on implications:

ADVERTISEMENT

Investors need to be very wary of investing in smaller companies with shale assets. The economics vary greatly between different areas of the same shale deposit. Whilst some acreage in the Barnett shale is highly rewarding, other acreage proves not to be economic. It is only by expending a considerable amount of CAPEX on drilling and fracking that you can be confident which is which. Hence drilling shale acreage, in my view, is a game for the big boys, with deep pockets. Otherwise it's a huge gamble.

Reuters' headline "The Barnett Shale formation in Texas will play a central role in the U.S. natural gas boom for a generation" may be overegging things a bit. According to the U-Texas press release, Barnett shale production is now at a peak of 2Tcf p.a. - and will decline to 900bcf by 2030 (with 44Tcf being economically recoverable, in total). However, according to the FAQ on the study US consumption in 2011 was 24.4Tcf. So whilst the Barnett shale was a significant contributor, it's actual and potential contribution is limited.

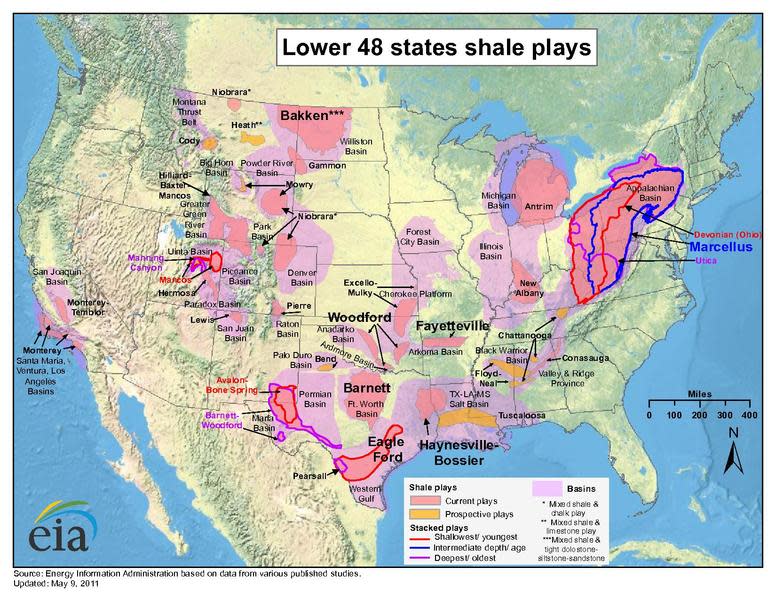

Texas University is planning to study other major shale formations: the Marcellus, Haynesville and Fayetteville. Until those studies are complete, it's somewhat hard to judge what the overall impact of shale production will be. You can see the major US shale plays here:

Areally, the Marcellus appears to dominate, so the results of that study will be important. According to various reports, the latest EIA estimate for the Marcellus is 141Tcf technically recoverable. Indications are that that figure may be revised upwards, as it only covers data through 2010, but economically recoverable is another matter.

So, my overall conclusion is that the jury is still out on the full impact of shale gas. IMO this is an important issue for all investors to follow, for the following reasons:

Successful exploitation of shale gas by the US has global implications.

If there is sufficient US production for export, this will impact LNG prices worldwide - investors need to be cautious about hydrocarbon businesses reliant on high gas prices in the far east (gas in Japan sells for ~ $17/mcf, vs $4/mcf in the US). Japan is already making noises about the current crude oil-linked LNG pricing mechanism.

It does seem increasingly likely that the US will have access to a relatively cheap source of energy for at least the next 20-30 years. That is highy positive for US industry and the US economy and strengthens the US competitive position vis a vis, for example, Germany.

Clearly, the importance of shale gas is positive for companies that support the industry, whose shares have previously been under pressure due to lower gas prices. At current levels, the economics add up and drilling necessary to maintain & increase production will proceed.

The expertise of businesses experienced in US shale gas development will probably be in demand worldwide.

Technologies that allow natural gas to be exploited efficiently will be in demand

I look forward to the results of the Marcellus study with considerable interest.

Manchester United staff have been left fuming at a decision from INEOS and Sir Jim Ratcliffe ahead of the FA Cup final against Manchester City next month.

For the Love of Dogs viewers were left infuriated as they pointed out a 'bad habit' of presenter Alison Hammond's during the latest episode of the ITV show, which has seen ratings plummet.

The moment was filmed by a Pollok resident who was left disgusted after spotting the vermin from her kitchen window in the Templeland Road area of Glasgow.

Vida was treated by vets for lacerations which saw its coat soaked in blood but Quaker was in an equine hospital with its future "not looking good", sources said

Prince William made a surprise visit to a school in the West Midlands today, where he issued a 14-word update on his wife, Kate Middleton, amid her cancer treatment

Meghan Markle and Prince Harry made their first public appearance alongside Prince William and Kate Middleton in 2018, but a Royal author has claimed it was marred by an awkward moment

Callum Laing, 40, was diagnosed with a stage 4 Glioblastoma brain tumour, after he had been suffering from intense headaches - but surgeons in Edinburgh have made a surprising discovery.

Footage taken by a Brazilian tourist shows several pedestrians stepping to soothe the black horse which caused damage after running through the London streets on Wednesday.

Yahoo Finance

Yahoo Finance