Yahoo Finance

Yahoo Finance These shares are a bargain buy as consumers look forward to sunnier times

Tesco’s share buyback programme seemingly knows no bounds. Between its start in October 2021 and the company’s half-year results in August 2023, Tesco repurchased £1.6bn of its own shares. By April, this figure is on course to reach £1.8bn. That compares with a current market value of roughly £20bn.

In addition, its recent decision to sell its credit cards, loans and savings operations to Barclays for around £700m means further share buybacks are ahead. In fact, the retailer plans to use most of the combined £1bn it will receive from the sale of its banking arm and a recent special dividend paid to it by Tesco Bank to repurchase even more of its own shares.

Some investors are likely to be unhappy with the growing scale of the company’s share buyback programme. They may think that a reduction in debt or greater investment in growth opportunities are better uses of surplus cash.

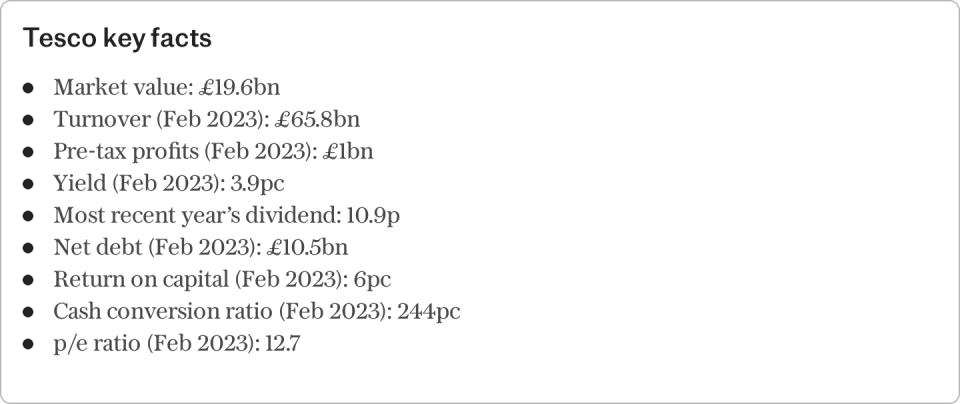

In Questor’s view, though, the company’s share buyback programme represents a highly efficient use of capital. Tesco’s shares currently offer excellent value for money, which means repurchasing them is a logical move. They trade at just 12.7 times earnings, thereby significantly undervaluing the company’s long-term growth potential.

Moreover, Tesco is not highly indebted and has a strong market position. For example, debts equivalent to 82pc of assets and an interest bill covered around six times by profits in the first half of the year evidence a solid financial position that should further strengthen as the sale of its banking arm reduces financial liabilities.

Its latest trading statement, meanwhile, showed a rise of 0.15 of a percentage point in its market share in Britain to 27.9pc in the four weeks to Christmas. Alongside a 35pc share of the online grocery market, the company has an excellent competitive position at a time when the longstanding trend towards digital retailing appears to have resumed.

For example, Tesco generated online sales growth of 11.5pc over the third quarter and Christmas trading period. This was better than the 10pc growth recorded in the first half of the 2024 financial year.

The company’s strong market position makes it well placed to capitalise on an improving consumer outlook. Although inflation currently stands at twice the Bank of England’s 2pc target and is proving to be somewhat sticky, wage growth has outpaced it over the past 10 months. Shoppers are gradually noticing an improvement in their spending power: consumer confidence recently reached its highest level for two years.

Upbeat consumers with greater spending power generally become less price conscious, which provides retailers with an opportunity to raise prices and increase profit margins.

Improving consumer confidence is also likely to mean they prioritise convenience, service and other factors alongside value for money. This could aid established mid-market grocers such as Tesco in their ongoing battle against no-frills operators that struggle to offer much more than low prices.

This trend is likely not only to persist but to gain momentum as the impact of higher interest rates on inflation is fully felt. And with the approach of interest rate cuts, which should stimulate economic growth, the improving prospects for retailers do not appear to have been priced in by investors.

Indeed, Tesco’s shares have risen by just 8pc since this column first recommended them in October 2017. Although they have outperformed the FTSE 100 index by six percentage points over the same period, this nevertheless represents a disappointing outcome thus far.

More encouragingly, the company’s latest trading update showed that like-for-like sales increased by 6.4pc in the 19 weeks to Jan 6. This prompted an increase in the company’s financial guidance for the year: it now expects adjusted retail operating profits of around £2.8bn, against a previous forecast of between £2.6bn and £2.7bn.

Clearly, Tesco’s financial performance could prove to be somewhat volatile in the short run as a result of Britain’s uncertain economic outlook. However, its low valuation more than adequately compensates investors for this risk, while its solid market position highlights its long-term growth potential as inflation falls, interest rates are cut and consumer confidence continues to improve.

Therefore, the company remains a worthwhile purchase with the capacity to generate far greater outperformance of the market than that recorded since our original tip.

Questor says: buy

Ticker: TSCO

Share price at close: 277.6p

Read the latest Questor column on telegraph.co.uk every Monday, Tuesday, Wednesday, Thursday and Friday from 6am

Read Questor’s rules of investment before you follow our tips