Yahoo Finance

Yahoo Finance Sinking Profits Bring Reality Check to AI-Driven Rally in Emerging Market Stocks

(Bloomberg) -- Just as enthusiasm over artificial intelligence and China’s stimulus fades, a familiar weakness has come back to haunt equity investors in emerging markets: sinking corporate profits.

Most Read from Bloomberg

Key Engines of US Consumer Spending Are Losing Steam All at Once

GameStop Shares Surge as Gill’s Reddit Return Shows Huge Bet

Mnuchin Chases Wall Street Glory With His War Chest of Foreign Money

Homebuyers Are Starting to Revolt Over Steep Prices Across US

AMLO Protege Sheinbaum Becomes First Female President in Mexico

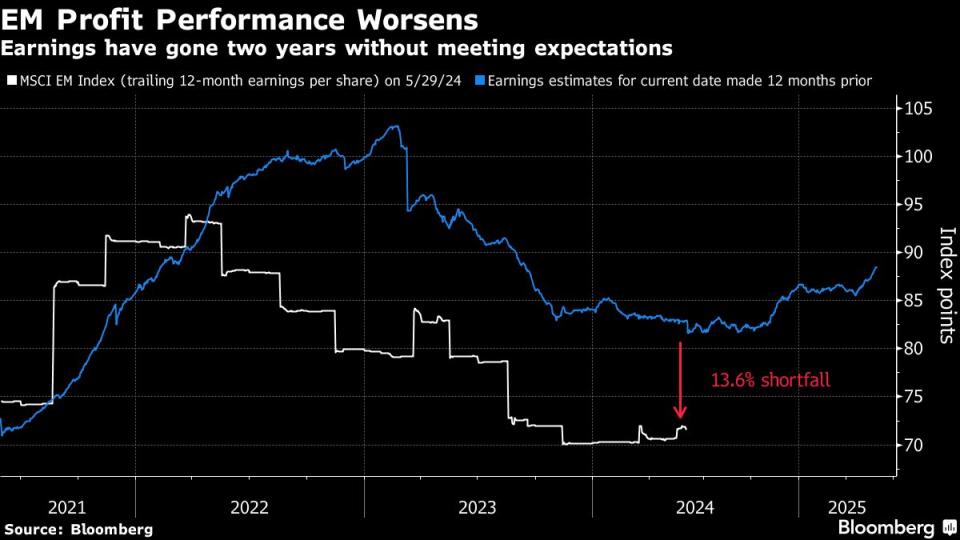

With 96% of companies in the MSCI Emerging Markets Index done with their quarterly results, the earnings season is almost over. And the picture isn’t pretty — Almost half of the companies have missed analyst estimates, average profits have slumped 10% compared with the prior-year period and for every dollar of predicted earnings, companies are bringing home only 86 cents. Two years ago an 18% rise in profits helped EM companies smash projections.

That suggests EM stocks could struggle to sustain a $2.1 trillion rally that’s been driven by trends such as the rush into AI-related stocks and optimism about a quick, stimulus-driven economic recovery in China. Those wagers are waning as the world’s second-largest economy suffers from weak consumer demand and a price war among AI companies spooks money managers.

“The downside surprise in profit expectations is largely driven by weak earnings momentum in China,” said Nenad Dinic, an equity strategist at Bank Julius Baer in Zurich. Elsewhere, “the erosion in margins appears to come from rising operating expenses,” he said, pointing to wage increases in Brazil, Colombia, Mexico and India.

The latest earnings season marks eight quarters of misses for the average emerging-market company, based on a comparison of trailing 12-month earnings per share for the MSCI index and earnings estimates compiled by Bloomberg. Companies’ results are trailing investor expectations so much that profits have to jump 24% over the next year just to catch up with current forecasts.

“That’s definitely a risk for the EM stock rally,” said Marcus Weyerer, a senior ETF investment strategist at Franklin Templeton Investment Management Ltd. “If we see disappointments in earnings continue, then at some point it’ll have an effect,” he said. Stocks could decline by 10% to 15% if companies continue to miss estimates, Weyerer said. “However, certain markets like India have also broadly delivered so far”.

The MSCI EM index advanced 15% from Jan. 17 through May 20, before weaker sentiment toward AI stocks triggered a 4.8% fall through May 31. Technology stocks from China and the AI hubs Taiwan and South Korea were leading the declines. The index was rebounding Monday, with India’s stocks surging to a record as exit polls indicated a resounding victory for Prime Minister Narendra Modi’s party.

Chinese mainland companies in the past quarter reported the weakest earnings since April 2018, soon after the trade war between the US and China began. Hong Kong-listed Chinese companies posted results that showed a marginal recovery after hitting the lowest level in at least a decade.

Stingy Consumers

Sluggish consumer spending is one cause for poor corporate performance not just in China, but across emerging markets.

For instance, Unilever Plc’s Indian unit reported a 5.5% drop in net income for the first quarter, missing analyst estimates. Behind the decline was sluggish rural demand combined with high net-worth urban consumers pivoting to other brands. Similar trends can be seen elsewhere, with Chilean retailer Cencosud SA, restaurant chain operator Yum China Holdings Inc. and Swiss-South African jeweler Richemont delivering weaker-than-expected results.

Read more: In China, All Tech Races Descend Into a Price War

Chinese consumers “are looking to conserve wealth,” said James Johnstone, co-head of emerging and frontier markets at Redwheel in London. “The very exciting post-pandemic revenge spending is over and people are tightening their belts.”

Unlike China, where deflation helps companies control their costs, other EM countries are struggling after three years of elevated inflation. But competitive pressures and price-sensitive consumers still reeling from the economic impact of Covid mean companies are unable to pass these costs on.

Meanwhile, a price war in AI is putting corporate performance under pressure. Alibaba Group Holding Ltd. dropped prices of some of its services, spurring its rivals to do the same. Investors are balking at the extent of discounts that are being offered — as much as 97% for some services — and reconsidering further investments in that area. A gauge of Chinese tech stocks has slumped 11% in just nine trading days.

On average, the operating-profit margin at EM companies has fallen more than 3 percentage points in the past two years. The deterioration was worst for industrial companies, financial institutions, technology firms and real estate developers, Julius Baer’s research in Asia shows.

Central-Bank Dilemma

There’s one more thing hampering corporate profits: A deceleration in the pace of monetary easing. While some developing countries started cutting interest rates in mid-2023, progress has slowed as delays to the Federal Reserve’s policy pivot and the dollar’s resilience pressure local currencies.

Policymakers, for now, are focusing on supporting their currencies. “Despite room for rate cuts, several EM central banks remain hawkish,” said Dinic. “Poor corporate performance appears to be a secondary concern compared to broader macroeconomic stability.”

What to Watch

Election results from India, Mexico and South Africa are in focus for EM investors.

With eroding support for the ruling party in South Africa, the focus will be on coalition talks amid hopes for a market-friendly alliance

In India, exit polls signaled an emphatic victory for Prime Minister Narendra Modi’s ruling party

The peso tumbled after Claudia Sheinbaum secured a landslide victory to become Mexico’s first female president

China’s manufacturing activity expanded at the fastest pace in almost two years in May, according to a private survey, contrasting with weak official data that dented the country’s growth outlook.

Several emerging economies will report inflation, trade and growth data, which investors will use to gauge the path of monetary policy.

Poland’s central bank is expected to keep the policy rate unchanged at its June 5 meeting, extending the pause since the last cut in October 2023. Headline inflation broadly remains within target.

Kenya on June 5 and India on June 7 are also expected to leave their benchmark borrowing costs unchanged as EM central banks turn cautious on easing amid delays to rate changes by the Federal Reserve.

(Updates with more comments in the sixth paragraph)

Most Read from Bloomberg Businessweek

Disney Is Banking On Sequels to Help Get Pixar Back on Track

The Budget Geeks Who Helped Solve an American Economic Puzzle

Israel Seeks Underground Secrets by Tracking Cosmic Particles

How Rage, Boredom and WallStreetBets Created a New Generation of Young American Traders

©2024 Bloomberg L.P.