Yahoo Finance

Yahoo Finance We Think Shareholders May Want To Consider A Review Of Emmerson Resources Limited's (ASX:ERM) CEO Compensation Package

The results at Emmerson Resources Limited (ASX:ERM) have been quite disappointing recently and CEO Rob Bills bears some responsibility for this. Shareholders will be interested in what the board will have to say about turning performance around at the next AGM on 24 November 2022. This will be also be a chance where they can challenge the board on company direction and vote on resolutions such as executive remuneration. From our analysis, we think CEO compensation may need a review in light of the recent performance.

Check out our latest analysis for Emmerson Resources

Comparing Emmerson Resources Limited's CEO Compensation With The Industry

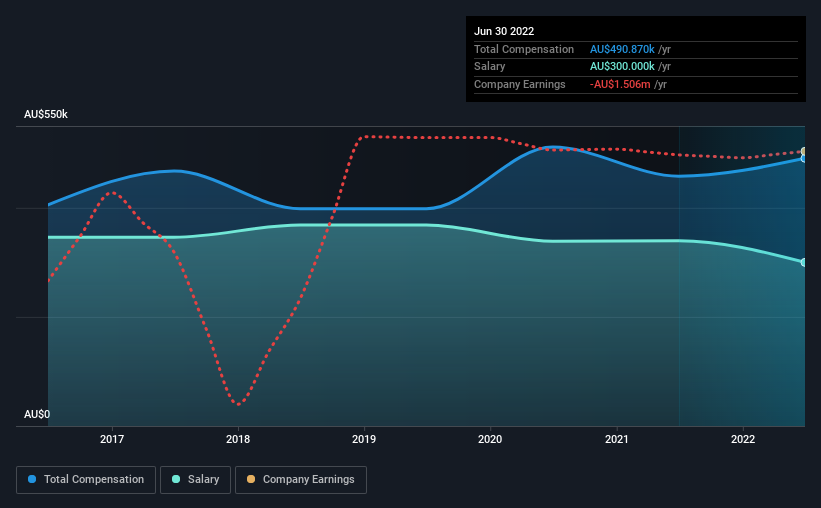

According to our data, Emmerson Resources Limited has a market capitalization of AU$47m, and paid its CEO total annual compensation worth AU$491k over the year to June 2022. That's a modest increase of 7.2% on the prior year. In particular, the salary of AU$300.0k, makes up a huge portion of the total compensation being paid to the CEO.

For comparison, other companies in the industry with market capitalizations below AU$296m, reported a median total CEO compensation of AU$366k. Hence, we can conclude that Rob Bills is remunerated higher than the industry median. Furthermore, Rob Bills directly owns AU$758k worth of shares in the company, implying that they are deeply invested in the company's success.

Component | 2022 | 2021 | Proportion (2022) |

Salary | AU$300k | AU$340k | 61% |

Other | AU$191k | AU$118k | 39% |

Total Compensation | AU$491k | AU$458k | 100% |

Talking in terms of the industry, salary represented approximately 60% of total compensation out of all the companies we analyzed, while other remuneration made up 40% of the pie. Our data reveals that Emmerson Resources allocates salary more or less in line with the wider market. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Emmerson Resources Limited's Growth

Emmerson Resources Limited saw earnings per share stay pretty flat over the last three years. In the last year, its revenue is down 44%.

A lack of EPS improvement is not good to see. And the impression is worse when you consider revenue is down year-on-year. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Emmerson Resources Limited Been A Good Investment?

Since shareholders would have lost about 22% over three years, some Emmerson Resources Limited investors would surely be feeling negative emotions. So shareholders would probably want the company to be less generous with CEO compensation.

To Conclude...

Along with the business performing poorly, shareholders have suffered with poor share price returns on their investments, suggesting that there's little to no chance of them being in favor of a CEO pay raise. At the upcoming AGM, the board will get the chance to explain the steps it plans to take to improve business performance.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. In our study, we found 3 warning signs for Emmerson Resources you should be aware of, and 1 of them is potentially serious.

Important note: Emmerson Resources is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here