Yahoo Finance

Yahoo Finance Three Growth Companies On The Japanese Exchange With High Insider Ownership And A Minimum Of 18% Earnings Growth

Amid a backdrop of a strengthening Japanese stock market, with the Nikkei 225 Index climbing by 2.6% and the TOPIX Index up by 3.1%, investors are keenly observing movements within Japan's financial landscape. In such an environment, growth companies with high insider ownership can be particularly compelling, as this combination often suggests confidence from those closest to the company in its future prospects and alignment of interests between shareholders and management.

Top 10 Growth Companies With High Insider Ownership In Japan

Name | Insider Ownership | Earnings Growth |

SHIFT (TSE:3697) | 35.4% | 27% |

Kanamic NetworkLTD (TSE:3939) | 25% | 28.9% |

Hottolink (TSE:3680) | 27% | 57.4% |

Medley (TSE:4480) | 34% | 28.7% |

Micronics Japan (TSE:6871) | 15.3% | 39.8% |

Kasumigaseki CapitalLtd (TSE:3498) | 34.8% | 44.6% |

ExaWizards (TSE:4259) | 24.8% | 91.1% |

Soiken Holdings (TSE:2385) | 19.8% | 118.4% |

AeroEdge (TSE:7409) | 10.7% | 28.5% |

freee K.K (TSE:4478) | 24% | 72.9% |

Let's dive into some prime choices out of from the screener.

Mercari

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Mercari, Inc. operates a marketplace application in Japan and the United States, focusing on buying and selling a wide range of products, with a market capitalization of approximately ¥344.47 billion.

Operations: The company generates revenue primarily through its marketplace applications active in both Japan and the United States.

Insider Ownership: 36%

Earnings Growth Forecast: 18.9% p.a.

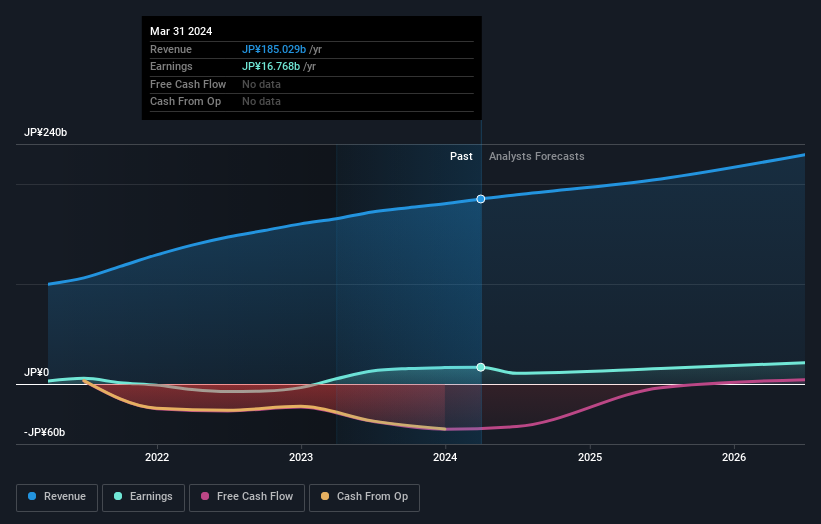

Mercari, a growth-focused company in Japan with significant insider ownership, is poised for continued expansion. Despite a volatile share price recently, Mercari's revenue and earnings growth outpace the Japanese market averages significantly, with revenues expected to grow by 9.7% annually and earnings by 18.9%. The firm projects robust financials for the fiscal year ending June 30, 2024, including JPY 190 billion in revenue and JPY 12 billion profit attributable to owners. However, its annual earnings growth does not exceed the high threshold of 20%.

Get an in-depth perspective on Mercari's performance by reading our analyst estimates report here.

Our valuation report unveils the possibility Mercari's shares may be trading at a premium.

Rakuten Group

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Rakuten Group, Inc. operates in e-commerce, fintech, digital content, and communications sectors globally with a market capitalization of approximately ¥1.85 trillion.

Operations: The company generates revenue through its involvement in e-commerce, fintech, digital content, and communications sectors.

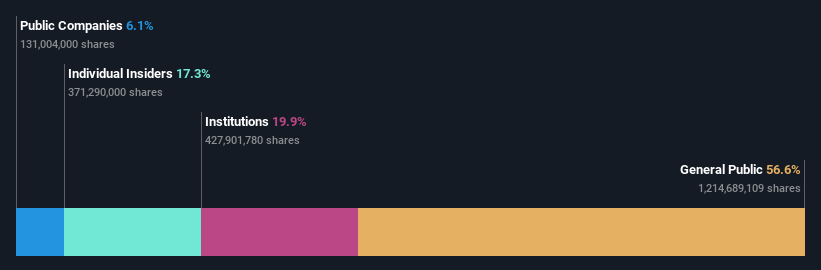

Insider Ownership: 17.3%

Earnings Growth Forecast: 83.2% p.a.

Rakuten Group, positioned below its estimated fair value by 79.8%, is on track to profitability within three years amid a forecasted annual revenue growth of 7.7%, outpacing the Japanese market's 4.2%. However, its projected Return on Equity at 9.4% remains modest. Recent corporate guidance anticipates double-digit growth in operating results for FY2024, excluding its securities segment affected by market volatility, complemented by a substantial $1.99 billion fixed-income offering to bolster financial flexibility.

BayCurrent Consulting

Simply Wall St Growth Rating: ★★★★☆☆

Overview: BayCurrent Consulting, Inc. offers consulting services across various industries in Japan, with a market capitalization of approximately ¥506.75 billion.

Operations: The firm generates its revenue by offering consultancy across diverse sectors in Japan.

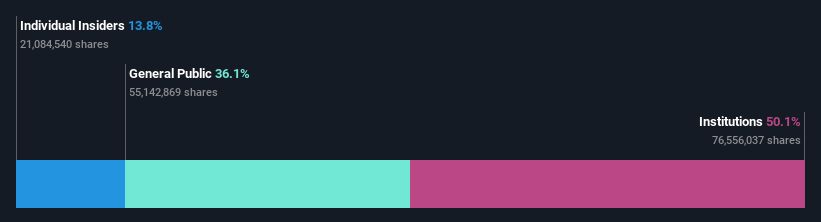

Insider Ownership: 13.9%

Earnings Growth Forecast: 18.4% p.a.

BayCurrent Consulting, with a recent share buyback totaling ¥3.6 billion, underscores its commitment to shareholder value and capital efficiency. Despite a highly volatile share price recently, the company's earnings are expected to grow by 18.36% annually, outpacing the Japanese market average of 8.9%. While its revenue growth forecast of 18.3% slightly trails the ambitious 20% threshold, it still exceeds the broader market's forecast of 4.2%. The firm also boasts a robust projected Return on Equity of 33.4% in three years, indicating efficient management and profitability potential despite not being at the top for insider ownership growth metrics in Japan.

Taking Advantage

Navigate through the entire inventory of 98 Fast Growing Japanese Companies With High Insider Ownership here.

Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Curious About Other Options?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include TSE:4385 TSE:4755 and TSE:6532.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com