Yahoo Finance

Yahoo Finance Uber (NYSE:UBER): Long-Term Growth Story Continues Despite Robotaxi Fears

Uber (NYSE:UBER), the leading ridesharing company, has demonstrated strong performance throughout the past 12 months despite experiencing setbacks in Q1 that caused its stock to lose some ground. Looking ahead in the long term, the growth trajectory in both the bottom and top lines seems robust. This is despite the potential threat posed by the transition to autonomous vehicles (AVs) to the company’s business model. Therefore, I currently maintain a cautiously bullish stance on Uber.

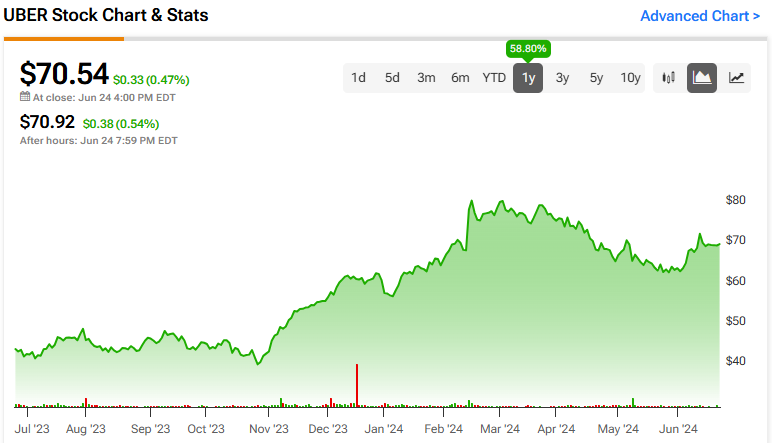

Why UBER Is Down Since Its All-Time Highs

Since reaching its all-time high peak in mid-February this year, Uber’s stock has underperformed and specific reasons for this became clearer following the Q1 results released in May.

First, there has been a significant shift in the composition of Uber’s core business. In Q1 2020, the Mobility segment (rides) contributed to around 70% of Uber’s revenues. Today, however, this figure has decreased to 56%, largely because Uber has expanded its presence in Deliveries (Uber Eats), which has become a major part of its business in recent years.

Comparing gross bookings in Q1 2024 to the same period last year, there was an overall increase of 20%. Within specific segments, the Mobility segment grew by 30% year-over-year in Q1 2024, down from 39% growth in Q1 2023. In contrast, Delivery gross bookings increased by 18% year-over-year in Q1 2024, up from 8% growth in Q1 2023.

I believe that the market has reacted negatively because Uber’s growth is slowing down due to its shift away from Mobility, its traditional core business that historically played a crucial role in its growth and valuation.

Another factor impacting Uber’s bottom line in Q1, leading to a loss of $654 million, was a non-recurring event. Uber reported a $721 million charge related to equity investments in other companies, such as DiDi (OTC:DIDIY). As the value of these investments dropped, Uber had to account for this decrease in value on its financial statements. While addressing these issues was the right move for transparency, it certainly delivered a one-punch hit to the stock price.

Will Autonomous Driving Hurt or Help UBER?

Another factor that may be affecting the company’s stock in the near term is the buzz surrounding Tesla’s (NASDAQ:TSLA) robotaxi strategy. Tesla’s plan to own and operate a fleet of robotaxis has sparked discussions about the potential impact of autonomous vehicles on Uber’s business model.

While this could potentially shape the future landscape of ridesharing, if Uber moves towards adopting this disruptive technology, several assumptions can be made.

Uber’s transition to autonomous vehicles presents financial challenges due to the upfront costs of acquiring and maintaining an AV fleet. Currently, Uber’s drivers bear these costs themselves. However, if Uber shifts to AVs, it would need to invest in purchasing or leasing these vehicles, which could be expensive initially.

Despite these initial costs, this transition would involve Uber deploying AVs as robotaxis, maximizing fleet utilization and operational efficiency. AVs could operate almost continuously, unlike traditional vehicles that often sit idle.

At any rate, according to Uber’s CEO, Dara Khosrowshahi, the company is well-positioned to navigate and thrive through the transition to autonomous vehicles. He also mentioned that Tesla’s robotaxi project will require tools that Uber already possesses to make financial sense.

“I don’t think it’s going to be all Robotaxi anytime soon, and we think that when the technology comes in, there will be a transition. You will have essentially hybrid networks. And going through that transition, we think we’re uniquely situated as a marketplace to assess and have any and all safe AV tech along with human drivers on our network.”

It’s noteworthy that Uber sold its autonomous vehicle unit to Aurora four years ago but continues its partnership. This smart move, in my view, should help Uber reduce operating costs while leveraging technology at scale.

What Lies Ahead for Uber?

Peering into Uber’s future, while forecasting the impact of autonomous vehicles (AVs) remains challenging, other factors are more predictable at this time, which I perceive as significant long-term risks.

One major concern is growing regulatory pressures. Despite being familiar with regulatory challenges, Uber’s size and market dominance make it a prime target for regulators. Legal battles and regulatory actions could potentially weigh on the company’s future profitability.

However, I believe Uber’s key segments’ growth potential should remain robust for at least the next couple of years.

In terms of financial performance, Uber is expected to see growth in both its bottom and top lines throughout 2024. Revenue is projected to grow by 15.8%, while EPS is expected to increase by 2%. This results in a forward price-to-earnings (P/E) ratio of 79x. Looking further ahead to the end of 2025, forecasts suggest a substantial 137.5% growth in profits, potentially yielding EPS of $2.11, alongside a 15% increase in revenues. This would reduce the forward P/E ratio to 33x, making Uber’s valuation much more compelling.

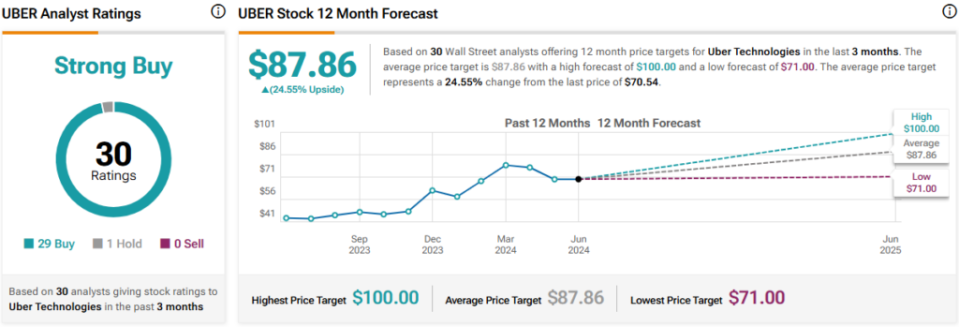

Is UBER Stock a Buy, According to Analysts?

The consensus among Wall Street analysts regarding UBER is a Strong Buy. This is based on 29 Buys and one Hold rating assigned in the past three months. The average UBER stock price target among 30 analysts is $87.86, implying upside potential of 24.6%.

The Bottom Line

While Uber faces challenges such as regulatory scrutiny and potential competition from autonomous vehicles threatening its business model, I believe that the company’s revenue composition shift towards delivery services could prove beneficial in mitigating this risk.

Uber’s revenue and net income growth prospects in the medium-to-long term also appear promising, driven by anticipated improvements in profitability and financial metrics.

Although Uber is not currently considered a low-cost stock, I do not perceive it as expensive relative to its growth profile. Therefore, I remain cautiously optimistic about Uber’s long-term prospects.