Yahoo Finance

Yahoo Finance UK economy ‘not as bad as is often assumed’

A number of analysts have suggested that the economic inheritance for the next government will not be as bad as many fear.

Although the UK slipped into a shallow recession at the end of last year, the economy outperformed expectations in the first quarter of the year, growing 0.7 per cent. This made it the fastest growing economy in the G7.

In a note released today, Simon French, head of research at Panmure Liberum, argued that the economy is “not as bad as is often assumed”, pointing in particular to strong household balance sheets and relatively low government debt.

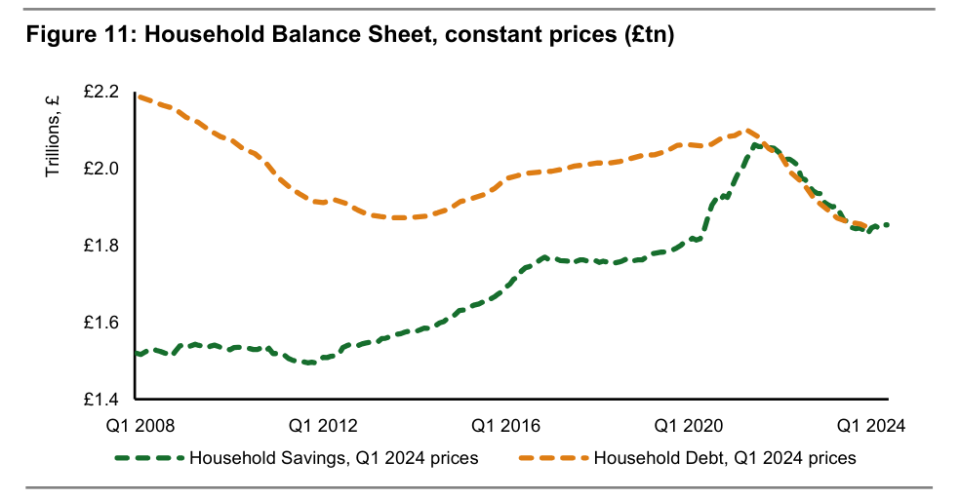

“One of the areas that gets rather less commentary than we feel is justified has been the fifteen-year-long deleveraging that the UK household sector has undertaken,” French wrote.

In 2008 UK households in aggregate were indebted to the tune of £700bn. Since then households have improved their financial position to the extent that now debt and cash balances are equal, at around £1.85 trillion each.

This should mean that households are more confident about going out and spending or taking on a bit more debt, supporting domestic consumption.

While national debt stands at its highest level since the 1960s, approaching 100 per cent of GDP, this is actually the second lowest in the G7, behind only Germany.

“Whatever public sector debt challenges faced by the UK government in the coming years, it won’t be alone – internationally – in facing these challenges,” French wrote.

Sanjay Raja, chief UK economist at Deutsche Bank, was also fairly optimistic about the state of the economy. “The next Government will inherit a stronger economy than most expected coming into 2024,” he wrote in a recent note.

Household disposable income is likely to be the main driver of growth over the course of the year, supported by strong household balance sheets. “Household balance sheets remain healthy, with deposits this year topping loans for the first time on record,” Raja argued.

He also expects businesses to “catch up” on investment levels, which have remained depressed since the Brexit vote.

Looking forward, measures of consumer and business confidence have increased ahead of the general election, which should provide further support to growth over the coming years. The bank expects growth to pick up to around 1.5 per cent in 2025 and 2026.

Capital Economics expects that the next government could also benefit from looser monetary policy. The consultancy expects inflation to remain low for the foreseeable future, enabling the Bank of England to cut interest rates and gilt yields to fall.

“That would mean the next government will start with the economic wind in their sails,” they argued.

French too noted that the cost of servicing debt has already moderated from around four per cent of GDP in the final quarter of 2022 to 2.8 per cent in the first quarter of this year.

Despite the improving economic outlook, the economists agreed that major challenges still needed urgently addressing.

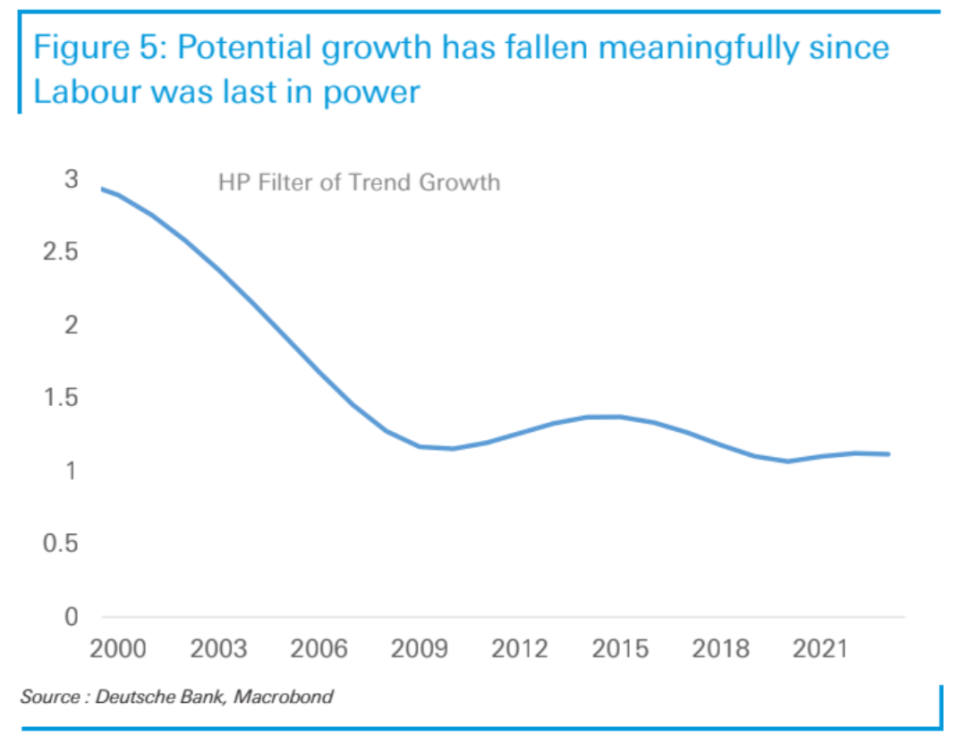

Raja pointed out that potential growth has fallen dramatically over the past 20 years while living standards have barely increased since 2017.

Analysts at Pantheon Macroeconomics also pointed out that the Office for Budget Responsibility (OBR) were already among the most optimistic forecasters.

This means stronger growth will “not magically generate” more funds for spending, because strong growth is already assumed by the OBR.

The “big imponderable” for French was whether Labour has the “requisite backbone” to take on the vested interests and bring about meaningful supply side reform on issues like planning.