Yahoo Finance

Yahoo Finance West Pharmaceutical (WST) Q4 Earnings Beat, Order Book Strong

West Pharmaceutical Services, Inc. WST report adjusted earnings per share (EPS) of $1.77 in the fourth quarter of 2022, down 13.2% year over year. The figure beat the Zacks Consensus Estimate by 27.3%.

The adjustments include expenses related to the amortization of acquisition-related intangible assets, among others.

Our projection of adjusted EPS was $1.37.

GAAP EPS for the quarter was $1.36, down 29.5% year over year.

Revenues in Detail

West Pharmaceutical registered net sales of $708.7 million in the fourth quarter, down 3% year over year. The figure, however, beat the Zacks Consensus Estimate by 8.2%.

The fourth-quarter revenue compares with our estimate of $653.9 million.

Organic net sales growth was 2.6% during the reported period. Our model estimated organic growth to be flat.

Per management, the company’s top line reflects declining demand for pandemic-related product. However, growth in demand, especially from biologic customers, and a strong order book for 2023 buoy optimism. The company remains committed to managing its cost structure for addressing an ongoing inflationary environment. It also plans to expand high-value product manufacturing capacity for supporting accelerating customer demand from recent launches and anticipated drug programs in the coming years.

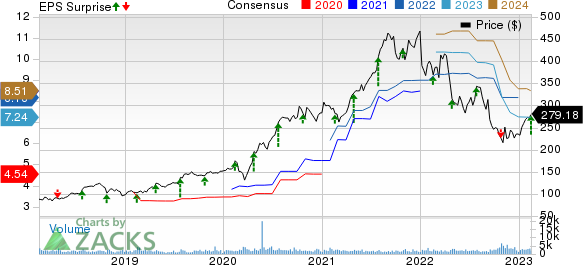

West Pharmaceutical Services, Inc. Price, Consensus and EPS Surprise

West Pharmaceutical Services, Inc. price-consensus-eps-surprise-chart | West Pharmaceutical Services, Inc. Quote

Segmental Details

West Pharmaceutical operates through two segments — Proprietary Products and Contract-Manufactured Products.

Net sales in the Proprietary Products segment amounted to $584.8 million, indicating a year-over-year decline of 4%. Organic net sales growth came in at 1.8%. HVP net sales (components and devices) accounted for approximately 72% of the segment’s net sales and delivered mid-single-digit organic net sales growth. Consumer demand for Crystal Zenith, Envision and film-coated component categories led to an increase in HVP net sales, partially offset by a decline in NovaPure sales related to COVID-19 vaccines.

Generics and Pharma market units of the Proprietary Products segment reflected robust organic growth during the fourth quarter. However, declining sales related to COVID-19 vaccines led to mid-single digit percentage-point decline in organic net sales for Biologics market unit.

In the reported quarter, net sales at the Contract-Manufactured Products segment fell 2% year over year to $123.9 million. However, the segment saw a 7% improvement in organic net sales.

Margins

In the quarter under review, West Pharmaceutical’s gross profit fell 12.8% to $268 million. The gross margin contracted by 410 basis points (bps) to 37%.

Selling, general and administrative expenses fell 12.6% to $85.7 million. Research and development expenses went up 16.1% year over year to $15.9 million.

Adjusted operating profit totaled $158.7 million, indicating a decline of 16.1% from the prior-year quarter. Adjusted operating margin in the fourth quarter contracted by 350 bps to 22.4%.

Full-Year Result

West Pharmaceutical reported revenues of $2.89 billion for full-year 2022, up 2% year over year. Adjusted EPS for 2022 stood at $8.58, flat year-over-year.

Financial Position

West Pharmaceutical exited fourth-quarter 2022 with cash and cash equivalents of $894.3 million compared with $729 million at the end of the third quarter. Total debt at the end of fourth-quarter 2022 was $208.9 million compared with $209.4 million at the end of the third quarter.

Cumulative net cash flow from operating activities at the end of fourth-quarter 2022 was $724 million compared with $584 million a year ago.

Meanwhile, West Pharmaceutical has a consistent dividend-paying history, with five-year annualized dividend growth of 6.43%. Management announced fourth-quarter 2022 dividend of 19 cents per share, representing the 30th consecutive annual increase in West Pharmaceutical’s dividend.

2023 Guidance

West Pharmaceutical issued its full-year 2023 outlook.

Net sales for full-year 2023 are projected between $2.935 billion and $2.960 billion. The Zacks Consensus Estimate for the same is currently pegged at $2.86 billion.

Organic sales growth is now estimated to be approximately 3-4%.

West Pharmaceutical expects full-year COVID-19-related net sales of approximately $85 million in 2023.

West Pharmaceutical now projects its adjusted EPS in the range of $7.25-$7.40. The Zacks Consensus Estimate for the same is currently pegged at $7.24 per share.

Our Take

West Pharmaceutical exited the fourth quarter of 2022 with better-than-expected results. Although the top line declined, demand growth and a strong order book for 2023 are encouraging. The company’s revenue outlook beat market estimates. However, the contraction in the gross margin and operating margin do not bode well.

On a positive note, West Pharmaceutical’s Proprietary Products segment registered growth in its organic net sales, which is encouraging. Continued strong demand for the company’s Crystal Zenith, Envision and film-coated component categories is encouraging. Double-digit organic net sales growth in the Generics market unit and high-single-digit organic net sales growth in the Pharma market unit are other quarterly highlights.

Zacks Rank and Stocks to Consider

Currently, West Pharmaceutical carries a Zacks Rank #3 (Hold).

Some better-ranked stocks in the broader medical space that have announced quarterly results are Cardinal Health, Inc. CAH, McKesson Corporation MCK and Hologic, Inc. HOLX.

Cardinal Health, carrying a Zacks Rank #2 (Buy), reported second-quarter fiscal 2023 adjusted EPS of $1.32, beating the Zacks Consensus Estimate by 16.8%. Revenues of $51.47 billion outpaced the consensus mark by 2%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Cardinal Health has a long-term estimated growth rate of 11.6%. CAH’s earnings surpassed estimates in two of the trailing four quarters and missed the same in the other two, the average being 6.4%.

McKesson, having a Zacks Rank #2, reported third-quarter fiscal 2023 adjusted EPS of $6.90, which beat the Zacks Consensus Estimate by 8.8%. Revenues of $70.49 billion outpaced the consensus mark by 0.02%.

McKesson has a long-term estimated growth rate of 10.4%. MCK’s earnings surpassed estimates in two of the trailing four quarters and missed the same in the other two, the average being 3.4%.

Hologic reported first-quarter fiscal 2023 adjusted earnings of $1.07 per share, beating the Zacks Consensus Estimate by 18.9%. Revenues of $1.07 billion surpassed the Zacks Consensus Estimate by 9.5%. It currently sports a Zacks Rank #1.

Hologic has a long-term estimated growth rate of 15.2%. HOLX’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 30.6%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cardinal Health, Inc. (CAH) : Free Stock Analysis Report

McKesson Corporation (MCK) : Free Stock Analysis Report

Hologic, Inc. (HOLX) : Free Stock Analysis Report

West Pharmaceutical Services, Inc. (WST) : Free Stock Analysis Report