Yahoo Finance

Yahoo Finance Factoring time into your investments

Stocks fell last week, with the S&P 500 falling 2.9% to close at 4,320.06. It was the worst week since March. The index is now up 12.5% year to date, up 20.8% from its Oct. 12 closing low of 3,577.03, and down 9.9% from its Jan. 3, 2022 record closing high of 4,796.56.

It’s been a rough couple of weeks in the stock market. After hitting its 2023 closing high of 4,588.96 on July 31, the S&P has been struggling to regain its footing.

But as TKer Stock Market Truth No. 2 reminds us, it’s typical for stocks to experience big drawdowns in any given year. Dealing with market volatility is what investing in risky assets like stocks is all about.

This market slump has had me thinking about a discussion I recently participated in with Bespoke Investment Group’s Paul Hickey and CappThesis’ Frank Cappelleri on the Facts vs. Feelings podcast, hosted by Carson Group’s Ryan Detrick and Sonu Varghese.

As we were wrapping up, Ryan asked us for a timeless piece of investing advice. All of our answers hit on a similar theme. Here’s a lightly edited transcript from the podcast:

Frank: Know your timeframe. And don’t change. You can either be a trader, a short-term trader. Or if you’re long term, I think you have to be market agnostic.

Paul: Your holding period. A one-day holding period, it’s a coin flip. The longer you’re willing to stick to it, the better. We call it the Montana rule. … Markets have never been down over a 16-year stretch or longer. Time heals in the markets.

Me: Time in the market beats timing the market.

Regardless of if you’re trading for the short term or investing for the long term, making money in the stock market is a process. And processes involve time.

So, whether you’re a chart guru like Frank or you’re a data god like Paul, the key variable when considering a trade or an investment is time.

'Time heals in the markets'

In some cases, it might be appropriate to operate on tight timeframes. In many other cases, the move is to have a long timeframe.

The chart below backs up Paul’s observation. From Bespoke Investment Group: "Historically, the odds of the S&P 500 being up over any one-month timeframe have been 62.6%. Over a year, the odds of being up jump to 74.6%, and over eight years, they jump to 97%. Since 1928, all 16+ year time frames have seen positive returns."

And by the way, this only works if you stay put in the market. The more you weave in and out of the market, the more you risk missing out on those important stretches of gains that can make or break your long-term performance. As the saying goes, "Time in the market beats timing the market."

In the stock market, time pays. It’s the valuable edge investors can take advantage of as they build long-term wealth in a market where the long game is undefeated.

Check out the whole episode of Facts vs. Feelings on Apple Podcasts, Amazon Music, Spotify, YouTube, or wherever you get podcasts!

Reviewing the macro crosscurrents

There were a few notable data points and macroeconomic developments from last week to consider:

The Fed keeps rates unchanged. On Wednesday, the Federal Reserve kept monetary policy tight, leaving its target for the federal funds rate unchanged at a range of 5.25% to 5.5%.

From the Fed’s policy statement: "Recent indicators suggest that economic activity has been expanding at a solid pace. Job gains have slowed in recent months but remain strong, and the unemployment rate has remained low. Inflation remains elevated."

The Fed also raised its estimates for GDP growth in 2023, and 2024; lowered its estimates for the unemployment rate in 2023, 2024, and 2025; and lowered its estimate for core PCE inflation in 2023. It also raised its projection for the fed funds rate in 2024 to 5.1% from 4.6%. Taken together, these revisions were considered hawkish.

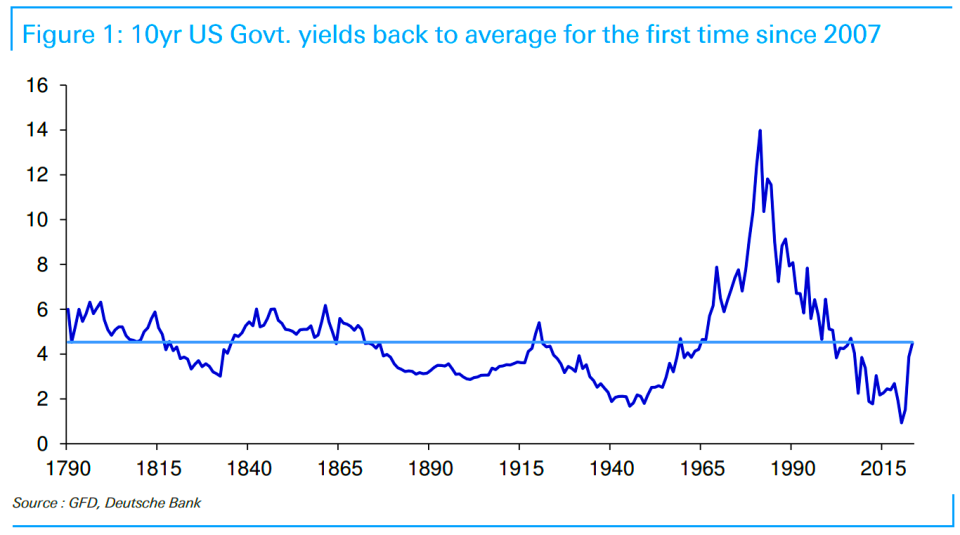

Interest rates are up. The yield on the 10-year Treasury note hit 4.5% for the first time since 2007.

While rising interest rates represent a headwind for consumers and businesses, keep in mind that consumer and business finances are unusually strong.

Household finances are in good shape. From WSJ’s Nick Timiraos: "Debt service payments as a share of household income edged ever so slightly *lower* in Q2 from the previous quarter and from the year-earlier quarter."

Unemployment claims fall. Initial claims for unemployment benefits declined to 201,000 during the week ending Sept. 16, down from 220,000 the week prior. It was the lowest print since January. While this is up from a September 2022 low of 182,000, it continues to trend at levels associated with economic growth.

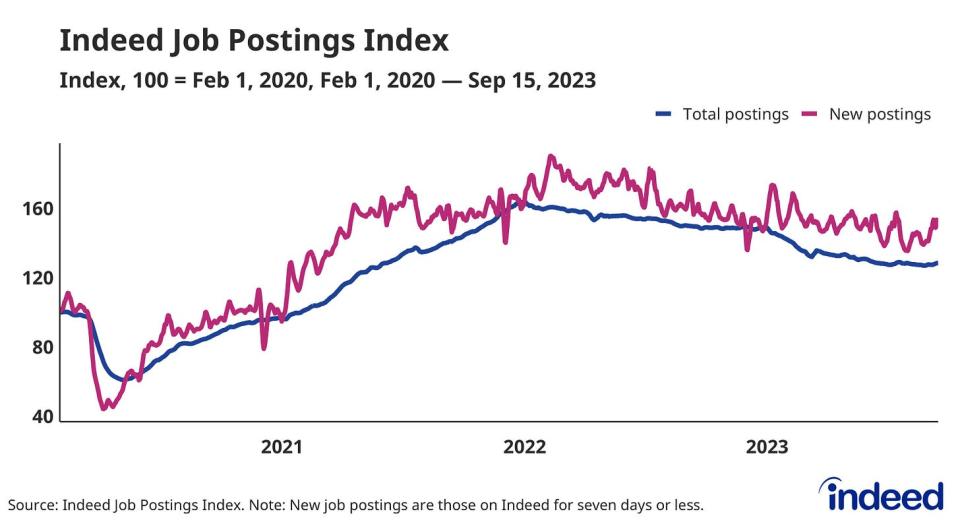

Job openings stabilize. From Indeed’s Nick Bunker: "Online job postings aren't falling like they were earlier this year. In fact, they aren't falling at all. The Indeed Job Postings Index has moved sideways over the past 3 months."

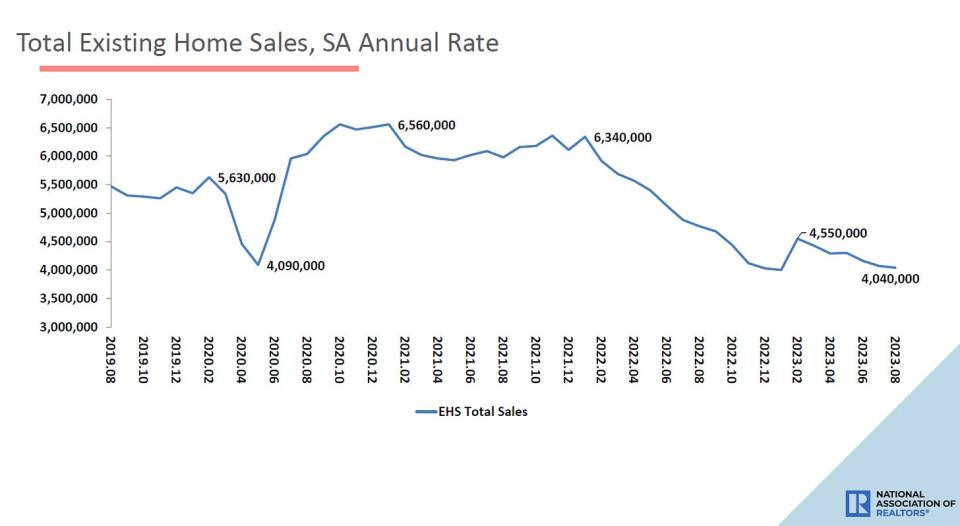

Home sales cool. Sales of previously owned homes fell 0.7% in August to an annualized rate of 4.04 million units. From NAR chief economist Lawrence Yun: "Mortgage rate changes will have a big impact over the short run, while job gains will have a steady, positive impact over the long run. The South had a lighter decline in sales from a year ago due to greater regional job growth since coming out of the pandemic lockdown."

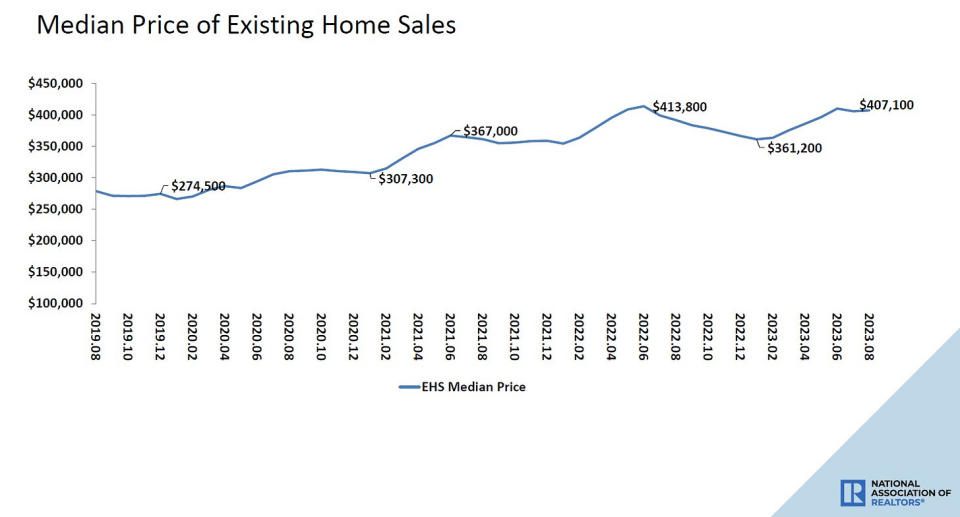

Home prices ticked up. Prices for previously owned homes rose month over month and were up from year-ago levels. From the NAR: "The median existing-home sales price climbed 3.9% from one year ago to $407,100 — the third consecutive month the median sales price surpassed $400,000."

Homebuilder sentiment falls. From the NAHB’s Alicia Huey: "The two-month decline in builder sentiment coincides with when mortgage rates jumped above 7% and significantly eroded buyer purchasing power. … And on the supply-side front, builders continue to grapple with shortages of construction workers, buildable lots and distribution transformers, which is further adding to housing affordability woes. Insurance cost and availability is also a growing concern for the housing sector."

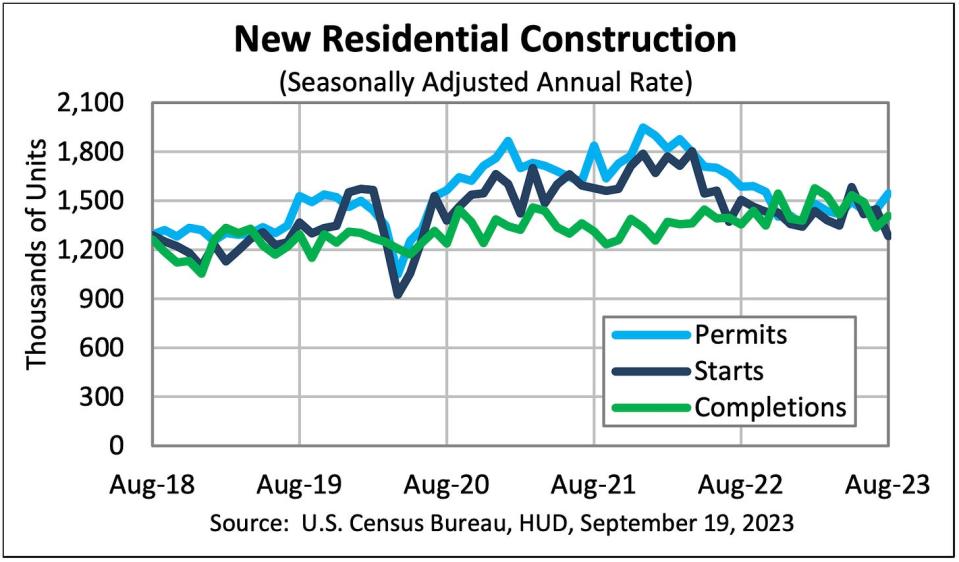

New home construction drops. Housing starts fell 11.3% in August to an annualized rate of 1.28 million units, according to the Census Bureau. Building permits rose 6.9% to an annualized rate of 1.54 million units.

Gas prices are up from a year ago. From AAA: "The national average for a gallon of gas hit what may be 2023’s peak price of $3.88 earlier this week, only to slide a few cents in the following days. Today’s average is $3.86 — a penny more than a week ago."

Spending is holding up, according to September card data. From JPMorgan Chase: "As of 17 Sep 2023, our Chase Consumer Card spending data (unadjusted) was 0.5% above the same day last year. Based on the Chase Consumer Card data through 17 Sep 2023, our estimate of the US Census September control measure of retail sales m/m is 0.23%."

The entrepreneurial spirit is alive. Small business applications, while down slightly from the previous month, remain well above prepandemic levels. From the Census Bureau: "August 2023 Business Applications were 466,163, down 0.9% (seasonally adjusted) from July. Of those, 149,785 were High-Propensity Business Applications."

Survey says growth is cooling. From S&P Global’s September Flash US PMI: "PMI data for September added to concerns regarding the trajectory of demand conditions in the US economy following interest rate hikes and elevated inflation. Although the overall Output Index remained above the 50.0 mark, it was only fractionally so, with a broad stagnation in total activity signalled for the second month running."

But… : "Despite a muted sales environment, US businesses registered greater hiring activity during September. The rate of job creation quickened to the fastest since May and was solid overall. In fact, the pace of employment growth was among the most elevated seen in the past year amid some reports that staff retention was improving. Companies also noted that vacancies were filled with greater ease than had been seen in recent months."

Keep in mind that soft survey data isn’t quite as reliable as hard data.

Most US states are still growing. From the Philly Fed’s State Coincident Indexes report: "Over the past three months, the indexes increased in 40 states, decreased in eight states, and remained stable in two, for a three-month diffusion index of 64. Additionally, in the past month, the indexes increased in 30 states, decreased in 13 states, and remained stable in seven, for a one-month diffusion index of 34."

Near-term GDP growth estimates remain positive. The Atlanta Fed’s GDPNow model sees real GDP growth climbing at a 4.9% rate in Q3.

Putting it all together

We continue to get evidence that we could see a bullish "Goldilocks" soft landing scenario where inflation cools to manageable levels without the economy having to sink into recession.

This comes as the Federal Reserve continues to employ very tight monetary policy in its ongoing effort to bring inflation down. While it’s true that the Fed has taken a less hawkish tone in 2023 than in 2022, and most economists agree that the final interest rate hike of the cycle has either already happened or is near, inflation still has to cool more before the central bank is comfortable with price stability.

So we should expect the central bank to keep monetary policy tight, which means we should be prepared for tight financial conditions (e.g., higher interest rates, tighter lending standards, and lower stock valuations) to linger. All this means monetary policy will be unfriendly to markets for the time being, and the risk the economy slips into a recession will be relatively elevated.

At the same time, we also know that stocks are discounting mechanisms, meaning that prices will have bottomed before the Fed signals a major dovish turn in monetary policy.

Also, it’s important to remember that while recession risks may be elevated, consumers are coming from a very strong financial position. Unemployed people are getting jobs, and those with jobs are getting raises.

Similarly, business finances are healthy as many corporations locked in low interest rates on their debt in recent years. Even as the threat of higher debt servicing costs looms, elevated profit margins give corporations room to absorb higher costs.

At this point, any downturn is unlikely to turn into economic calamity, given that the financial health of consumers and businesses remains very strong.

And as always, long-term investors should remember that recessions and bear markets are just part of the deal when you enter the stock market with the aim of generating long-term returns. While markets have had a pretty rough couple of years, the long-run outlook for stocks remains positive.