Yahoo Finance

Yahoo Finance Questor: This unloved electric car engineering firm has real potential

Fund management legend Sir John Templeton once said: “People are always asking me where the outlook is good …. But that’s the wrong question. The right question is ‘where is the outlook most miserable?’”

Management teams may not thank writers and analysts for saying that the outlook is “miserable” at the companies they are running, but Sir John was really trying to focus on the issue of valuation, because when sentiment is depressed that is when there may be bargains to be had. This takes us to relative market newcomer Dowlais (DWL).

Until artificial intelligence (AI) took up the running, there were few as powerful – or hyped – stock narratives as the switch to electric vehicles (EVs) from the internal combustion engine (ICE).

Tesla (TSLA:NDQ) led the charge, spearheading a whole new industry thanks to its charismatic and voluble leader, a first-mover advantage, carbon tax credits and – aided by the equity market – plenty of cash to burn.

But even Tesla’s shares are now down by more than half from their high, as the company’s peak stock market valuation of $1.2 trillion (£947bn) proved hard to sustain in a mass-market automotive industry where profit margins are generally single-digit and competition is fierce.

A further complication is a slowdown in demand for EVs, as the buying public baulks at a combination of the initial purchase price and the cost of insurance and availability of spare parts, while worrying at the same time about mileage ranges and the ease (or otherwise) of finding a charging point when it is needed.

This slowdown is taking its toll on a range of EV industry players and especially their share prices. Fisker filed for bankruptcy protection in the USA just last week, and it joined Lordstown Motors and Proterra as it did so.

Meanwhile, the share prices of other EV makers, such as Nikola (NKLA:NDQ), VinFast Auto (VFS:NDQ), Lucid Motors (LCID:NDQ), Faraday Future (FFIE:NDQ) and Polestar (PSNY:NDQ) have all skidded to a quite alarming degree.

As such, investors’ perception of the EV industry now seems to be tinged with scepticism, if not downright pessimism and the UK-listed Dowlais is not proving immune.

Spun out of FTSE 100 index constituent GKN (GKN) in April 2023, Dowlais has three operating units – Automotive, Power Metallurgy and a start-up hydrogen energy start-up business. Dowlais is a world leader in global drives for cars, both ICE and EV, through its powertrain and drive expertise.

Shareholders in GKN got one Dowlais share for every GKN share that they held at the time of the demerger and it has been a very bumpy journey ever since, in that Dowlais’ share price has pretty much halved.

The full-year results for 2023, published in March, were solid on an underlying basis but the headline-grabbing number turned out to be a £450m write-down on the value of the Powder Metallurgy operation that drove the firm into the red.

May’s trading update for the first four months of 2024 offered little succour, as the chief executive offer Liam Butterworth revealed a 1.9pc year-on-year drop in revenues.

Weakness in the ePowertrain business, which is driven by demand for EVs, more than offset strength in driveline (for ICE light vehicles) and powder metallurgy.

As a result, Mr Butterworth suggests that full-year revenues in 2024 would come in slightly below those of 2023, on a constant currency basis, an admission which drowned out the good news about how Dowlais had generated improved operating margins during the early stages of the year, thanks to ongoing efficiency programmes.

We therefore have an industry where perception has changed markedly for the worse and a share price that has gone from the top left of the screen to the bottom right.

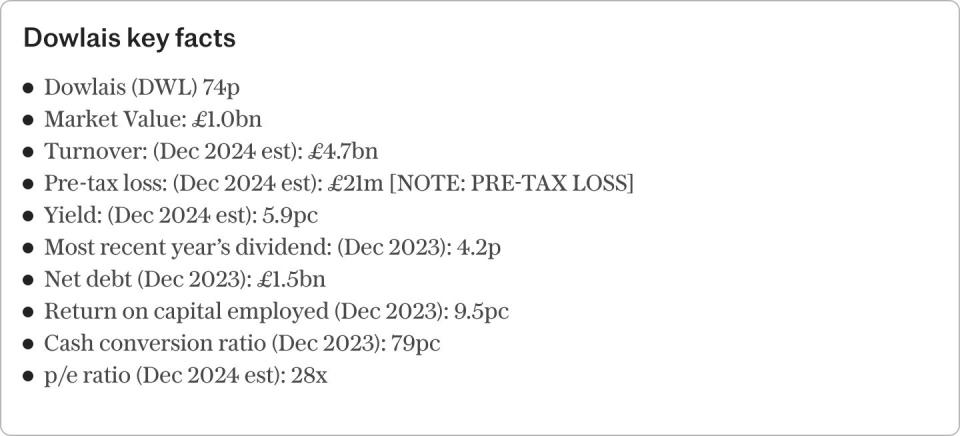

It must be noted that the balance sheet is not pristine, with net liabilities of £1.5bn, adjusting for debt, cash, leases and pensions and from an operational perspective there remains the further risk that automakers develop and produce eDrives for the EVs in-house, rather than get Dowlais to do it for them.

Shares in the FTSE 250 index constituent are therefore not really suitable for widows and orphans.

Yet there is clear potential here, thanks to the company’s competitive position and target market, and also downside protection thanks to the share price swoon, which leaves the shares offering a yield of around 6pc and trading on a very modest multiple of earnings and cash flow on an underlying basis.

A lot of bad news seems to be in the price and although near-term trading could be tough, this looks like a quality engineering business and one that could attract a bidder if the share price languishes for too long.

Questor says: Dive in for Dowlais (Buy)

Ticker: DWL

Share price at close: 74p

Read the latest Questor column on telegraph.co.uk every Sunday, Monday, Tuesday, Wednesday and Thursday from 8pm

Read Questor’s rules of investment before you follow our tips