Yahoo Finance

Yahoo Finance Three ASX Stocks Estimated To Be Trading Up To 43.3% Below Intrinsic Value

The Australian market has shown robust performance, with a notable 10% increase over the past year and the Utilities sector alone gaining 4.1% in just the last week. In such a thriving environment, stocks trading below their intrinsic value present compelling opportunities for investors looking to capitalize on potential growth and earnings forecasted to rise by 14% annually.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

Name | Current Price | Fair Value (Est) | Discount (Est) |

LaserBond (ASX:LBL) | A$0.71 | A$1.21 | 41.3% |

COSOL (ASX:COS) | A$1.23 | A$2.43 | 49.3% |

Charter Hall Group (ASX:CHC) | A$12.10 | A$22.43 | 46% |

ReadyTech Holdings (ASX:RDY) | A$3.17 | A$5.96 | 46.8% |

hipages Group Holdings (ASX:HPG) | A$1.045 | A$1.94 | 46.2% |

Regal Partners (ASX:RPL) | A$3.24 | A$6.17 | 47.5% |

IPH (ASX:IPH) | A$6.45 | A$11.37 | 43.3% |

Millennium Services Group (ASX:MIL) | A$1.145 | A$2.24 | 48.9% |

South32 (ASX:S32) | A$3.64 | A$6.12 | 40.5% |

Treasury Wine Estates (ASX:TWE) | A$12.42 | A$21.36 | 41.9% |

Let's explore several standout options from the results in the screener

Collins Foods

Overview: Collins Foods Limited operates, manages, and administers restaurants across Australia, Europe, and Asia with a market capitalization of approximately A$1.08 billion.

Operations: The company generates revenue through its KFC restaurants in Australia (A$1.09 billion), KFC restaurants in Europe (A$287.06 million), and Taco Bell restaurants (A$52.65 million).

Estimated Discount To Fair Value: 36.8%

Collins Foods, trading at A$9.32, is considered undervalued based on DCF analysis, with a fair value estimated at A$14.75, indicating significant potential upside. Despite recent executive changes with CEO Drew O'Malley stepping down and Kevin Perkins serving as interim CEO, the company's financial outlook remains robust. Analysts predict a 20.53% annual earnings growth over the next three years and revenue growth forecasts outpacing the Australian market average. However, its dividends are poorly covered by earnings and profit margins have declined from last year.

Domino's Pizza Enterprises

Overview: Domino's Pizza Enterprises Limited runs a chain of pizza delivery and carryout restaurants, with a market capitalization of approximately A$3.32 billion.

Operations: The company generates its revenue primarily from its network of pizza restaurants, which brought in A$2.48 billion.

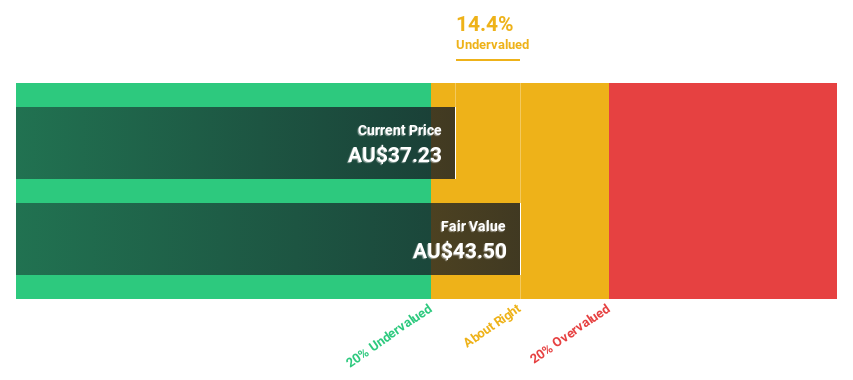

Estimated Discount To Fair Value: 14.4%

Domino's Pizza Enterprises, priced at A$37.23, trades below the calculated fair value of A$43.5, reflecting a modest undervaluation based on cash flow analysis. The company is expected to see robust earnings growth at 28.2% annually, outpacing the broader Australian market's 13.7%. However, revenue growth projections are moderate at 6.4% per year and financial leverage remains high with significant debt levels impacting its balance sheet stability.

IPH

Overview: IPH Limited operates as a provider of intellectual property services and products across regions including Australia, New Zealand, Asia, and Canada, with a market capitalization of approximately A$1.57 billion.

Operations: The company's revenue is generated from intellectual property services in Asia (A$120.45 million), Canada (A$134.91 million), and Australia & New Zealand (A$284.78 million).

Estimated Discount To Fair Value: 43.3%

IPH, valued at A$6.45, is perceived as undervalued with a fair value estimate of A$11.37 based on discounted cash flows, suggesting significant potential upside. The company's earnings are expected to grow by 16% annually, surpassing the Australian market forecast of 13.7%. Despite this growth, its dividend coverage is weak and shareholder dilution has occurred over the past year. Additionally, IPH operates with a high debt level which could pose financial risks.

The analysis detailed in our IPH growth report hints at robust future financial performance.

Delve into the full analysis health report here for a deeper understanding of IPH.

Key Takeaways

Get an in-depth perspective on all 49 Undervalued ASX Stocks Based On Cash Flows by using our screener here.

Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Curious About Other Options?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ASX:CKF ASX:DMP and ASX:IPH.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com